March Showers

DHL Wealth Advisory - Mar 21, 2025

- Investment Services

- Portfolio Management

- Special Reports and Newsletters

- Total Client Experience

- Wealth Management

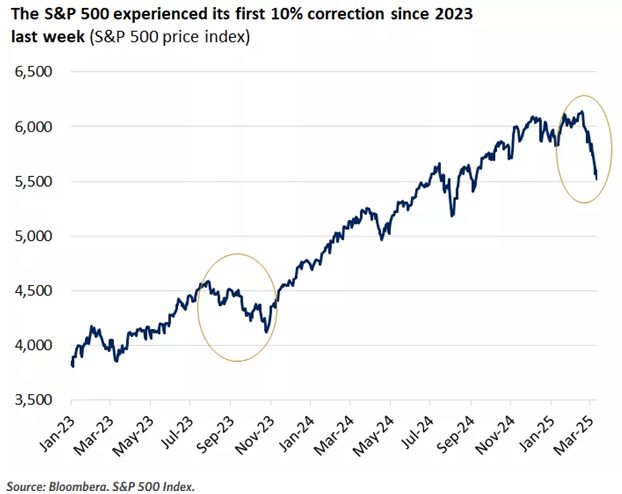

The stock market remained volatile over the last week, with the S&P 500 briefly dipping into correction territory, down 10.1% from its recent highs. This was the first 10%+ drawdown in the S&P 500 since October 2023, nearly 1.5 years ago...

The stock market remained volatile over the last week, with the S&P 500 briefly dipping into correction territory, down 10.1% from its recent highs. This was the first 10%+ drawdown in the S&P 500 since October 2023, nearly 1.5 years ago. But this one happened fast. In 2023, the correction took four months to play out. This time around. Less than four weeks.

Elsewhere, the technology-heavy Nasdaq has dropped about 14% from peak-to-trough this year. And Canadian markets, while they have held up considerably better, have seen a pullback of about 6.5% from peak to trough this year.

This pullback comes as markets grapple with a few concerns:

- U.S. and Canadian economic growth seem to be shifting to a slower gear. Data thus far in the first quarter points to positive, but softer consumption, with consumer sentiment surveys also indicating some weariness in confidence overall.

- The big elephant in the room. Tariff uncertainty has become an overhang, not only on consumers, but on corporations that may be delaying spending or capital-markets activity until there is more clarity.

However, it’s a Friday afternoon and we are a half glass full type of team. Despite all this negative sentiment, there have been pockets of strength, and most of our diversified portfolios are actually up a handful of percent and not far removed from all-time-highs.

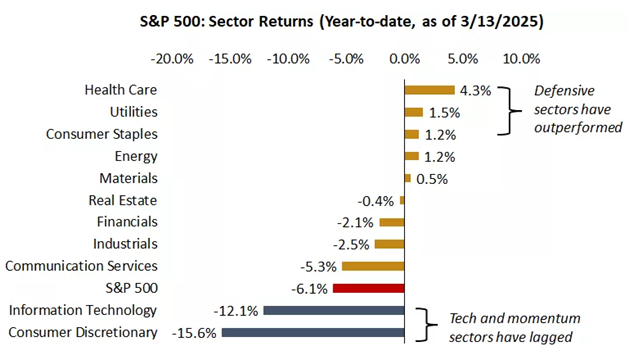

Within the U.S. stock market, for example, five of the 11 sectors of the S&P 500 are positive this year. And we have seen defensive sectors outperform technology and growth sectors thus far.

Source: FactSet

Notably, in Canada, only three of the 11 sectors of the Canadian TSX index are positive this year. These include materials, communication services, and utilities. While the Canadian stock market is basically flat this year, much of the underlying sector performance has come from materials and gold stocks, as gold prices hit new highs for the year.

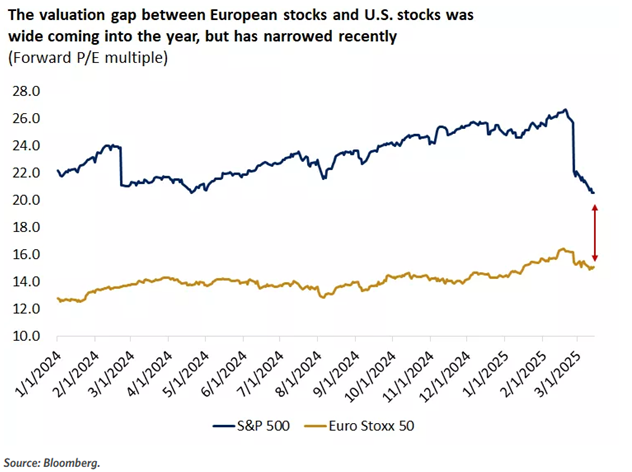

We have also seen bond markets outperform equity markets and deliver positive returns, as investors have flocked to safe havens as uncertainty and volatility remains elevated. Finally, international markets have dramatically outperformed U.S. and Canadian stocks this year. Thankfully we have a European sleeve in all of our discretionary accounts. This outperformance has come as investors rotated especially out of higher-valuation U.S. stocks into areas of the global market that offer better valuations and exposure to both growth and value.

In our view, over the long term international and EM equities may not consistently outperform domestic stock markets, especially if the U.S. and Canada can deliver over time on productivity and earnings growth. However, we continue to see international stock markets having a role in diversified portfolios, especially this year when the U.S. and Canadian growth outlooks have softened.

To us, this underscores the value of portfolio diversification and active management. Overall, after two years of strong performance in the stock market, driven in the U.S. primarily by mega-cap technology and AI sectors, we have seen in 2025 thus far a return to stock and asset selection. For long-term investors, market volatility and stock-market pullbacks are not pleasant, but they can offer opportunities – to rebalance or add quality investments across a diverse set of stocks, bonds and international markets.

Meanwhile, BMO’s Chief Investment Strategist Brian Belski had a good report out this week that we thought was worth highlighting. Belski is confounded (once again) with the plethora of macro forecasts that have been released the past several days that contain vigorous and decisive directness within what he believes is a blizzard of ambiguity and opacity. Furthermore, conclusions cannot and should not be made before the final variables are known. To use another analogy, you need to run the race before you know your final time.

Source: Canadian Strategy Snapshot: Freeze Frame

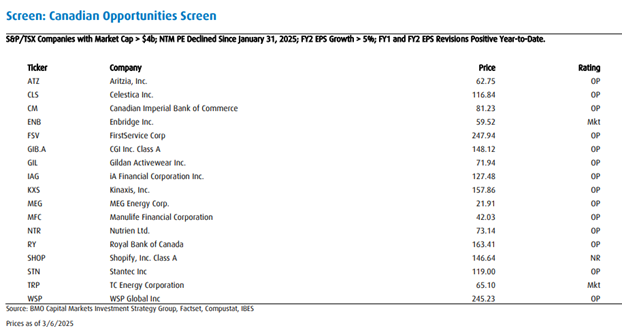

Uncertainty scares investors and reactionary analysis only magnifies the noise in his view. To be clear, tariff actualities and political consternation is all about duration risk. Fear of the unknown causes strife and Canada is chalk full of strife right now, unfortunately. NO ONE KNOWS. Humility is the better tactic. So let’s deal with what we know. Belski sees NO material change in forward fundamentals in terms his Canadian models. As such he is not changing his 2025 target for the TSX. YES, he continues to believe Canadian equities will hit new all-time highs by year end. Do not take this conviction as being flippant. Fear is a powerful emotion and uncertainty is the ice that is freezing Canadian investors. However, there are always opportunities, after all Canada has some of the best companies with the best products and services in the world. As such, he believes investors should be looking for opportunities over the next several months for companies that are being unfairly punished. Belski has created a screen of S&P/TSX companies that have seen valuation compression so far this year, despite having positive FY2 EPS growth expectations and have seen positive revisions to both FY1 and FY2 EPS.

Source: Canadian Strategy Snapshot: Freeze Frame

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.