Have a Tariffic Mothers Day!

DHL Wealth Advisory - May 09, 2025

- Investment Services

- Portfolio Management

- Special Reports and Newsletters

- Total Client Experience

- Wealth Management

Global markets continued to rally this week stringing together three solid weeks of gains. In fact, US benchmarks are surprisingly higher today than where they were on the universal tariff announcement day – aka “Liberation Day”...

Global markets continued to rally this week stringing together three solid weeks of gains. In fact, US benchmarks are surprisingly higher today than where they were on the universal tariff announcement day – aka “Liberation Day”, but we’ll refrain from such theatrics.

Moving markets this week was a continuation of Q1 earnings season that is largely coming in better than expected along with ongoing de-escalation of tariff rhetoric. With respect to earnings, over half of the Canadian TSX companies have reported and +80% of S&P 500 companies.

In Canada, earnings growth is tracking towards 9% year-over-year for Q1, below expectations of about 15% at the end of 2024. While in the U.S., earnings growth for Q1 remains on track for 12.5% year over year, above the 11.5% expected at the end of last year. Around 76% of companies have reported positive earnings surprises, above the 10-year average beat rate of 75%.

Naturally, all eyes remain focused on the next three months, not the most recent three. Given the fluid macro backdrop around the consumer and tariff, guidance for the second quarter of earnings growth has weakened in both the U.S. and Canada. The earnings growth forecast for Q2 has fallen to 5.8% in the U.S. and 3.2% in Canada.

We have already seen meaningful downward revisions to the second quarter, as well as lowered expectations for Q3 and Q4. The expectation for corporate earnings growth for 2025 in both economies remains at about 10% annually. While this may be revised somewhat lower, historically, if earnings growth is positive, we have not experienced recessionary environments.

With respect to recessionary chatter, Canadian GDP growth for February softened to 1.6% year-over-year, below expectations of 1.7% and last month's 2.2%. We continue to see weak retail sales and consumer confidence in Canada as well. Given the potential for tariffs to impact prices of goods. However, BMO’s economics team does not expect negative economic growth or a deep recession, given the potential for both fiscal stimulus from the newly formed government and interest rate cuts by the Bank of Canada, both of which would support household and corporate spending.

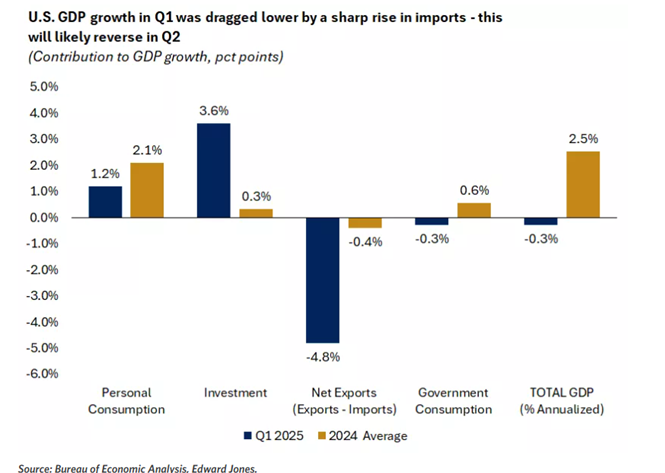

Similarly in the U.S., first-quarter economic growth came in weaker than expected, as gross domestic product (GDP) growth fell by -0.3% in Q1 versus an expectation of -0.2%. This was driven largely by a surge in imports — the biggest in nearly five years — as companies purchased goods in anticipation of higher tariff rates.

In both the U.S. and Canada, growth may rebound in 2026 if central banks cut rates in the back half of 2025 and progress is made on fiscal stimulus and deregulation. This should support both consumer and corporate spending broadly.

And back to what else. The ongoing trade war. At least three developments this week were widely interpreted as turning down the temperature on the trade war, and thus provided modest support for equity prices, bond yields and the U.S. dollar. Probably most important, the U.S. and China managed to agree to talk, without either losing face—some form of negotiations begin this weekend in neutral Switzerland. Second, with much fanfare, the U.S. and U.K. agreed on a preliminary deal to dial down tariffs on metals and autos, perhaps providing a framework for others. And, finally, Canadian PM Carney’s high-stakes meeting at the White House at least set the stage for less fractious relations between the two massive trading partners than the past four months. While there was no white smoke from Washington, as the PM predicted, the calmer tone is a small positive.

Notwithstanding those dry facts, the market remains understandably focused on the high-wire U.S.-China negotiations. There are plenty of signs that the triple-digit tariff rates of the past month have all but brought trade to a standstill, with the President noting that ships are turning around in the ocean. It’s hard to believe that a full agreement can be reached anytime soon, given the gulf between the goal of balancing trade and the hard reality of a $305 bln deficit with China. However, there is certainly scope for the current trade-debilitating tariffs to be partially pulled back in short order, but it would hardly be cause for big celebration if we land at, say, 80%.

The early returns on how various economies are dealing with the first month of the full-on trade war are beginning to trickle in, and the news on the hard economic data is mixed. Starting in the U.S., last week’s jobs figure was firm, giving no obvious sign of strain, while the 4-week average of initial jobless claims has only nudged up to 227,000. This week’s services ISM was surprisingly steady at 51.6, and supply chain pressures actually eased last month. Now all eyes will turn to next week’s CPI and retail sales, but both are expected to post low-drama results—annual inflation is expected to stay stable for headline (2.4%) and core (2.8%), with 0.3% monthly increases for both, while tiny gains are expected for total and ex-auto retail sales.

The main point is that the U.S. economic data are hardly flashing serious warning signs, despite the deep dive in many sentiment surveys. This didn’t stop the US Federal Reverve from cautioning in its post-FOMC statement that there were now upside risks to both unemployment and inflation. On cue, the latest Blue Chip survey shows that the consensus now looks for just 1.2% GDP growth this year, down a full point since the start of the year, while unemployment is expected to climb to 4.4%, even as inflation has been lifted to 3.2% (from 2.5% in January). That combo has left the Fed in a box so far this year, with rates unchanged since December—much to the deep chagrin of the Administration. Markets have now pushed back the likely timing of the next cut to July 30, and we concur.

Overall, stock markets have rebounded remarkably well over the past three weeks. Queue our often used cliché that it’s about time in the market, not timing the market. The past few weeks have proven this exceptionally well.

Nonetheless, keep in mind that volatility is normal. In any given year, two to three pullbacks are likely — especially in a year when we have elevated uncertainty around tariffs, inflation and economic growth. However, given that we do not expect a deep or prolonged recession in the U.S. or Canada, we continue to view periods of volatility as opportunities to rebalance, diversify or add to portfolios across sectors and asset classes.

While uncertainty remains elevated this year, there are indeed tailwinds intact for the market. Not only from further concrete trade deals and details, but also a Fed and Bank of Canada that are on-track with rate cuts, policymakers making progress toward fiscal stimulus and tax reform, and earnings growth that is poised to re-accelerate — all supportive of improved market sentiment.

Source: BMO Economics Talking Points: No Smoke on the Water

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.