Happy Friday the 13th

DHL Wealth Advisory - Sep 13, 2024

Major benchmarks rebounded following a few days of choppy trading sessions fueled by economic data and the debate between the US presidential candidates, Vice President Kamala Harris and former President Donald Trump...

Major benchmarks rebounded following a few days of choppy trading sessions fueled by economic data and the debate between the US presidential candidates, Vice President Kamala Harris and former President Donald Trump. While it was difficult to separate election-fueled shifts from macroeconomic-driven moves in rates and stocks following Wednesday’s anticipated U.S. August CPI report, investors pointed to a few corners of the market that appeared to have been impacted by the debate. Shares of Trump Media & Technology Group (DJT), which has turned into something of a Wall Street weathervane about the former president’s election prospects, fell as much as 17% Wednesday morning. Cryptocurrency-focused companies were also down and 10-year Treasury yields have slipped a bit further to 3.63%, suggesting the market believes the Democrats’ chances of winning the election may have risen, leading to less fiscally-stimulative policies than proposed by Trump.

On the economic front, Wednesday’s U.S. CPI report was taken in stride, with core inflation holding at 3.2% y/y, slowing to 2.7% annualized over the latest six months, and to 2.1% over the latest three months. Good enough to confirm that the Federal Reserve will cut rates next week, but perhaps not enough to argue for a 50-bp move.

Source: BMO Economics AM Notes: September 12, 2024

The widely expected cut next week would mark the first move since the Fed has held the target rate steady for over 12 months and it will be the first cut since they dropped it to essentially zero during the early days of the pandemic in 2020. We identified eight easing cycles going back to 1982 when the Fed started officially announcing its policy actions. According to our analysis, the S&P 500 delivered positive returns in the 12 months following the initial rate cut for six of the eight cycles with an average gain of 11.3%. However, the macro context behind the moves mattered a great deal, which is why performance varied so significantly around these turning points ranging from -23.9% to 32.1%. In cycles where rate cuts were able to prolong economic expansion and keep corporate earnings on an upward trend, stocks performed quite well. However, in cycles where monetary stimulus was unable to prevent an economic downturn (i.e., 2001 and 2007), stocks recorded significant losses in the following year as earnings growth struggled. Fortunately, the current environment appears to fall into the former category. Yes, labor markets are certainly cooling, but jobs are still being added at a modest rate and leading job indicators (i.e., jobless claims) remain well-behaved. In addition, GDP is still tracking slightly above trend according to the GDP Now estimate from the Atlanta Fed, while S&P 500 earnings are expected to grow at a double-digit clip for all upcoming quarters through the end of 2025. Therefore, we believe investor debate about the size and depth of the upcoming easing cycle somewhat misses the point - so long as nothing breaks in the economy, US stocks remain firmly within a bull market, but with significantly strong trailing one-year performance headed into this initial rate cut, future gains are likely to be more muted relative to historical norms, in our view.

Source: US Strategy Comment - Initial Fed Cuts and Market Performance

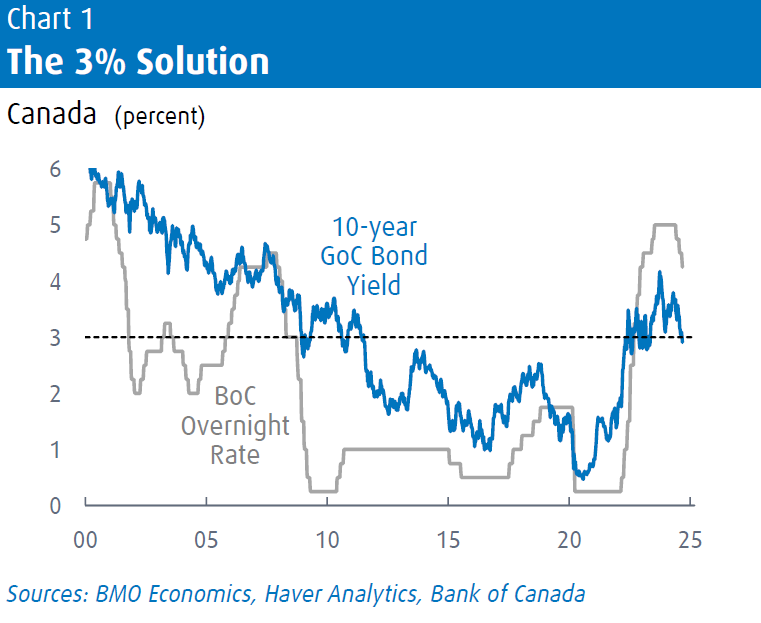

In Canada, we now expect the 3% overnight rate level to be breached, and probably more forcefully, and almost certainly much sooner then the U.S. We are adding two additional 25 bp cuts in the first half of 2025, and now see the Bank on a forced march of seven consecutive quarter-point rate cuts (after the cuts at the past three meetings). That combination of 10 consecutive 25 bp cuts will exactly slice the overnight rate in half from its prior peak of 5.0% to 2.5% by July of next year. The key change there is we now see the Bank taking the rate below what we consider to be neutral (closer to 3%), and that change has been prompted by the run-up in the jobless rate to 6.6%. Two weeks ago, we asked: “After all, if the jobless rate keeps rising, and the output gap keeps widening, while inflation is better behaved, why would the Bank stop at 3%?” And the only answer we can come to is that they won’t. Like the Fed, the risk is clearly that the Bank will proceed even more quickly than we expect, and Governor Macklem himself mentioned in his London speech that “if inflation is weaker than we expect, it could be appropriate to lower rates more quickly.”

Source: BMO Economics Talking Points: Time Has Come Today…

With the BoC well underway, the equity market has been quietly staging some significant rallies in rate-sensitive areas. Since last fall, utilities have rebounded more than 20% and higher dividend-paying equities have benefited after a few years of week performance.

Long-term inflation expectations in the market have mostly reverted to pre-pandemic norms of around 1.6%, while real yields have dipped a little below that level. The market is thus telling us in very loud terms where it considers neutral to be—below 3%—and fully expects the Bank to get there with pace. This 3% level appears to be the new normal for interest rates in Canada. While markets don’t always get it right, we’re not quarreling with this conclusion: Expected inflation and real rates have normalized after the extreme disruptions of the past five years. We look for next week’s CPI report to print just 2.2% inflation, the lowest since early 2021, and within sight of target. With ex-shelter CPI trends now running at just above 1% in both the U.S. and Canada, it’s also time to fully let go of the higher-for-longer inflation mantra. Good riddance.

Source: BMO Economics Talking Points: Time Has Come Today…

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.