May Trade Note.

DHL Wealth Advisory - Jun 06, 2025

- Investment Services

- Portfolio Management

- Special Reports and Newsletters

- Total Client Experience

- Wealth Management

Global economy – slowing, not cratering. While front-running in US imports benefitted economies outside the US in Q1, a pull-forward in consumption ahead of tariffs may be temporarily boosting US growth in Q2...

Global economy – slowing, not cratering. While front-running in US imports benefitted economies outside the US in Q1, a pull-forward in consumption ahead of tariffs may be temporarily boosting US growth in Q2. Going into H2, we expect the US economy to trend toward weaker global growth conditions, but the transition could be smooth and a global recession averted. One important source of support is the consumer who is now enjoying some relief due to the rapid deceleration in inflation for essentials, which is freeing up funds that can then be used to buy discretionary goods and services. Moreover, while jobs creation in non-cyclical industries is downshifting due to reduced government employment, it is picking up in cyclical industries. Overall, as much as the second-order impact of US tariffs and tightening financial conditions have yet to filter through the global economy, recession odds have certainly trended lower.

Begs the question: Have pundits been too downbeat on the economic outlook in recent months? Using the ‘Royal We’ there, of course, but the question still holds. Since the trade war rolled into town—early in 2025 for Canada, Mexico, and China, and April for most everyone else—the consensus has been busily marking down the growth forecast for this year and next, while mostly pushing up the core inflation outlook. And, yes, the “consensus” includes us. Meantime, sentiment among businesses and consumers has pretty much fallen off a cliff in North America, with U.S. households especially rattled by the prospect of renewed inflation. Equity markets initially fully shared those concerns, flirting with a 20% drop from February to early April for the S&P 500.

But, famously, stocks did not stay down for long. With the rebound erratically resuming this week, the S&P 500 is now up 20% from the early-April lows and not far removed from all-time-highs. The MSCI All Country Index is up by a similar tally, and managed a monthly gain of 5% for May. Initially, many analysts and economists wondered aloud if the rebound in stocks wasn’t getting too far ahead of reality. But, just as the equity market first sensed the possibility that sentiment had been too downbeat, the economic survey data are beginning to flag the same. This week saw both major U.S. consumer confidence surveys bounce from the lows in May, with the Conference Board’s measure jumping 14%, the biggest monthly increase in four years. The University of Michigan found that consumer inflation expectations had backed down from the mountain in May, albeit holding at high levels (4.2% over the next five years and a whopping 6.6% for the next year).

It’s not just the soft data that are improving and/or holding up better than expected. U.S. growth, while underwhelming, is hardly wilting. True, jobless claims perked up last past week to 240,000, but the four-week average held fast. And, true, real GDP dipped 0.2% in Q1, but a spike in imports was the driver there. With imports pulling back sharply in April, that quirk will be soon reversed, possibly prompting some to lift Q2 growth estimates—the Atlanta Fed’s early read was already at a decent 2.2% prior to the helpful trade data, and has now been lifted to a solid 3.8%. And while real consumer spending was sluggish in April at +0.1%, the three-month trend of 3.4% growth is solid. No doubt, housing is heavily challenged by the uncertainty and by 30-year mortgage rates of nearly 7%. So, make no mistake, the economy is not on the verge of breaking out, but a spell of modest growth seems the most likely outcome.

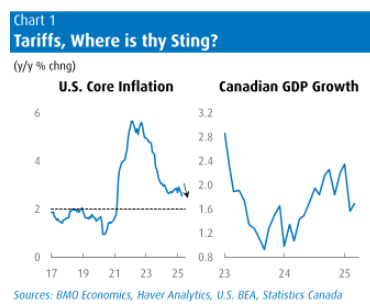

At the same time, the great tariff inflation scare seems to be everywhere except in the data. The Fed’s closely watched inflation gauge remained very well behaved in the first month of the trade war. The core PCE deflator nudged up just 0.1% m/m in April, following a like-sized rise the prior month. This shaved the annual inflation rate to a mild 2.5% y/y clip, its slowest since March 2021, or back before inflation really got rolling. The overall figure is even better at 2.2% y/y, held down by sinking energy costs. Tariffs, where is thy sting? We have consistently been on the side asserting that the trade war is a bigger threat to growth than inflation, and the very mild price results so far do nothing to alter our contention.

If anything, the assertion that sentiment has been too downbeat versus reality seems even more compelling in Canada. The TSX has leaned that way, with the index cruising to a series of record highs this week, before retreating. And the Canadian dollar has snapped back by almost 5% since February. On the one side, confidence was shattered for both consumers and businesses by the multiple trade threats, as well as a burst of political uncertainty in the first four months of 2025. On the other, the economic data have been even sturdier than in the U.S.—at least on headline GDP. In stark contrast to the small U.S. dip in Q1, Canadian growth handily topped estimates with a 2.2% showing, even slightly above the prior quarter. Yes, the details were hardly positive, as final domestic demand actually slipped slightly, but amid the intense trade uncertainty and a tough winter, the gain was above anyone’s forecast. Perhaps even more surprisingly, the flash estimate suggests the economy was still grinding forward in April.

Make no mistake, we have not suddenly become pie-eyed optimists on the Canadian growth outlook. Economists continue to look for a mild pullback in GDP in both Q2 and Q3, with business investment and housing bearing the brunt. But, forecasts expect growth for the full year to be a bit above 1% this year and next, not far from the 1.5% average pace of the past two years.

Trades:

Following an extremely busy April, we let the markets do the heavy lifting higher in May. The result was our best monthly gain ever for our flagship Income Growth mandate which saw gains of ~9% in May, good for +12% thus far in 2025.

Trim:

Artizia (ATZ): Following a blockbuster earnings report, and a tactical add on weakness earlier in April, we trimmed a small amount in shares of Aritzia. We continue to hold this stock as a core holding, but price appreciation made it a large over-weight. We reduced the position back to ~3%.

Source: BMO Economics Talking Points: An Overabundance of Caution?

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.