The Year of the Pooh.

DHL Wealth Avisory - Nov 29, 2024

- Investment Services

- Portfolio Management

- Special Reports and Newsletters

- Total Client Experience

- Wealth Management

North American markets were higher on the holiday shorted week. News flow was quiet given the Thanksgiving Holiday to the south, but markets rallied on with new highs on both sides of the border...

North American markets were higher on the holiday shortened week. News flow was quiet given the Thanksgiving Holiday to the south, but markets rallied on with new highs on both sides of the border. Last week we touched on the 2025 US Market Outlook of BMO’s Chief Investment Office Brian Belski. This week we’ll highlight his outlook for Canada.

Last year, Belski’s 2024 Market Outlook for Canada was titled “The Return of ‘Tigger’” as he believed AND still believes Canada is well positioned to shift from a more timid/defensive “Eeyore” environment to an offensive “Tigger” market (excuse the Winnie the Pooh references). Indeed, after over a year of depressed valuations and sluggish relative performance, Canadian equities finally caught a bid in the second half of 2024, with the TSX hitting new all-time highs for the first time since early 2022. Overall, Belski believes that the Canadian recovery trade remains in its early stages, with Canada set to hit new all-time highs throughout 2025.

Source: Belski - Investment Strategy - 2025 Market Outlook: The Year Ahead for the US and Canada

In his opinion, the core drivers and fundamental underpinnings behind Canada’s stock market recovery in 2024 are likely to continue to define 2025 Canadian equity performance. As such, as monetary policy continues to ease, equity flows broaden out and earnings growth converges with the US, he believes the TSX can, and will, attain higher prices with a 2025 year-end price target of 28,500/ This represents an over 10% annual return.

Source: Belski - Investment Strategy - 2025 Market Outlook: The Year Ahead for the US and Canada

Belski highlights five key performance drivers of the TSX over the last six months that will follow through into 2025:

1. 2025 = Continued Valuation Expansion With a Dose of Downside Protection

Yes, Canada continues to offer asymmetric upside, in our opinion. As we have written about extensively, valuation normalization favors Canada longer term, a process that should also add downside protection during periods of heightened volatility. While valuations have started to NORMALIZE and have now passed their long-term historical averages, Belski believes there remains significant breadth of absolute and relative value in Canada. In fact, his work shows that almost all TSX sectors have valuations below their US peers, with many sectors still at, or below, historical valuation levels. As such, while he does not expect Canadian valuations to reach the AI-driven heights of the US, Canada is likely to continue to see valuation expansion above historical averages throughout 2025 with a narrowing of valuation spread versus the US. YES, Valuation Remains a Key Advantage for the TSX in 2025.

Source: Belski - Investment Strategy - 2025 Market Outlook: The Year Ahead for the US and Canada

2. 2025 = Earnings Rebound and Converging Growth Profile

From Belski’s perspective, while the bulk of the earnings recovery he expected in 2024 was pushed out to 2025, this improving growth profile and increasing analyst confidence will remain a key fundamental support to drive the TSX higher in 2025. As such, as the reality of a more resilient economy, lower interest rates, and rebounding earnings growth continue throughout 2025, he believes valuations will continue to expand with the TSX attaining successively higher prices. Furthermore, as part of the normalization process, he believes the Canadian growth profile will converge with the US in 2025, thereby being a key catalyst for valuation convergence with the US as well. YES, Rebounding Earnings Growth Will Be the MAIN Driver of TSX Stock Returns in 2025.

Source: Belski - Investment Strategy - 2025 Market Outlook: The Year Ahead for the US and Canada

3. 2025 = Broadening Performance Will Continue to Benefit Canada

The broadening out of equity performance that we saw in the second half of 2024 will continue to benefit Canadian equities heading into and in 2025. While there will certainly remain ebbs and flows of performance concentration within the US mega caps, ultimately, Belski believes performance will broaden, which will remain a key tailwind for Canadian equities. In fact, the TSX has been highly correlated to both the S&P 500 equally weighted index and US SMID Cap names. As such, as US performance broadens away from the mega caps into smaller and lesser-known names, Canada will likely continue to participate.

Source: Belski - Investment Strategy - 2025 Market Outlook: The Year Ahead for the US and Canada

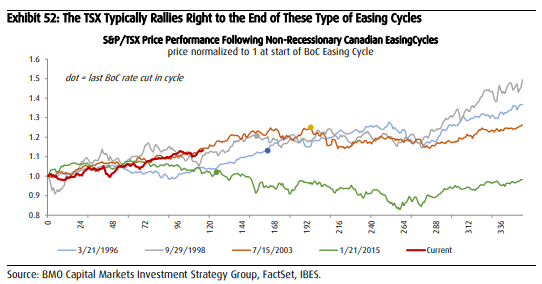

4. 2025 = Easing Environment to Remain Tailwind Throughout 2025

With inflationary trends continuing to ease, the Bank of Canada clearly remains in an easing cycle. As we ourselves have highlighted many times, we believe this is a “proactive” non-recessionary easing cycle that is likely to remain a strong positive catalyst for TSX performance right until the end of the easing cycle and possibly beyond. Based on these more proactive easing cycles, the TSX has historically rallied right to the end of the cycle, only pausing briefly after the last rate cut as markets adjust to shifting rate expectations. Overall, even though rate cuts expectations will likely shift over the course of the year, economists are largely aligned that the trend is for lower policy rates well into 2025. As such, the easing cycle will likely remain a key tailwind for the TSX in 2025 and is likely to propel strong performance throughout the year.

Source: Belski - Investment Strategy - 2025 Market Outlook: The Year Ahead for the US and Canada

5. 2025 Wild Card = Positive Equity Flow Potential

While this is certainly a much slower moving variable and a wild card for 2025, Belski’s works shows significant “pent-up” demand for positive equity flows. Indeed, foreigners have been clear net sellers of Canadian equities for two consecutive years; however, the pace of selling has started to slow and could reverse to net buyers in 2025. In fact, history shows rebounds in foreign flows are highly correlated with TSX relative performance. Additionally, domestic investors have seen a sharp increase in money market and cash investments as GIC rates increased. However, as rates continue to trend lower, investors generally begin to redeploy these elevated cash positions into Canada equities, particularly into the more income intensive areas of the market. Overall, he believes increasing positive equity flows, both foreign and domestic, is a key positive wild card for 2025.

Source: Belski - Investment Strategy - 2025 Market Outlook: The Year Ahead for the US and Canada

The rally seen in late 2024 was better late than never, as the TSX saw a sharp rebound in equity flows with valuations rebounding back to historical averages. Indeed, many of the economic and market fears that plagued Canadian stocks for the past two years have dissipated as the Bank of Canada became increasingly aggressive “normalizing” interest rates. With this overhang now removed from the market, 2025 is likely to be a more normalized market, driven primarily by fundamentals and rebounding earnings growth. Overall, we believe 2025 will be a continuation of the second half of 2024, particularly as confidence in the earnings outlook continues to improve and flows return to Canadian equities. Our base case assumes stable commodity prices, a growth profile that will converge to the US and continued improvement in the earnings multiple above its long-term historical average. In our view, the economic and market fundamentals provide a supportive backdrop heading into 2025, pointing to a solid handoff to the new year. While it may not be a smooth ride, we believe equities have the potential to build on their strength as market leadership continues to evolve.

Source: Belski - Investment Strategy - 2025 Market Outlook: The Year Ahead for the US and Canada

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.