The Time Has Come...

DHL Wealth Advisory - Aug 23, 2024

It was a positive but quiet week for North American benchmarks following a few weeks of outsized moves. The big event of the week came early Friday morning as US Fed Chair Jerome Powell solidified that the next move out of the Federal Reserve will...

It was a positive but quiet week for North American benchmarks following a few weeks of outsized moves. The big event of the week came early Friday morning as US Fed Chair Jerome Powell solidified that the next move out of the Federal Reserve will be a rate cut. Now, the only question that remains is will it be 25bps or 50bps.

Powell laid the groundwork Friday for interest rate cuts ahead, though he declined to provide exact indications on timing or extent. “The time has come for policy to adjust. The direction of travel is clear, and the timing and pace of rate cuts will depend on incoming data, the evolving outlook, and the balance of risks.”

With markets awaiting direction on where monetary policy is headed, Powell focused as much on a look back at what caused the inflation that led to an aggressive series of 11 rate hikes from March 2022 through July 2023. However, he did note the progress on inflation and said the Fed can now turn its focus equally to the other side of its dual mandate, namely to make sure the economy stays around full employment.

“Inflation has declined significantly. The labor market is no longer overheated, and conditions are now less tight than those that prevailed before the pandemic,” Powell said. “Supply constraints have normalized. And the balance of the risks to our two mandates has changed.” He vowed that “we will do everything we can” to make sure the labor market says strong and progress on inflation continues.

The speech comes with the inflation rate consistently drifting back to the Fed’s 2% target though still not there yet. A gauge the Fed prefers to measure inflation most recently showed the rate at 2.5%, down from 3.2% a year ago and well off its peak above 7% in June 2022.

Meanwhile, as we head into the final weeks of summer, we thought it would be helpful to highlight some key observations and trends in the market that we have been discussing or that we believe have been flying under the radar as there seems to be an inordinate amount of attention paid to index-level performance.

First, sentiment shifts have become seemingly more violent in recent weeks swinging from recession fears to soft landing expectations following every major economic data point release. Clearly the pendulum has swung in favor of optimism with the S&P 500 recovering sharply from its recent sell-off in early August and once again approaching record highs. How long this momentum can last has been a topic of debate since this bull market began in late 2022. Nonetheless, we do believe that plenty of opportunities still exist beneath the surface particularly considering improving market breadth trends in recent months. However, fundamental dispersion trends suggest that a highly selective investment approach will likely be required to identify these opportunities.

Source: US Strategy Comment: Select Observations as Summer Winds Down

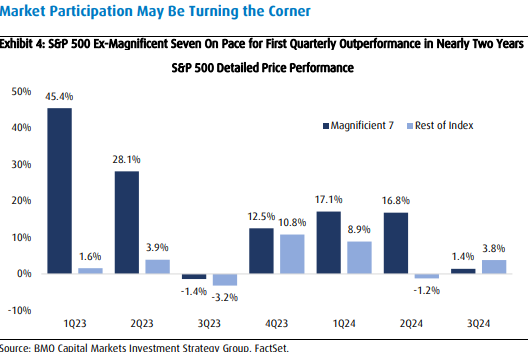

It is no secret that the so-called magnificent seven stocks have been the driving force behind market gains for much of the past two years and this has led to concentration worries amongst investors given the bloated valuations of some of these stocks. However, an interesting development has occurred alongside the most recent market rebound during the third quarter: These seven stocks have underperformed the rest of the index for the first time in nearly two years, as seen below. And this underperformance is something we find reassuring since the S&P 500 is nearing records again without this segment of the market leading the way. A broadening out of the rally has probably been our third highest talking point in 2024, trailing inflation and interest rates. We wanted to see gains in other sectors to ensure the longevity of this cycle.

Source: US Strategy Comment: Select Observations as Summer Winds Down

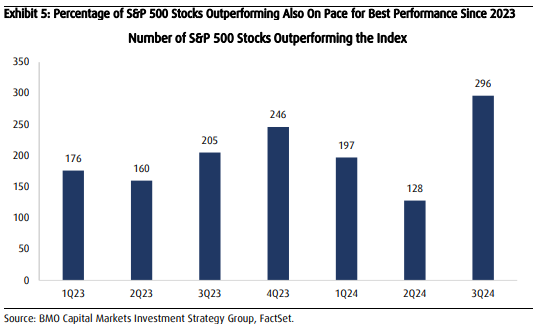

In addition, participation levels have also improved dramatically since Q3 started as nearly 300 S&P500 stocks have outperformed the broader index – the highest level in nearly two years. If the theme of the last 18 months was narrow leadership (with mega-cap technology leading the way higher), we see the theme of the next 18 months being diversification, with portfolios having both growth and value/cyclical parts of the market performing well.

Source: US Strategy Comment: Select Observations as Summer Winds Down

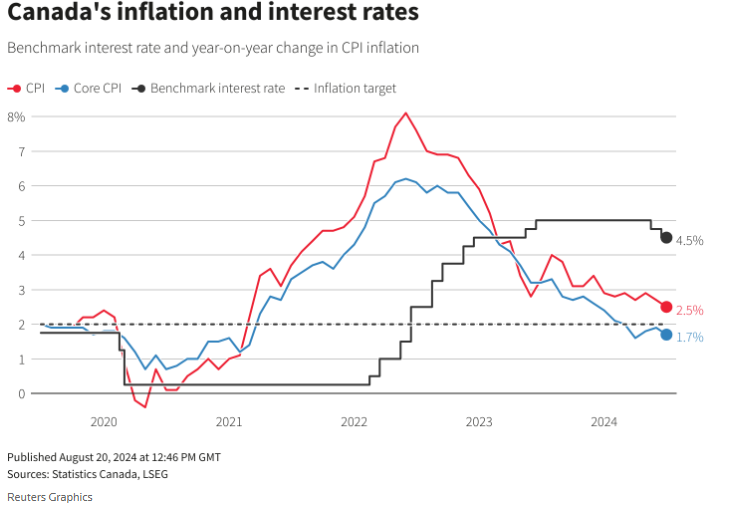

Back to our #1 talking point of 2024. This week we had Canadian Consumer Price Inflation data that came in at the lowest levels in 40 months. July inflation came in at 2.5%, matching forecasts, while core inflation measures eased as well, keeping the Bank of Canada on track to cut interest rates again in September. In fact, in addition to a September 4th cut, markets are pricing in 3 additional cuts in 2024 that would bring down the benchmark rate to 3.75% by year-end. It is worth reminding readers that we entered 2024 at a multi-decade high of 5% on the benchmark.

Overall, history tells us that if the central bank is cutting interest rates and if the economy is holding up (i.e., "soft landing"), markets can continue to perform well in this backdrop. While we know market fluctuations are normal, particularly as we are heading toward a seasonally weaker September and October – and then into U.S. elections in November – we would use these periods of volatility and pullbacks as opportunities, especially as we continue to see better inflation trends and economic growth that is cooling but still positive.

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.