Goodbye Summer; Hello Pumpkin Spice, Everything.

DHL Wealth Advisory - Aug 30, 2024

Markets spent the week largely treading water, awaiting the highly anticipated results of Nvidia. Death, taxes, and NVDA beats on earnings are three things you can bank on these days. But here’s the issue with that stock and company...

Markets spent the week largely treading water, awaiting the highly anticipated results of Nvidia. Death, taxes, and NVDA beats on earnings are three things you can bank on these days. But here’s the issue with that stock and company: The size of the beat this time was much smaller than we’ve been seeing. Even future guidance was raised, but again not by the tune from previous quarters.

More importantly, however, is that the muted reaction out of that stock was actually quite positive for the market as a whole. A day where Nvidia, which is the bellwether for AI, traded marginally lower but the broader market, especially technology and semiconductors, traded higher speaks to the broadening that we’re starting to see in this market rally.

Further, Economic data released Thursday lent support to the stock market. Weekly jobless claims fell from the prior week, further easing US recession concerns. In addition, second-quarter gross domestic product was revised higher to 3% growth from an initial 2.8% rate. So, while we continue to see a “welcomed” cooling in the labour market, the economic backdrop remains strong lending support for the US Fed to slowly begin loosening rates.

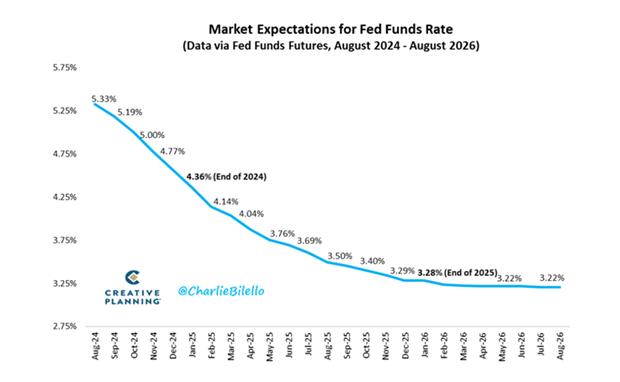

It’s no secret that markets have been fixated on – and driven predominantly by – the timeline to Fed rate cuts for the better part of the last year. The wait is almost over, as we think the commentary from Chair Powell is consistent with the prevailing view that interest-rate cuts will commence in September.

The Fed has held its policy rate steady for more than a year now, with the extended pause stemming from the fact that the central bank's dual mandate (stable inflation plus maximum employment) was not yet in a position that could warrant a change in policy settings. With the trends in inflation and employment now both on the move, and with economic growth still positive, but at a slower pace, we expect the Fed's attention will now be more balanced, with an effort to support the labor market and economy.

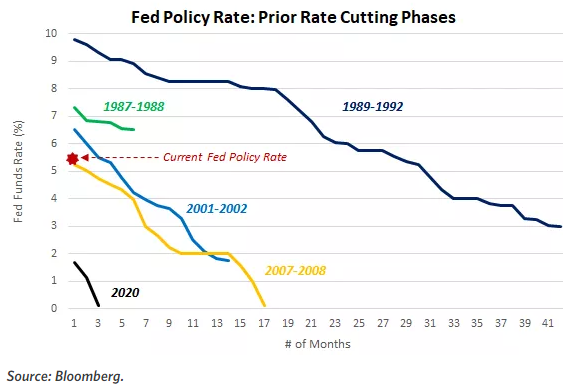

Removing the extraordinary cutting cycle that we witnessed around Covid, it’s been about 15 years since we had a “traditional” cutting cycle, so we thought a walk down memory lane would be helpful. Historically, the Fed starts cutting rates in response to an economic downturn, a financial shock/crisis, or both (Covid). The conditions are somewhat unique this time, as the Fed is not seeking to address a collapsing economy or arrest a seizing financial system. Put differently, the Fed often cuts rates to press on the gas pedal, stimulating a sputtering economy. This time around it’s more about letting off of the brake, upon which the Fed has had its foot firmly pressed for the last two years.

Given our comments above, we expect this rate-cutting cycle to start, and proceed, gradually. Barring a sharp and unexpected change in the path of inflation or unemployment, we think the Fed will make incremental, 25-basis-point (0.25%) cuts to its policy rate.

The policy-easing cycle that began in 2007 commenced with an outsized cut (0.50%) and included numerous large rate cuts as we navigated the housing market collapse and global financial crisis. Similarly, the easing cycle following the tech bubble pop and 9/11 in 2001 included numerous 50-basis-point rate cuts. We don't see a need at this stage for a dramatic move by the Fed, and in the absence of any particularly weak upcoming jobs reports, we think a string of 25-basis-point rate cuts is the likely approach, as the Fed seeks to find a neutral stance for its policy rate.

We think a shift to a phase of monetary-policy easing will be a tailwind for financial markets over the coming year. That said, this has been widely and eagerly anticipated, so a portion of that benefit has already been pulled forward into the stock and bond markets.

However, we don't think the benefits of lower rates have been fully exhausted for the stock market. The ability for the Fed to lower rates in a manner that orchestrates a soft landing for the economy (avoiding recession) should, in our view, provide scope for corporate profits to rise at a healthy clip next year, which we believe would be a fuel source for this bull market to extend this year and into 2025.

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.