MWW - The Mag (9)7

DHL Wealth Advisory - Feb 21, 2025

Despite the big macro headlines, it was a somewhat uneventful week for equities, which in fact quietly saw a couple new all-time-highs out of the S&P500. We talked at length in our last week’s edition about the ongoing earnings season..

Despite the big macro headlines, it was a somewhat uneventful week for equities, which in fact quietly saw a couple new all-time-highs out of the S&P500. We talked at length in our last week’s edition about the ongoing earnings season. At this stage, we are at the tail-end of the season, and while the trend continues to be better-than-expected. That is not exactly the case for the so called Mag 7…

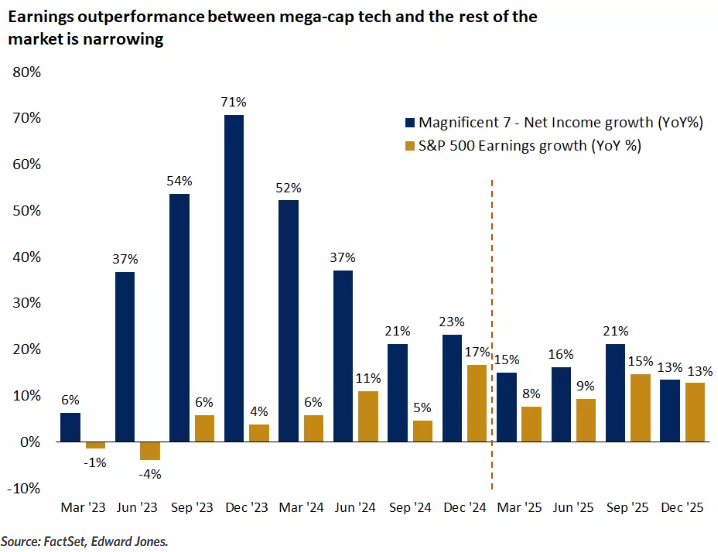

The Magnificent 7 group of companies (Apple, Microsoft, Amazon, Alphabet, Meta, NVIDIA, and Tesla) that comprise about a third of the S&P 500 weight has lost some of its luster so far this year. Even though the group has contributed more than half of the S&P 500 gain in the past two years, performance is lagging in 2025, while sales growth in the fourth quarter of 2024 was at its slowest since 2022. Increasing competition in the artificial intelligence (AI) arena and rising spending are raising concerns about valuations, which carry a 35% premium to the broader index.

Source: Factset

What’s unfolding is a leadership rotation into other areas of the market. We have seen a couple false starts of this long-awaited rotation to areas outside of mega-cap tech for years now. It seemed we were well on our way back in 2023, but enter stage left Artificial Intelligence. Did that ever put the great rotation on pause with big tech once again leading the way. What’s a bit different this time is that profits for the Magnificent 7 are indeed slowing after two years of explosive growth. We are by no means saying these are now bad investments. Results remain strong. Earnings for the group rose 25% in the fourth quarter, still outpacing the S&P 500, but to a lesser extent than in the recent past. Up until last week, tech was the only sector down for the year, a stark difference to its dominant position over the past two years. On a positive note, that hasn't been enough to drag the whole market lower. We see the broadening of market leadership as a healthy development for the sustainability of the bull market in stocks.

Source: Factset

The bigger story, in our view, is that earnings growth for the S&P 493 (subtracting the Magnificent 7) is accelerating after a two-year lull. For the fourth quarter, financials, health care, and real estate are joining the sectors that house the growth stocks (tech, communication services and consumer discretionary) in delivering double-digit profit growth. And the broader index is on track for its highest quarterly earnings increase in three years, with profits growing 17% from a year ago compared with expectations of 12% growth before earnings season started.

Source: Factset

Under the hood, leadership is shifting, which is a positive development for diversified portfolios that stand to benefit from sector, style and geographic rotations. While the broader market has generally been moving sideways for the past three months, as they've had to absorb news about increasing AI competition, tariffs, and a hotter-than-expected inflation, they remain well supported by positive fundamentals. Headline volatility will always be present, especially this year, but investors will be served well by separating the signal from the noise.

Elsewhere, the January Canadian CPI inflation report on Tuesday was not a bad result, with the headline and most measures of core up 0.1%-to-0.2% m/m in seasonally adjusted terms. That compares quite well to the unsettling 0.4%-to-0.5% bumps in the U.S. CPI for the start of the year. Still, there is little debate that underlying inflation is no longer improving in Canada, and in fact seems to be grinding a bit higher recently. This week’s Focus Feature looks at some of the quiet strong points in the Canadian economy at the moment; it suggests that if we weren’t all talking about tariffs, we would be talking about how the economy had turned the corner after a tough spell with higher interest rates.

Source: AM Charts for February 19, 2025

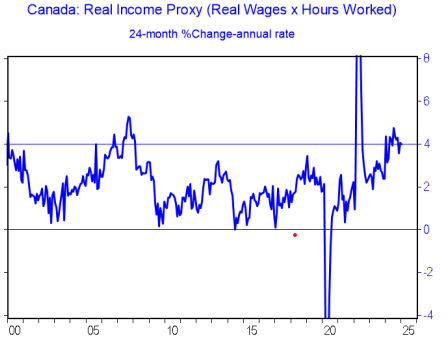

One of the key points is that Canada is highly sensitive to rates, arguably more so than any other economy. So, along with the BoC being the most aggressive cutter out there, this sets up a big tailwind for the economy. But on top of that, we’ve also seen both robust job growth (2.0% y/y) and solid real wage growth (1.6% y/y), as well as longer workweeks.

Source: AM Charts for February 21, 2025

Taking all that together, a proxy of real incomes is up about 4% y/y, and that’s also true over the past two years (so it’s no fluke). As the chart shows, that’s the strongest this measure has risen in the past 15 years (aside from the pandemic distortion). Despite all the focus on tariffs and the mortgage resets, consumers are in fact well-armed.

Source: AM Charts for February 21, 2025

Source: Haver Analytics

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.