Here We Go Again...

DHL Wealth Advisory - Jan 17, 2025

- Investment Services

- Portfolio Management

- Special Reports and Newsletters

- Total Client Experience

- Wealth Management

After a stuttering start to 2025, financial markets found a firmer footing this week as inflation concerns calmed...

After a stuttering start to 2025, financial markets found a firmer footing this week as inflation concerns calmed. While most of the attention is now focused on next Monday’s inauguration—and what may soon follow—this week’s market driver was a more mundane economic report. The U.S. CPI inflation report for December landed a touch below expectations on the core measure, and that was enough to break the fever in global bond markets and provide some heavy-duty support for stocks.

Source: Brave New World Order

It remains to be seen how long the reprieve for inflation concerns will last. The reality is that the U.S. economy continues to chug along, consistently surprising one and all to the high side. This week alone saw another jump in small business sentiment, a solid advance in all-important December retail sales, a pop in housing starts, and a big rise in manufacturing production. The Atlanta Fed is now tracking 3.0% growth in its US GDP forecast for Q4, and the economy clearly had solid momentum heading into 2025. All great news for investors.

Source: Brave New World Order

While the growth backdrop will undoubtedly be harmed by a trade fight, the outlook for inflation is a bit more nuanced, and will depend heavily on the degree of retaliation to U.S. tariffs. But even if others decide to take a lighter touch on retaliation, the persistent strength in the U.S. dollar will drive up costs elsewhere. Picking a nearby example, the greenback has risen by more than 7% in the past four months alone against the Canadian dollar, pressuring import prices higher. On the flip side, it’s that very run-up in the U.S. dollar that leaves us a tad skeptical that U.S. inflation will see much of a bump from tariffs, and that’s especially so if they are applied in a staged manner or imposed on only specific nations.

Source: Brave New World Order

Even so, financial markets and even the Fed seem preternaturally calm over the very real prospect of “serious” tariffs. Fed Governor Waller has suggested that the inflation impact on the U.S. would not be significant, and would be temporary in any event (i.e., a one-time hit), so the Fed would look past it. It’s not clear if that’s a widespread view among Fed officials, but Waller is certainly leaning more dovish than others more broadly. He again asserted this week that rate cuts are still quite possible in coming months, even if a pause is all but certain at this month’s meeting.

Source: Brave New World Order

Where does this shifting global backdrop leave the Bank of Canada? In stark contrast to widespread expectation that the Fed will pause on January 29, the Bank is still mostly expected to trim again that day. (Sidebar, we will point out that no fewer than five BoC decision dates fall on the same day as the FOMC meetings this year; that’s more times than the two have coincided over the past 20 years.) While the debate in the U.S. is all about how much inflation tariffs may cause, the only question in Canada is how much growth damage they will inflict. As a result, the Bank seems poised to continue cutting despite:

• The recent 7% drop in the Canadian dollar to near 20-year lows.

• The widespread assumption that the Fed will pause.

• A robust employment report for December, which even saw the jobless rate dip.

• More signs that the domestic economy is responding with purpose to prior rate cuts, including a 19% y/y rise in home sales last month, and a pick-up in mortgage borrowing trends.

Source: Brave New World Order

Canada’s own CPI report for December may provide a bit of home-grown support for rate cuts. The GST holiday, which began mid-month, is expected to help clip headline inflation to 1.8% (more than 1 ppt south of U.S. trends), while favourable base effects may also help shave the yearly core readings. But, ultimately, the Bank’s decision may come down to what unfolds on the tariff front.

Source: Brave New World Order

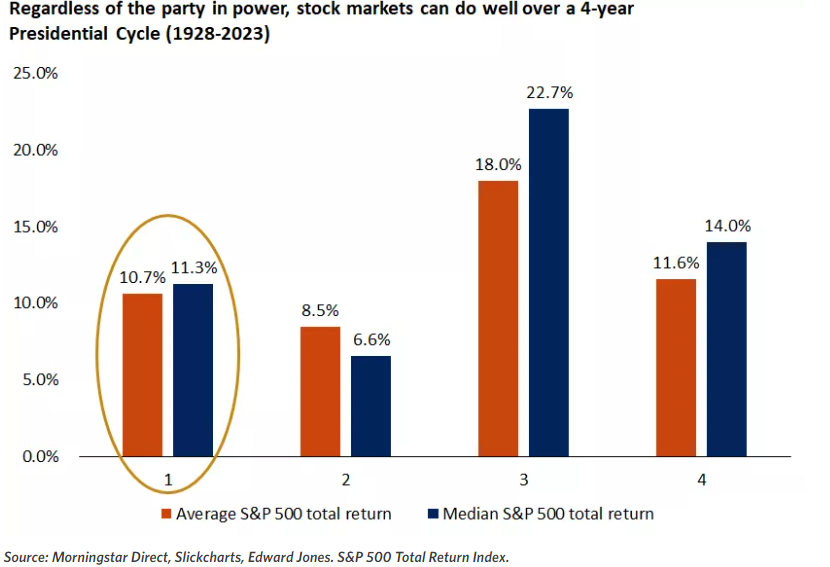

Lastly, with the looming inauguration of Trump 2.0, this is a great time to remind our readers that financial markets tend not to be driven by politics and headlines, but by fundamentals.

We continue to see the economic and market expansion being supported by three key fundamental factors: A solid labour market, which continues to support consumption; positive S&P 500 earnings growth, which will likely reach over 10% in 2025; and central banks that will still move policy rates lower from here.

Remember, after two back-to-back years of solid gains in the U.S. and Canadian markets, and low volatility during this period, we would expect to see some moderation in returns and bouts of increased market volatility ahead. However, we continue to believe that investors can use these pullbacks as opportunities, to diversify, rebalance and add quality investments at better prices, across both growth and value parts of the market.

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.