A New Axis of Evil, Eh.

DHL Wealth Advisory - Jan 10, 2025

- Investment Services

- Portfolio Management

- Special Reports and Newsletters

- Total Client Experience

- Wealth Management

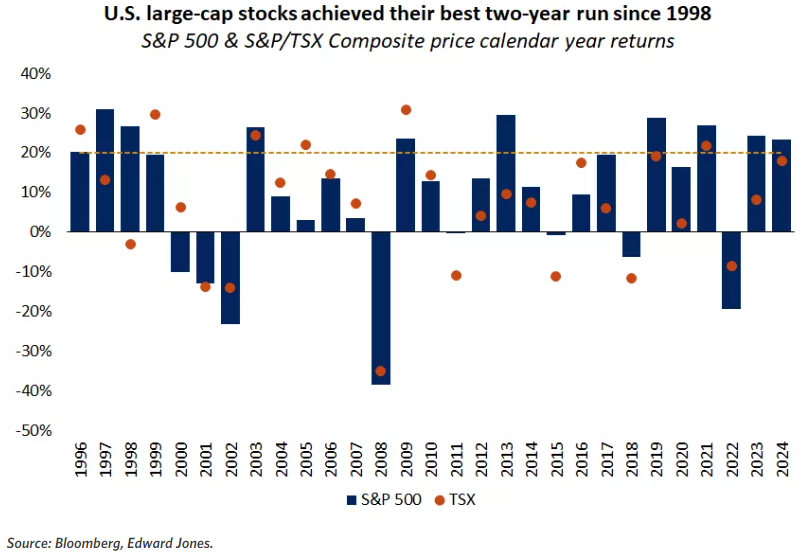

Despite an underwhelming end, 2024 proved to be a stellar year for investors. The TSX gained 18% and the S&P 500 achieved its second consecutive year of 20%-plus performance for the first time since 1998...

Despite an underwhelming end, 2024 proved to be a stellar year for investors. The TSX gained 18% and the S&P 500 achieved its second consecutive year of 20%-plus performance for the first time since 1998. U.S. mega-cap tech led the way, but portfolios enjoyed solid gains across sectors, styles and market caps. Now that 2024’s strong performance is in the rearview mirror, it’s natural for investors to ask if the good times can continue.

We think 2025 will bring a mix of headwinds and tailwinds along with some policy uncertainty around tariffs and interest rates. But ultimately, we believe stocks and bonds can build on 2024’s gains, as the main drivers that propelled the stock market higher over the past 12 months appear poised to continue. The key pillars of this positive stance are: a) a low probability of recession in the next year (just take a look at today’s jobs report on both sides of the border); b) strong corporate earnings momentum (double-digit growth projected in the U.S. and Canada); c) a relatively favourable inflation and interest rate environment; and d) still reasonable valuation and dividend growth potential for a number of sectors and individual stocks (especially in Canada).

Source: Investment Strategy

At the same time, investors should not underestimate the risks of a Trump-led tariff war and the high valuation for the U.S. stock market (particularly in the Tech and Communication sectors), along with the extreme concentration we are seeing with the top 10 largest U.S. companies comprising more than a third of the S&P 500’s value (a level only matched during the 1970s “nifty-fifty period”).

Source: Investment Strategy

While both markets did well in 2024, the U.S. once again managed to outperform given the country’s huge edge in productivity growth and the S&P 500’s much higher exposure to the Artificial Intelligence theme which has captured investors’ imagination. However, we are seeing sector leadership broaden out and the S&P/TSX remains far cheaper, and the sector weights are more favourable in the context of a “soft landing” scenario (Financials, Industrials and Energy Infrastructure, in particular). Also, the prospect of a new Government with a more sensible economic vision could act as an important catalyst for foreign and domestic investors.

Source: Investment Strategy

With respect to specific areas of the market, Defensive/interest rate sensitive sectors like Utilities, REITs, and Financials should continue their recovery if we are right in our view that long-term interest rates are unlikely to spike up significantly from current levels. As for shorter-term rates, both the Bank of Canada (“BoC”) and the U.S. Federal Reserve (“Fed”) remain in easing mode which has historically been a good tailwind for equities. We believe this is true despite the Fed recently indicating a slower path of interest rate cuts in 2025 relative to overly optimistic trader expectations. Also helpful is that the yield curve is steepening (meaning 10-year rates are now higher than the 2-year rate) which has historically been a good omen for stocks.

Source: Investment Strategy

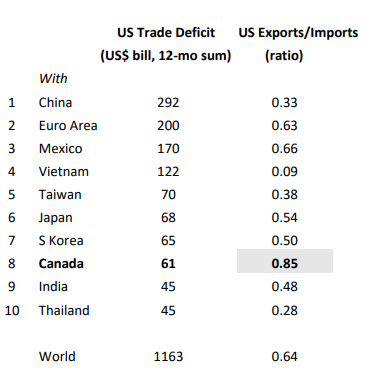

Diving into the Trump tariff threat a little deeper, it’s worth reiterating that Canada is really NOT the issue when it comes to the US Trade Deficit. You’ve likely heard a lot about this in recent weeks, but here’s the hard data: Per U.S. figures, over the past 12 months to November, the total U.S. goods trade deficit was US$1.16 trillion, of which Canada accounted for all of 5% (a bilateral gap of US$61 billion). Among major trading partners, that only ranks as the eighth-largest imbalance—even as Canada is the #1 U.S. export destination. And, the Canadian surplus is entirely due to energy trade.

Source: U.S. Trade Deficit: Canada is Really NOT the Issue

Also note the right-hand column in the figure below, which considers the ratio of U.S. exports to imports. Its global ratio is 0.64, while with Canada the ratio is 0.85—by far the highest tally (or the most equally balanced trade) among the 10 largest trading partners. Mexico is second “best” among this group at 0.66.

Source: U.S. Trade Deficit: Canada is Really NOT the Issue

Source: U.S. Trade Deficit: Canada is Really NOT the Issue

A couple sidenotes:

1) The combined shortfall with Mexico and Vietnam, the two most obvious beneficiaries of trade diversion from China, is now precisely the same as that with China ($292 billion).

Source: U.S. Trade Deficit: Canada is Really NOT the Issue

2) The export/import ratio with Vietnam is not a typo! The U.S. deficit with that nation has quadrupled in the past 8 years, as production has aggressively shifted there from China.

Source: U.S. Trade Deficit: Canada is Really NOT the Issue

No doubt 2025 will bring its own twists and turns in the market narrative, but there remain reasons for optimism as we enter the new year. We still see a Fed and BoC that want to gradually ease policy, while the labour market is healthy and economic growth solid. In fact, unemployment rates just dropped on both side of the border with this morning’s big jobs beat. Meanwhile, valuations have risen and policy uncertainty is high, but that should not preclude corporate profits from rising, providing fuel for further gains.

While we recommend staying invested to participate in the broader expansion, investors should: 1) rebalance appropriately to ensure proper diversification to help navigate the bumps along the way, 2) calibrate realistic expectations for volatility and more moderate gains as we advance.

The upshot is that fundamentals remain healthy, pointing to a solid handoff to the new year. While it may not be a smooth ride, we believe equities have the potential to build on their strength as market leadership continues to evolve.

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.