K.C.C.O As The Kids Say.

DHL Wealth Advisory - Aug 16, 2024

What a difference a couple days can make…. Two weeks ago markets were in freefall following the worst 2-day stretch since covid. Now, markets are once again flirting with all-time-highs...

What a difference a couple days can make…. Two weeks ago markets were in free fall following the worst 2-day stretch since covid. Now, markets are once again flirting with all-time-highs. Last week started with a quadruple-point drop in the Dow, (more on this later) which sparked the typical parade of red chyrons and "market sell-off" headlines. The days that followed saw additional sizable swings, though they included several sharp daily gains.

We are not saying this bout of volatility should be patiently dismissed, but panic is not the proper reaction either. Market declines are never comfortable, and they can feel particularly jarring after a stretch like we have seen in 2024, as stocks were repeatedly setting new highs with almost no volatility to speak of. We think that a key to navigating - and benefiting from - a market decline is proper perspective.

Market declines of any size can feel unsettling. The 3% decline in the S&P 500 last Monday (the TSX was closed for holiday on Monday) captured significant attention and stirred an even larger amount of indigestion. But what about the 3% rally in the first several days of July? Or the better-than-2% jump in the final few days of July? Remember those? They probably don't stand out as much because, let's face it, pullbacks just hit differently. Herein lies the importance of a broader view. It should not be lost that this recent pullback was coming from a market at record levels. The frenzy of market volatility can often cause investors to forget what came before. But zooming out reveals that even with the recent drop, the stock market is still up nearly 20% over last year and 50% since this bull market began in October of 2022.

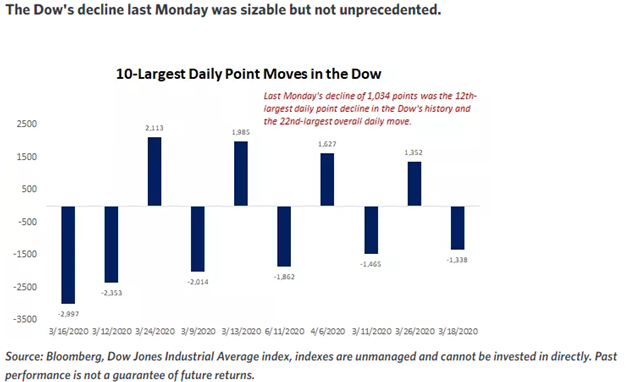

For context, Monday’s 1,034 point drop in the DOW was the 12th largest daily move in its history, but well shy of the craziness witnessed in the darkest days of covid. Remember those? We won’t blame you if you’ve intentionally blacked those out. Well, the 10 biggest days were all within a 4-week period between March-April 2020. It’s also worth pointing out that the 4 biggest daily gains coincided around/following the worst daily losses. A great opportunity in reminding readers about the difficulty around “timing the market”.

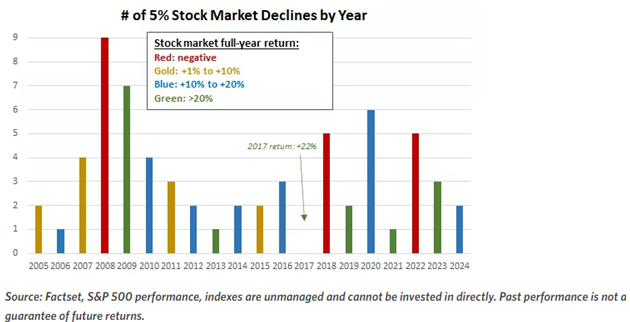

Market volatility has also been very illusive the last few years, which is something we wrote about several weeks ago. We have been in surprisingly tranquil environment since the most recent bear market low in October 2022. In fact, over the last quarter-century, we get an average of three 5% pullbacks a year. Something that occurs that frequently should not feel like a shock.

If we widen out a bit and look at market corrections of 10% or more, they're less frequent, but hardly a rarity. Over the last several decades, on average, we've experienced roughly one 10% correction per year. Put very plainly, market pullbacks are normal. Treating them as such can produce much more level-headed decisions, and a lot less anxiety, when they arise.

The central question that emerged last week: Was that pullback the beginning of something much worse? Our take is that this spate of volatility has likely not yet fully run its course. But is this the start of a larger, more sinister decline in the market? No, we don’t think so. The rebound since the latter part of last week was a positive sign, not only for overall market performance, but also because it demonstrated that the backdrop is far more balanced, if not more favourable, than the initial sell-off was otherwise indicating.

The catalyst for each pullback will be different, but for it be more prolonged and meaningful there needs to be something fundamentally wrong with an economy. Like a recession for instance, which leads to a decline in corporate profits and hence lower share prices. Fears of an imminent recession were overblown last week, in our opinion. The economy is slowing – something we firmly anticipated coming into 2024 – but we think the prospects of an outright downturn in GDP this year are still small. Afterall, corporate profits remain on the rise and the US Fed is about to embark on a phase of easing monetary policy. It is worth remembering that in order to stick a soft landing and a normalization of interest rates, we needed to see a cooling of the economy and labour market. Hence it should be no surprise that some of the data shows this. No backdrop is immune from weakness, but we think conditions remain more favourable than hurtful.

Market pullbacks offer the silver lining of attractive entry points and opportunistic rebalancing. Here's what we know: every market pullback in history has been following by a rebound. Every. Single. One. While the coast is not completely clear, we don't anticipate anything different this time around.

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.