Not Since Tom Hanks Botched A Moon Landing...

DHL Wealth Advisory - Sep 27, 2024

So much for all the fuss about September being the worst month of the year for markets…

So much for all the fuss about September being the worst month of the year for markets… Global benchmarks continued their march to record highs this week on the coattails of last week’s larger-than-expected rate cut out of the US Federal Reserve and a big stimulus package out of the world’s second largest economy in China.

Coming into the month we wrote that September is the most challenging month of the year for equities. In the past 25 years, the S&P 500 has declined 14 times in September, with an average performance of a sickly -1.7%, and is currently on a four-year losing streak for the month. The TSX has done it one better, falling in 15 of the past 25 Septembers, with an average price change of -1.8% for the month. This year, after seemingly sticking to that historical script for the first week, stocks have since gone rogue, with many major averages at all-time high this week. The reason we are recapping this is that it speaks to one of the important principles of investing: It’s rarely wise to try and time the market…

BMO Economics Talking Points: Goldilocks and the Wee Bears

The proximate cause was clearly the Fed’s mildly surprising 50 basis point cut, which the market had really only begun to seriously price in as the meeting approached. The direction of travel was hardly a surprise, as Chair Powell had already signaled the start of rate cuts last month at Jackson Hole. The drop in the consumer price index (CPI) from a peak of 9.1% in June 2022 to 2.5% in August has given policymakers greater confidence that inflation is moving sustainably toward 2%. At the same time, the increase in the unemployment rate from 3.4% to 4.2% is a reminder that the Fed has a dual mandate, not only to achieve price stability but also maximum employment. As a result, the Fed has officially shifted from a laser-like focus on inflation, to equal concern on the softer job market.

BMO Economics Talking Points: Goldilocks and the Wee Bears

We think that the larger cut highlights the Fed's commitment to not fall behind the curve by keeping policy overly restrictive for too long. Partly it was a catch-up move, as Powell suggested that a cut might have occurred in July if the Fed had the jobs data for that month in hand (the July jobs report was released on 8/02, two days after the 7/31 Fed decision). That said, Powell made clear that 0.5% cuts are not the norm, and smaller cuts remain the baseline for the upcoming meetings.

BMO Economics Talking Points: Goldilocks and the Wee Bears

In fact, the last three times the Fed cut by 50 basis points there was a lot more going on with the economic backdrop: 2020 in response to the pandemic; 2008 in response to the financial crisis; 2001 in response to the popping of the tech bubble. Clearly this time is different in the sense that the Fed is cutting rates because it can, not because it has to. The larger cut is not in reaction to recessionary conditions but rather an insurance against an unexpected slowdown in employment, with a goal to preserve the economic expansion.

We think the Fed's proactive approach increases the likelihood of a soft landing, which has been our base-case scenario. While the impact of last year's rate hikes will continue to be felt for a while longer, economic conditions appear more helpful than hurtful, as interest-rate relief is on the way: 1) Consumer spending is still robust, as last week's retail sales showcases; 2) Jobless claims are low, pointing to a cooldown rather than a sudden deterioration in the labour market, with the rise in unemployment driven by an increase in the supply of labour instead of a jump in layoffs; 3) Household net worth is at record highs, boosted by appreciating home and stock prices; 4) Wages have been growing faster than the pace of inflation since May of last year, helping consumers maintain purchasing power; and 5) Unlike in 2022 and part of 2023, financial conditions and lending standards are easing. All suggest that soft landing is not only possible but very likely.

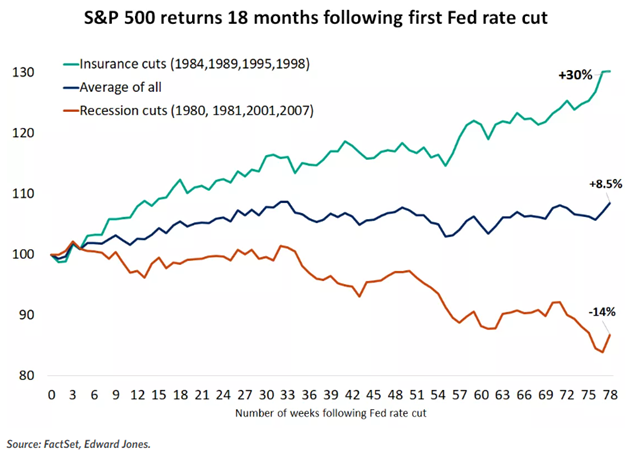

Now, what does a first cut mean for investors? The lesson from history is that equities' response to rate cuts depends on the state of the economy. The start of a rate-cutting cycle that coincides with no recession has historically led to strong equity returns 6, 12, and 18 months after the first rate decline. Examples of such instances are the cycles that started in 1984, 1989, 1995 and 1998. On the other hand, rate cuts in response to economic weakness and recession have been accompanied with losses, as in 1981, 2001 and 2007.

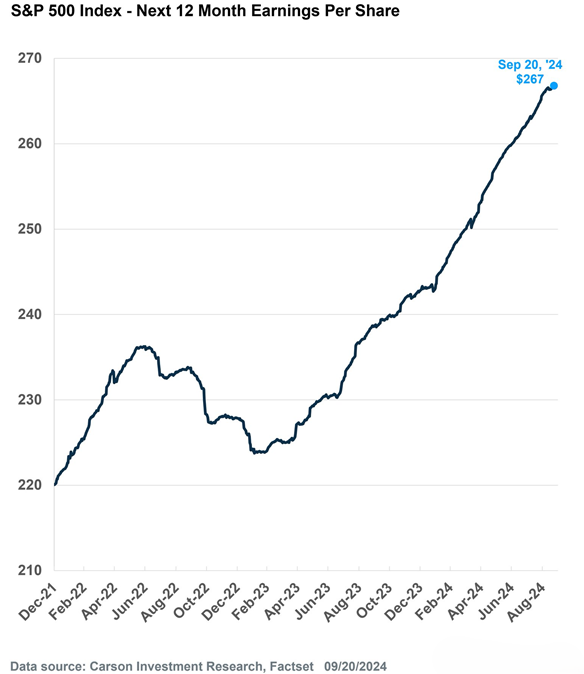

Given our above mentioned assessment of current economic conditions, we think we are tracking the trajectory of previous Fed rate-cut cycles outside of U.S. recessions, not the trajectory of recessionary rate-cut cycles. The last time stocks were at record highs when the Fed implemented the first rate cut of the cycle was in 1995 (the year Apollo 13 hit movie theaters) , and the S&P 500 went on to gain 23% in the 12 months after. Historically, valuations have tended to rise after the start of easing. In fact, when simply looking to valuations, forward 12-month EPS, which is a measure of corporate profitability has gone from $225 at the start of '23 (when everyone promised us the recession to end all recessions) and it is up to $267 now. That is not a recessionary backdrop…

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.