Today's Content Is Not To Be Discussed At the Dinner Table

DHL Wealth Advisory - Oct 25, 2024

The six-week stretch of record gains finally came to an end this week as market attention begins to really focus on the upcoming US Presidential Election. The stock market had been on quite a run prior to this week, rallying more than 12%...

The six-week stretch of record gains finally came to an end this week as market attention begins to really focus on the upcoming US Presidential Election. The stock market had been on quite a run prior to this week, rallying more than 12% just since early-August and extending its year-to-date return to nearly 23%. If the S&P 500 holds on to this gain for the remainder of 2024, this will be the second consecutive year with a return of 20% or more.

The strength of this market over the last two years has not been by luck. Instead, it's been powered by the "big three" fundamentals: a growing economy, a more friendly interest-rate policy outlook, and rising corporate profits. We wrote to this in our last week’s edition and, of course, everyone read that report so there’s no point in reading old news. Instead, this week we are going to focus on the elephant in the room. US politics.

With about 10 days to go before we know the next US President (well, we hope 10 days…), contentious and unusual have become the campaign norm in the lead up to the past few general elections as has the great deal of investor uncertainty regarding US stock market performance implications stemming from the eventual winner. There is always much debate surrounding which party is better for US stocks particularly given the hyper-polarization of US politics lately. However, we have found through our years of work that the US stock market tends to go up over time whether a Democrat or Republican is in the White House, and it is ultimately the direction of a free market, capitalistic economy, not politics or government policy, that dictates stock prices.

Nonetheless, we thought it would be useful to provide some market performance context for all potential scenarios that could occur based on upcoming election results. The analysis suggests that the oft-feared “blue wave” is not as scary as some investors make it out to be, while a Trump victory is no guarantee of continued market gains.

Main Points:

- The stock market has performed better under Democratic Presidents, on average

- Despite perceptions, gridlock is not necessarily always good for US stocks

- Monetary vs. fiscal policy has a more direct positive impact on stock market returns

- Longer-term market performance has not been significantly impacted by tax policy

Source: US Strategy Comment: Election Outcomes and US Stock Market Performance

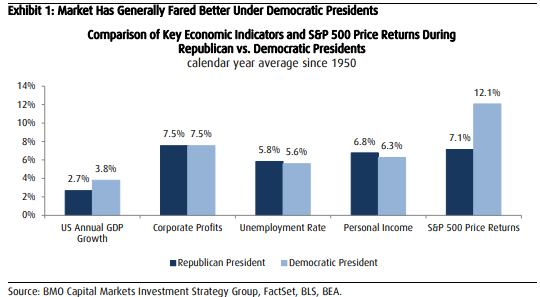

Democrats Have Been Better for the Market and Economy, Historically: Whether it is by coincidence or causation, historical evidence suggests that the market and economy perform better under Democratic presidential leadership. As Exhibit 1 shows, GDP growth has been much more favorable under Democratic control while market performance has been about 5% higher, on an annualized average basis. Interestingly, corporate profit growth has been about the same regardless of who is in office – a direct contradiction to the popular belief that Democrats pursue profit limiting policies – with similar trends in unemployment and personal income data. This suggests that the keys areas of the US economy – corporate profits, employment levels and the health of the consumer – are ultimately determined by economic cycles, not presidential cycles or government policies.

Source: US Strategy Comment: Election Outcomes and US Stock Market Performance

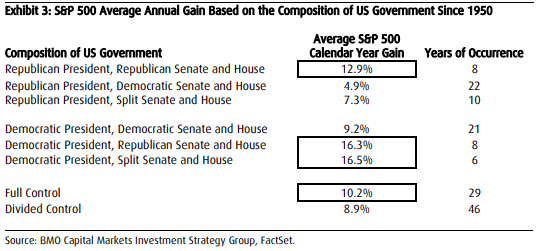

The “Gridlock Is Good” Adage Is Not Necessarily Accurate: A fair number of investors subscribe to the view that political gridlock is good for stock market performance. From our perspective, the most common theme from those who favor political gridlock is that the divide is good for growth since gridlock should lessen government interference in the private sector. While we understand this point of view and tend to agree to a certain extent, we believe the reality is a bit more complicated. As shown in Exhibit 3, the analysis reveals that at a very broad level (i.e., full vs. divided control), the market tends to perform a bit better when one party controls all three branches of government. Coincidentally, the highest average returns during full control years have come under Republican leadership, although that scenario has only occurred in eight years since 1950. In fact, the best years of market performance have occurred under Democratic presidents with Republican Senate and House majorities or split control of the chambers, while the worst years have occurred under Republican presidents with Democratic Senate and House majorities or split control of the chambers.

Source: US Strategy Comment: Election Outcomes and US Stock Market Performance

Monetary Policy Has a More Direct Impact on Stock Market Performance: Monetary and fiscal policy generally share the common goal of sustaining economic growth. The effectiveness of each can vary significantly based on the context, but empirical data suggest that both tend to work best in tandem to achieve this common goal. However, when it comes to implications for stock market performance, historical data suggests that monetary policy has had a more direct and quicker impact.

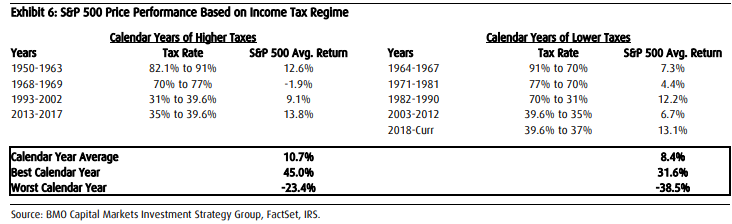

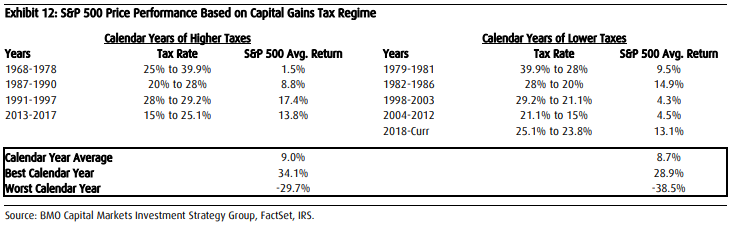

Higher Taxes Have Not Impeded Market Gains Historically: The prospect of any sort of tax increase has always spooked investors since the perception is that higher rates would impede stock market performance potential. We understand the consternation, nobody wants to pay higher taxes, but the prevailing wisdom that tax hikes destroy markets is misguided if history is any sort of guide. And by contrast, there has been little proof of lower taxes improving market gains. Indeed, according to historical changes in the individual, corporate and capital gains top tax rate, the stock market has generally performed better during periods of higher, not lower, tax rates across changes in all three categories.

Source: US Strategy Comment: Election Outcomes and US Stock Market Performance

Bottom line is that generally there’s a lot of noise and unwarranted volatility around elections. To much surprise, we have been largely spared that thus far in 2024, but if large swings do indeed ensue, it’s important to remember the above points. In times of volatility, remove the noise and look to facts and historical data/precedent, all of which suggests that whatever follows in the coming weeks, it doesn’t have an impact on the big three fundamentals. All of which remain healthy and intact.

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.