Happy Easter!

DHL Wealth Advisory - Apr 17, 2025

- Investment Services

- Portfolio Management

- Special Reports and Newsletters

- Total Client Experience

- Wealth Management

It was a mixed holiday shortened week for major North American benchmarks with Canada’s TSX posting decent gains and our counterparts to the South seeing small losses...

It was a mixed holiday shortened week for major North American benchmarks with Canada’s TSX posting decent gains and our counterparts to the South seeing small losses. Moving markets this week was continued headlines of uncertainty surrounding tariffs while also getting a string of stronger-than-expected economic data.

In Canada this week we learned that inflation for the month of March came in lighter than expected. Canadian consumer prices rose 0.3% in March (or flat in seasonally adjusted terms), much lower than expected and cutting the annual inflation rate 3 ticks to 2.3%.

The pullback in headline inflation is a pleasant surprise, given that this month represents the full removal of the GST holiday (which was still in effect for half of February). The big story here was a steep drop in travel tour prices and a meaty drop in airfares from year-ago levels, as Canadians pulled back abruptly on U.S. travel in prime time. And while the overall result was helped by a modest 1.8% drop in gasoline prices, those pump costs are poised to plummet by more than 10% m/m in April, likely carving the headline inflation rate well below 2% a month from now.

After a couple months of high-side surprises, Canadian inflation caught a serious March break, held down by much milder travel costs than normal. This speaks to the fact that the inflation impact of the trade war is more of a two-way street for Canada than the U.S., since Canada's tariffs are so much lighter so far, while the domestic economy is under more pressure. As well, the reversal of the Canadian dollar into firmer terrain erases one of the BoC's inflation concerns, as it will hold back import prices. Normally, this would be a big green light for the BoC to cut interest rates on Wednesday, but alas…

The Bank of Canada did not cut interest rates on Wednesday in what was the first “pause” following a string of seven consecutive meeting cuts going back to June of last year. The BoC held rates steady at 2.75% in what was viewed as a close call, but markets had been leaning to no move as well. The policy announcement focused mostly on the extreme degree of uncertainty in the outlook, with the Monetary Policy Report employing two potential scenarios (and admitting there are plenty of other possibilities).

It's tough to characterize the tone of the Bank's stance, as it indicates that it both is "prepared to act decisively" and yet "will proceed carefully and be less forward-looking than usual until the situation becomes clear". The point is that the Bank will mostly act reactively, which helps explain why it decided to hold. As well, for Canada at least, the trade outlook has not changed materially since the prior rate decision in March—"the situation is no clearer"—even as the global trade landscape has deteriorated heavily.

Elsewhere (I did say it was a busy week for economic data), we got a much stronger US retail sales report than we have seen in a long time. The monthly increase was the best since January 2023. Total U.S. retail sales jumped 1.4% in March, in-line with consensus forecasts. Retail sales excluding autos and gas stations increased a better-than-expected 0.8%. Tariff front-running clearly helped lift retail sales to a whole new level of growth last month, easily offsetting the drag from gasoline stations. A modest decline in CPI inflation in March means we saw meaningful real retail sales gains for the first time this year. This was something we hit on last week on reasons to not be overly pessimistic: Still strong consumer spending, slowing inflation, and a still growing economic backdrop. This week we had positive news on all three.

However, that wasn’t enough to drive gains in the US markets for the week with tariff noise firmly in the driver season. We’ve talked about this ad nauseam the last six months, but a pick-up in volatility was inevitable following two years of relatively tranquil markets. Historically, the average intraday move (difference between the daily high and low) for the S&P 500 has been around 1%. But since the higher tariff plan was revealed on April 2, the average intraday move has jumped to a jaw-dropping ~5%.

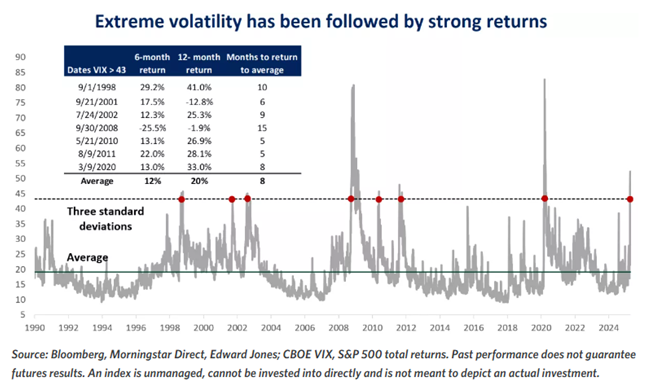

Highlighting the extreme market fluctuations and uncertainty, the volatility index (VIX), also known as the fear index, spiked last week to the highest since the early days of the 2020 pandemic. The index has been that high only eight times in the past 35 years. Typically, it takes a while for volatility to return to normal, on average about eight months. But what history shows is that fear creates opportunities for those that follow a disciplined and patient approach. Once the VIX index has exceeded 43 (it reached a high of 52 on 4/8/25), forward six- and 12-month equity-market returns have been strong. That is not because volatility itself is good, but because spikes in volatility tend to occur when pessimism is already priced in.

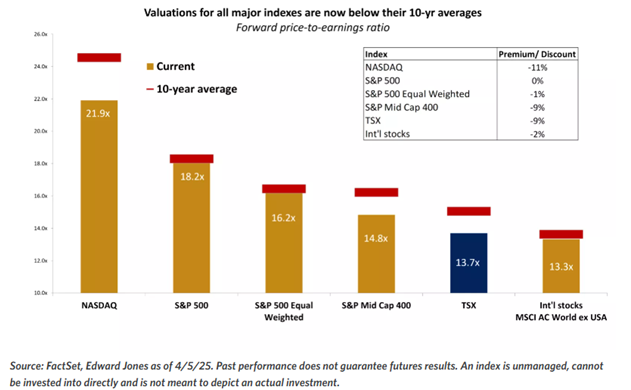

A V-shaped recovery in stock prices is not likely as long as trade headwinds persist. However, the upside of this down market is that valuations are now looking more compelling and are no longer stretched, which was a concern coming into this year. All major indexes are trading at or below their 10-year historical averages.

We are by no means out of the woods as progress on trade deals will be needed for markets to calm down. We hope that next chapter in the trade war will be de-escalation. But alas hope is not a strategy. To navigate this environment, we recommend adhering to the following principles:

- Focus on what you can control (diversification, quality investments, long-term perspective).

- Amid headline noise, avoid making emotionally charged decisions, which more often than not lead to subpar outcomes.

- Time in the market is better than timing the market.

- Understand the risks of not investing. Assuming 3% inflation, prices will double during a normal 25-year retirement period. Therefore, it is critical to own assets that can help you maintain your purchasing power over time.

- Talk to your advisor!

Sources: BMO Economics EconoFACTS: Bank of Canada Rate Decision and MPR, BMO Economics EconoFACTS: U.S. Retail Sales (March), BMO Economics Canadian Housing Monitor: Canadian Housing Monitor: March 2025

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.