Time To Hit The Panic Button? And We're Talking About The Canucks...

DHL Wealth Advisory - Oct 18, 2024

For the 47th time of 2024, the S&P 500 hit a new all-time-high. There wasn’t a whole lot moving markets higher this week as investors begin to digest the start of 2024’s last earning season...

For the 47th time of 2024, the S&P 500 hit a new all-time-high. There wasn’t a whole lot moving markets higher this week as investors begin to digest the start of 2024’s last earning season. It did start off with a bang with better-than-expected results out of major US Financials like Morgan Stanley and JP Morgan. Of note, Taiwan Semiconductor, the world’s largest chip producer, beat third-quarter earnings estimates and posted a 54% increase in profit. The company produces chips for companies such as Apple and Nvidia. Naturally these results lifted sector sentiment with both those companies also hitting new all-time-highs.

Source: S&P 500 to hit 'well north' of 6,000 by the end of 2024 amid stock FOMO: Goldman

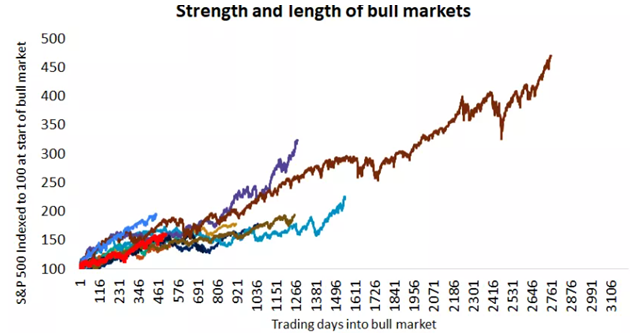

It's worth highlighting that this past weekend marked the 2-year anniversary of the October 12, 2022 bear market low. With the recent rally and valuation surpassing expectations, we have fielded a lot of questions of late that there is no-longer much value in markets. We strongly disagree…

Before we get to that, let’s take a walk down memory lane… Two years ago, on October 12, 2022, inflation was above 7% in Canada and the U.S., central banks were in the midst of a historically aggressive rate-hiking campaign, and the S&P 500 had dropped 25% off its high. However, as is often the case, widespread pessimism at the time gave way to a new bull market, which continues to this day. Since then, stocks have gained 60% in the U.S. and 35% in Canada. Today, inflation in Canada is sub 2% and nearing 2.5% in the US. Meanwhile, global central banks are in a synchronized interest rate cutting cycle.

Source: One is No Longer a Lonely Number

You might say a 60% return out of the S&P is a lot in the first 2 years of a bull market? The answer to that might be surprising. In fact, it is right in line with the historical average of the past 11 bull markets going back to 1957. Given its lower exposure to technology and the lagging economic momentum, Canada’s TSX has underperformed the S&P 500 but the index continues to make a series of new highs this year, participating in the global rally.

Now, what’s next? Geopolitical uncertainty and the U.S. election might be sources of short-term volatility, but history offers reasons for optimism. The average duration of the last 11 bull markets has been nearly five years, with most of them (eight out of 11) making it to the end of the third year. This suggests that the current bull might still be in its early or middle phase. However, year three might not be a smooth ride. Returns tend to moderate, with stocks advancing only half the time, while in the other half stocks pulled back to catch their breath. From a fundamental perspective, it will be the outlook for growth, interest rates and corporate profits that will likely determine outcomes. So, let's dive into these factors.

Source: One is No Longer a Lonely Number

In the first half of 2022 the U.S. economy hit a soft patch, experiencing a mild contraction in the first quarter and barely positive growth in the second quarter. But since then, GDP growth has been averaging a strong 3% over the past two years and is on track to post a 3.2% gain in the third quarter. Forecasts are for U.S. growth to slow in the quarters ahead toward a pace consistent with or slightly below the economy's long-term potential rate, which is considered to be around 2%, based on labor force and productivity growth. A slowing but still growing economy can provide a favorable foundation for corporate profits to continue to rise, which in turn can help sustain the bull market. In Canada growth will likely remain muted in the remainder of the year before likely starting to rebound in the second half of 2025 as the BoC's rate cuts start to filter through the economy.

Source: One is No Longer a Lonely Number

On interest rates, it’s no coinciding that the market bottomed around a peak in inflation. Last month the Fed made a decisive step in starting to normalize its policy rate by delivering its first rate cut of this cycle, lowering interest rates by a larger-than-typical half a percentage point (0.5%). While last week's inflation came in slightly hotter than expected, it's unlikely to stop the Fed from continuing its easing campaign, as it has now shifted its focus from inflation to the labor market. As US inflation inches to 2%, the Fed will want to gradually remove its restriction and keep the chances of a soft landing alive.

Source: One is No Longer a Lonely Number

Now, to corporate profitability. Driving the nearly 60% stock-market gain has been a combination of growth in corporate earnings and valuation expansion. More specifically, S&P 500 profits have risen about 15% over the past two years, reaching new records. While the market gains in these two years are right in line with the average bull-market gains, the asset class, style and sector leadership are in many ways unique. When examining the past 11 bull markets, this is the only time off a two-year low that the "average" stock, as proxied by the S&P 500 equal-weight index, has not outperformed the market-cap weighted index. We have also seen the biggest outperformance of growth-style investments relative to value, as excitement around artificial intelligence has boosted valuations for the mega-cap tech stocks, leaving other parts of the equity market behind. To this end, the small-medium cap (SMID) gains have been less than half of what is typically observed at the start of a new bull. These “SMID” areas of the market are areas where we see considerable upside potential.

Source: US Strategy Comment: When Will SMID-Cap Get Investor Attention?

The bottom line is that investor pessimism, growth concerns, and uncertainty around inflation two years ago have given way to economic resilience, easing price pressures, and excitement around artificial intelligence, marking the transition to a new bull market. As the old adage goes, bull markets don't die of old age, but from a recession, overly tight Fed policy, or an external shock. The latter is impossible to predict, but with the odds of a recession decreasing and the Fed embarking on a rate-cutting cycle amid a healthy labor market, we expect the bull market to continue into its third year.

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.