The Fed's Balancing Act

DHL Wealth Advisory - Jun 20, 2025

- Investment Services

- Portfolio Management

- Special Reports and Newsletters

- Total Client Experience

- Wealth Management

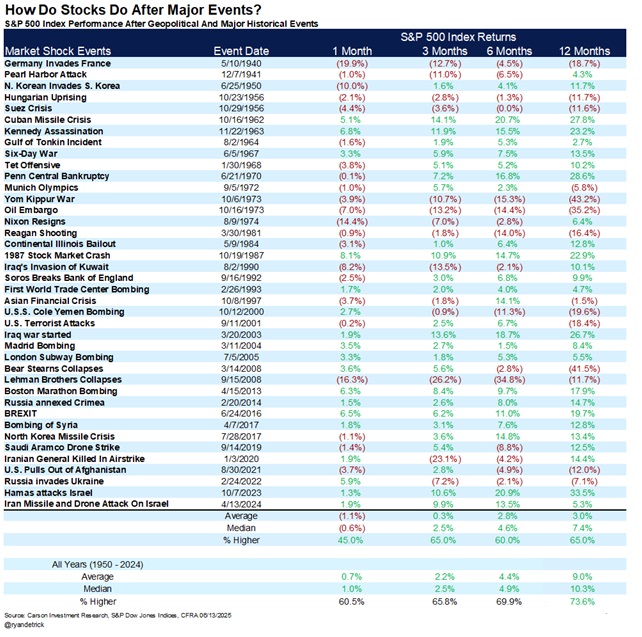

North American markets were basically flat on the week, but easily within reach of new all-time-highs. All this despite the ongoing conflict in the Middle East. The initial market reaction to the event last Friday...

North American markets were basically flat on the week, but easily within reach of new all-time-highs. All this despite the ongoing conflict in the Middle East. The initial market reaction to the event last Friday sparked a risk-off sentiment globally, as well as a sharp move higher in oil prices. Three key points to keep in mind as we navigate geopolitical uncertainty:

- Geopolitical tensions, while often taking a huge human toll, typically have short-lived impacts on financial markets and tend to be met with a flight-to-safety response as well as a rise in commodity/oil prices.

- The impact on oil and energy importing economies can be more severe than on exporters.

- Balanced portfolios tend to perform better during these times. The rise in the energy and commodity sectors can offset some of the broader equity market volatility, as an example.

We have used this table in prior instances of social unrest. It’s a great example of our first point above. Going back to the start of WW2, markets have generally been higher 3-12 months after an event.

Meanwhile, over the last week, we have gotten a few key updates on the trade and tariff negotiations. Perhaps the two we are watching most closely is a potential deal between the U.S. and China and the July 9 end of the 90-day pause with other major trading partners:

China and the U.S. have established a trading "framework" in theory: This past week, we heard from both U.S. and Chinese officials that a trade framework between the economies has been established. This includes tariffs on Chinese exports coming down from 145% to 55% (10% reciprocal tariffs, 20% fentanyl-based tariff, and 25% existing tariff on China). Tariffs on U.S. exports to China meanwhile remain at 10%.

In addition, there is further agreement on nontariff barriers, including critical Chinese rare-earth minerals. China has agreed to temporarily restore rare-earth licenses to U.S. manufacturers for six months, while the U.S. will relax restrictions on Chinese jet engines and related parts. While a step in the right direction, the U.S. and China trade relationship is a critical one to monitor in the months ahead.

The July 9 deadline on other trading partners may be extended as negotiations remain ongoing. Last week, Treasury Secretary Bessent indicated that the administration may extend the 90-day pause for top trading partners, if they show "good faith" in ongoing trade negotiations. We know that establishing trade deals that address tariff and nontariff barriers can take time, often months or years, and we would expect some extension for partners who are currently in discussions with the U.S. However, even during this pause, tariffs on these partners remain somewhat elevated at 10%.

The bottom line, in our view, is that uncertainty around tariffs remains, but the worst-case outcome or the highest tariff rates that were outlined on April 2 will likely be avoided.

Nonetheless, it is likely that tariff rates in the U.S. will move substantially higher from the approximate 2% rates we saw at the beginning of the year, to potentially 10%+ and even higher on China and other select sectors. We would expect average tariff rates with Canada to increase to between 5% and 10%.

This will likely weigh on both inflation and economic growth, as prices on goods move higher and consumption potentially slows. But it is important to keep in mind that both the U.S. and Canada are services-driven economies, with around 70% of GDP coming from services sectors. While tariffs could impact goods pricing and demand, they may not have as broad of an impact on a service-led economy.

Thus, while we expect prices to rise marginally and growth to slow in the quarters ahead, we still see positive economic growth, and we do not yet see a recession or prolonged downturn in the U.S. or Canada.

Elsewhere, as expected, the US Federal Reserve held their overnight rate steady at 4.25-4.5% on Wednesday for a fourth straight meeting. And, the Fed signalled that policy could remain on hold for at least a little while longer.

The statement said: “Uncertainty about the economic outlook has diminished but remains elevated. The Committee is attentive to the risks to both sides of its dual mandate”. On the first sentence, the words “remains elevated” are key. On the second sentence, the stagflation risk siren that was sounded last meeting (“the risks of higher unemployment and higher inflation have risen”) has been turned down, but it hasn’t been turned off.

In the ‘dot plot’, the median projection for this year stayed at two 25 bp rate cuts (to 3.875%), although one more participant joined the ‘one-or-none’ club (it now boasts nine members with just one more needed to turn the median dial). For next year, the median call is now for only one cut; it was two before. The stagflation-skewed projection alterations are prompting more Fed policy caution.

In the press conference, Chair Powell observed that labour developments, on balance, are still not “troubling” and economic growth is still “decent”. This affords the Fed more time to wait and see how inflation pressures mount this summer owing to tariffs (and the Fed is anticipating some pressures).

Bottom line: The Fed is weighing the risks of slower growth against those of faster inflation. If the former is significantly heavier, the Fed will likely ease, but if the latter is meaningfully heavier, the Fed will probably remain on hold (recall policy is still on the restrictive side). By summer's end, we should be starting to see an emerging tilt to the slower growth side, setting the stage for a rate cut or two.

Source:BMO Economics EconoFACTS: FOMC Policy Announcement and Summary of Economic Projections

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.