And the Penguins Breathe a Cold Sigh of Relief

DHL Wealth Advisory - Apr 11, 2025

- Investment Services

- Portfolio Management

- Special Reports and Newsletters

- Total Client Experience

- Wealth Management

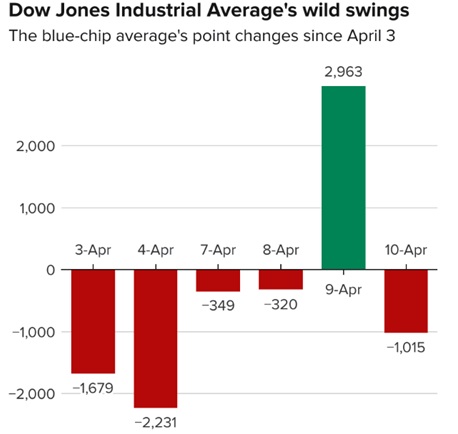

What a dizzying week… The past five days have truly been one for the record books. Monday saw an incredibly 8% whipsaw in major benchmarks on “false” reports that the Trump administration was holding off on reciprocal tariffs for 90 days...

What a dizzying week… The past five days have truly been one for the record books. Monday saw an incredibly 8% whipsaw in major benchmarks on “false” reports that the Trump administration was holding off on reciprocal tariffs for 90 days. Markets reacted positively to the report but quickly gave back gains after the administration denied the claim. Tuesday and Wednesday morning markets went dramatically lower then on Wednesday afternoon we got an opening.

Catching everyone off guard, Trump said that he will reduce, for 90 days, the reciprocal tariff rate to 10% (from up to 50%) for the more than 55 countries that had a reciprocal rate above the 10% global base tariff (this includes an important tariff reprieve to uninhabited islands around Antarctica). At the same time, Trump hiked the tariff rate on China to 125% as retribution for its retaliatory actions. The response was the 3rd biggest single day gain for the S&P 500 since WWII at 9.5%. The NASDAQ was up a jaw-dropping 12.2%.

Source: CNBC

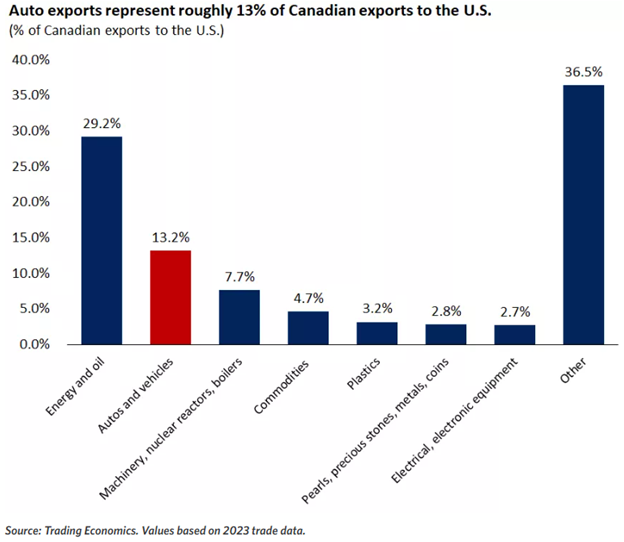

While Canada is still exempt from the reciprocal tariff, the previously announced levies still pose a headwind to economic growth. Trade as a percent of GDP in Canada is roughly 67% with the U.S. responsible for roughly 76% of Canadian goods exports. If the U.S. economy slows due to the recent tariff announcements, Canadian growth will likely slow as well.

Additionally, energy and autos are Canada's largest exports to the U.S., while commodities, which include steel and aluminum, are among the top 10. Each of these will be subject to tariffs from the U.S., which will likely weigh on activity in these sectors. The prior week's labour force survey showed Canadian employment contracted modestly in March while the unemployment rate ticked higher to 6.7%, perhaps signaling businesses have already adjusted hiring plans based on the policy uncertainty.

However, the Canadian economy entered 2025 with strong momentum. Real GDP expanded at a healthy 2.6% rate in the fourth-quarter driven by robust household spending. Additionally, the Canadian Government has room to provide fiscal support to businesses impacted by the tariffs, which could provide support to the economy over time.

How the incremental revenue from tariffs is used will be critical in determining the economic impact on the U.S. If a large portion of this revenue is deployed to areas that promote growth, such as financing lower taxes, economic growth could hold up better. However, if a majority of the additional tariff revenue is used to reduce the U.S. fiscal deficit, U.S. economic growth could slow more meaningfully.

While tariffs will serve as a headwind to economic growth, like Canada, the U.S. economy is entering this period from a position of strength

- U.S. real GDP has expanded at an above-trend pace over the past two years, and S&P 500 earnings per share grew by 18% in the fourth quarter, the strongest growth rate since the fourth quarter of 2021.

- Household balance sheets remain healthy, with the average household debt-service ratio (the percent of household disposable income spent to service debt payments) below pre-pandemic levels.

- Labour-market conditions remain healthy, even as some softening is expected ahead. Initial jobless claims have averaged roughly 221,000 thus far in 2025, well below the 30-year average of over 360,000. Nonfarm payrolls grew by a healthy 228,000 in March, well above consensus expectations for 130,000, while the unemployment rate rose modestly to 4.2%.

While recession risks have clearly risen, in our view an economic downturn is not a foregone conclusion. A strong starting point could provide support to the Canadian and U.S. economies. Additionally, with U.S. monetary policy in restrictive territory, the Fed has ample room to cut rates if the economy shows meaningful signs of slowing. While the BoC has cut rates more aggressively, additional rate cuts could be on the table if economic conditions slow, while fiscal stimulus could provide support as well.

Meanwhile, lost in the noise this week was a considerably better-than-expected US CPI inflation report which eased for the second consecutive month in March (caveat being just before a wall of U.S. import tariffs went up in April. Headline CPI actually decreased 0.1% last month on plunging gasoline prices, falling commodities prices, and easing services inflation.

This was the first monthly decline in consumer prices since May 2020. This better-than-expected report gives the US Federal Reserve some room to cut interest rates later this year, if emergency rate cuts were needed to rescue the labor market from recession. The Fed will need to see continued easing of services inflation to help offset any large increases in goods import prices in the months ahead. From a year ago, CPI inflation moderated to a much more comfortable 2.4% from 2.8% in February, beating consensus expectations for a moderation to 2.5%.

Bottom Line: This was another well-behaved CPI inflation report (the second in a row) that showed encouraging signs of moderating services inflation. Fed funds futures are now pricing in between 3 and 4 quarter-point rate cuts in 2025 with the first one coming as soon as June.

Circling back to the markets, with uncertainty likely to remain in the coming weeks, we recommend investors resist the urge to make emotionally charged decisions, and instead stick with their long-term investment strategy. It's important to remember that on average, the S&P 500 experiences three to four pullbacks of 5% per calendar year and one pullback of 10% per year. Additionally, pullbacks of 15% occur on average once every two years, while pullbacks of 20% or more occur about once every three years.

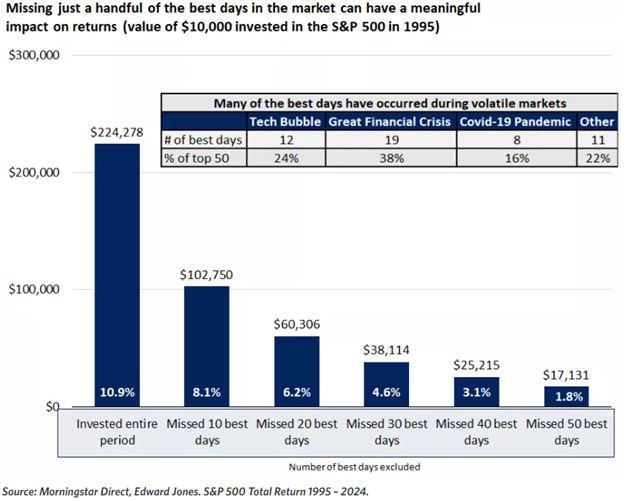

Over the long run, we believe time in the market is a better investment strategy compared with timing the market. Sorry, we know you’re probably tired of hearing that, but its importance cannot be understated – just look at Wednesday 10-14% intraday rally off its lows. In fact, missing just a handful of the best days of the S&P 500 over the past 30 years would have led to meaningfully lower returns. What's more, many of the best days in the market have come during periods of market volatility (like Wednesday), highlighting the importance of maintaining a long-term focus through turbulent markets.

Sources: BMO Economics EconoFACTS: 90-day Pause on U.S. Reciprocal Tariffs, BMO Economics EconoFACTS: 90-day Pause on U.S. Reciprocal Tariffs

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.