What is 678 Days Young?

DHL Wealth Advisory - Jul 04, 2025

The summer months are here, school is out, and markets seem to be more relaxed as well. In fact, all major indexes hit an all-time-high in this holiday shortened week. Overall, markets seem to have been energized in recent days with a dose...

The summer months are here, school is out, and markets seem to be more relaxed as well. In fact, all major indexes hit an all-time-high in this holiday shortened week. Overall, markets seem to have been energized in recent days with a dose of summer animal spirits, and momentum in the near term appears to be on investors' side.

With the mid-year point of 2025 in the rear-view-mirror, let’s look back at all the lessons that the global economy and financial markets taught us over this past six-month term—all of which pretty much defied every textbook ever written. And this list goes to 9:

- Middle East tensions will lead to lower oil prices and a weaker U.S. dollar. Following the U.S. Administration’s decision to bomb three of Iran’s nuclear sites this past weekend, oil prices plunged almost $10 from last Friday’s close, and the U.S. dollar weakened across the board—pretty much the opposite of what many feared or expected. The logical explanation for this unusual market reaction is that Iran’s initial response was mild and the U.S. almost immediately de-escalated. Still, the bigger picture over the first half of 2025 is that oil prices generally receded and most currencies strengthened versus the U.S. dollar, helping cap inflationary concerns in many economies.

- Markets love uncertainty. The first half of this year definitely ranked very high on the drama scale for financial markets, given the wild swings in trade policies, the aforementioned Mid-East flare-up, and lingering U.S. budget uncertainty. And yet, markets brushed off the flirtation with bear market terrain as recently as April. What makes the rapid return to all-time highs especially notable is that many of the sources of uncertainty remain unresolved, including the reciprocal tariff deadline of July 9. But even there, Treasury Secretary Bessent’s indication that major trade deals could be reached by “Labor Day” has rendered the July date less critical.

- Smaller, more volatile markets really, really love uncertainty. Even facing potentially the biggest hit from U.S. trade actions, Canada’s equity market has breezed higher, rising 22% from a year ago. In part, this reflects the fact that the TSX is not a great representation of the Canadian economy, and has been juiced by the strength in gold names (thank you Artemis and Kinross!). But, it also reflects the reality that the economy is faring better than the most dire expectations—GDP likely dipped at a 0.5% annual rate in Q2, but it’s still on track for a modest advance of just over 1% this year.

- Bigger budget deficits will lead to lower bond yields. As noted, the U.S. budget picture is not quite resolved just yet for this year, although the Senate appears to be getting close to a plan. However, the end result of the One Big Beautiful Bill will still likely add to the deficit forecast over the next decade, albeit not accounting for any extra tariff revenues. This means that the $2 trillion budget deficits will stick, and possibly widen. Initially, this caused some serious angst in Treasuries. Yet, 10-year Treasury yields have since faded, and are now down almost 30 bps since the start of 2025 to below 4.25%. Meantime, Canadian 10-year yields did nudge a bit higher over the past six months, in part due to very aggressive government spending plans, including a quick upswing in defence spending, first to 2% of GDP this year, and then to 3.5% within a decade. Canada/US 10-year spreads went from a record wide of -150 bps in January to -94 bps by Friday

- Threats to Fed independence will also lower Treasury yields. Following a barrage of criticism from the Administration over a lack of Fed cuts, rumours swirled this week that the Chair’s replacement would be announced far ahead of the May/26 term end. The Fed did stand out in the first half of the year as one of the few major central banks that did not cut rates—it is true. Yet, despite this lack of cuts, and even with the assault on the Fed’s independence, U.S. 10-year yields saw some of the biggest declines in the past six months.

- Aggressive interest rate cuts will help your currency strengthen. While the Fed sat on the sidelines through the first half of 2025, most other central banks kept right on cutting. The ECB has been among the most aggressive since the start of the year, chopping rates by 100 bps (on top of 100 bps in second half of last year).

- Tariffs will cause inflation to cool. One of the main reasons why the Fed stayed on the sidelines through the first half was over the uncertain impact of tariffs on inflation. Well, so far, so good. U.S. inflation data have been surprisingly—amazingly?—calm up to this point. While May core PCE prices were a tad above expectations at +0.2% m/m, the three-month trend was just 1.7%, matching the coolest pace in four years.

- Copper prices flunked their economics course. It’s long been said that copper is the commodity with a PhD in Economics. Well, copper, your alma mater is calling and they want their degree back. Even with many credible forecasters busily shaving their global growth outlook, copper prices have forged ahead by about 20% so far this year. There actually is some logic behind the upswing, as the weaker U.S. dollar has generally boosted commodity prices, and the threat of U.S. tariffs has played a role. But the firmness in the red metal may also be telling us that the global economic backdrop may not be as weak as earlier expected.

- Gold prices thrive when inflation is calming. The real rock star of commodities, and arguably all financial markets, in 2025 has been gold. While taking a big step back in the past two weeks, the yellow metal is still up 25% since the start of the year. Even in inflation-adjusted terms, bullion prices have surged to all-time highs, finally eclipsing the long-standing records reached way back in 1980. This strength has arrived even at a time when inflation has mostly moderated in much of the advanced world. The logical explanation is that gold has stepped in as a substitute safe harbour, along with the euro and Swiss Franc, when many have shunned the U.S. dollar.

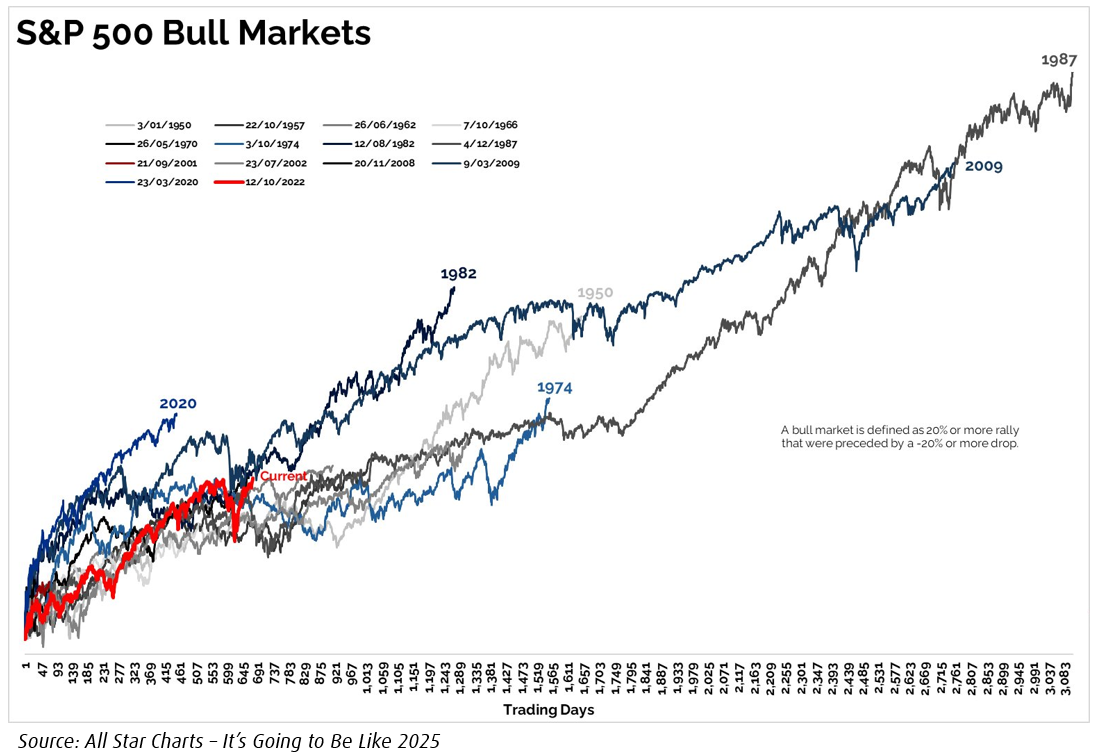

Meanwhile, the S&P 500 is up 72.6% over 678 trading days since the 2022 low, below the average bull market gain of 153.7% over 1,145 days. We’re now in year 3, a phase that’s historically flat and choppy. That’s typical mid-cycle digestion... not a red flag. This bull isn’t young, but it’s not stretched either. History still favors more upside… just not in a straight line.

Sources: BMO Economics Talking Points: School’s Out… Forever

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.