Trumps V-day Card to the World: You're Tariff-ic!

DHL Wealth Advisory - Feb 14, 2025

- Investment Services

- Portfolio Management

- Special Reports and Newsletters

- Total Client Experience

- Wealth Management

Global markets are certainly embracing the fluid backdrop with open arms as major indices broadly finished higher on the week as sentiment improved after investors got more certainty around President Donald Trump’s tariff plans...

Global markets are certainly embracing the fluid backdrop with open arms as major indices broadly finished higher on the week as sentiment improved after investors got more certainty around President Donald Trump’s tariff plans. It’s a strange world we find ourselves in where the U.S threatens pretty much every country with “reciprocal” tariffs, as soon as April 1, and that’s viewed as relatively good news by markets, since it leaves time for the world’s best deal maker to… make some deals?

There are of course some solid fundamental factors that are keeping markets on the straight and narrow. The upswing in stocks to near-record highs following some softness around the turn of the year has been keyed by generally positive Q4 earnings. Sentiment appeared to calm after January’s producer price index, as well as the consumer price index report released earlier this week, suggested a softer reading for the personal consumption expenditures price index. The PCE price index, which is due later this month, is the Federal Reserve’s preferred inflation gauge.

One of the biggest drivers of underlying stock-market performance is the direction of corporate earnings. In our view, earnings for 2025 remains on track for 10%-15% growth year-over-year, the highest level since 2021. We expect both growth and value parts of the market to contribute to earnings growth this year, which also supports the ongoing broadening of sector leadership in the stock market.

The fourth quarter 2024 earnings season is underway now, and corporate earnings continue to surpass forecasts. Over 77% of S&P 500 companies have reported earnings already, and among these, 76% have exceeded expectations. This is above the 10-year average of 75% and in line with the five-year average of 77%. While there have been some high-profile misses and a focus on capital spending, particularly among the mega-cap technology stocks, the overall direction continues to support corporate earnings momentum heading into 2025.

Source: S&P 500 Earnings Season Update: February 14, 2025

Overall, despite uncertainty around tariffs and trade, the fundamental backdrop remains supportive, in our view. The economy is growing above-trend, corporate profits are rising, and the unemployment rate remains historically low – all while potential pro-growth policies may be on the way.

From a market perspective, after two back-to-back years of solid gains in the U.S., and low volatility during this period, we would expect to see moderation in returns and increased market volatility ahead. However, we continue to believe that investors can use these pullbacks as opportunities to diversify, rebalance and add quality investments at better prices across stock and bond markets.

In our view, to optimize portfolio performance, diversification will be essential in the year ahead. Diversified portfolios not only help avoid too much exposure to any one asset class that may be at risk, but they also help maintain returns when certain parts of the market are outperforming.

While we continue to urge discipline and fundamentals in the face of persistent and often elevated trade noise, BMO finds this this uncertainty has led to “select outlook paralysis” among trade-exposed industries in the TSX. From our perspective, this “paralysis” is leading to a phenomenon of very beatable earnings in the second half of the year, especially when trade issues resolve. As such, we believe investors should be looking for high-quality Canadian companies with long-term fundamental growth profiles that may have been unjustly punished during recent trade consternation.

Source: Canadian Strategy Snapshot Trade Caution = Opportunities

For example, the breadth of upward revisions to Earnings Per Share (EPS) over the last 60 days has collapsed for both the S&P/TSX Consumer Discretionary and Industrials sectors, highlighting the level of outlook paralysis that has now hit these sectors. Furthermore, sector underperformance has reached extremes, with the year-over-year relative price performance of both these sectors at/or below 1 standard deviation of historical performance. As such, we believe there are likely many opportunities within these areas.

Source: Canadian Strategy Snapshot Trade Caution = Opportunities

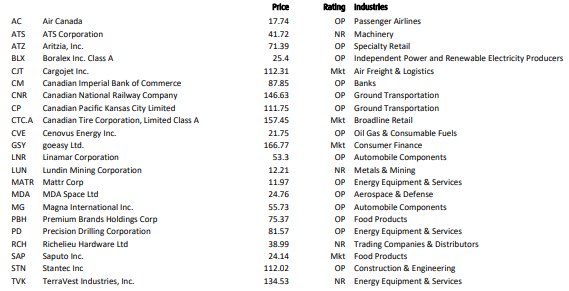

BMO’s Chief Investment Strategist Brian Belski highlighted this group of profitable (quality) Canadian companies that underperformed on the trade down days, but have positive forward growth expectations. This would suggest keeping an eye on these companies in periods of trade rhetoric.

Source: Canadian Strategy Snapshot Trade Caution = Opportunities

Source: Canadian Strategy Snapshot Trade Caution = Opportunities

While we agree that there’s some good opportunities in the names above (and we do own several in our own discretionary mandates), we continue to favor owning value, defensive and cyclical sectors as part of a diversified basket. Certain industries, like U.S. autos, are expected to be challenged if tariffs escalate with our North American trade partners, given that the U.S. is a major importer of car parts from Mexico and Canada. But the broader index is likely to hold up better than trade-sensitive sectors and international equities. Without a recession or the resumption of Fed rate hikes, we do not expect a prolonged tariff-induced market downturn. Instead, any short-term pullbacks are likely to occur within the broader bull market.

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.