Canada Gets the Gold For Rate Cuts. US Fed is Off the Podium.

DHL Wealth Advisory - Aug 02, 2024

Equity markets continued the rotation that began earlier this month, with small-cap stocks and value and cyclical sectors all outperforming mega-cap technology and growth sectors...

Equity markets continued the rotation that began earlier this month, with small-cap stocks and value and cyclical sectors all outperforming mega-cap technology and growth sectors. The Canadian equity market, which has a heavier weighting to sectors like financials and energy, hit an all-time-high of 23,000 on Thursday as it continues to outperform the S&P 500 over the past month. It shouldn’t come as a total surprise to our readers as we have been talking about it for all of 2024, but after more than 1.5 years of large-cap growth sectors and the "Magnificent 7" leading the market, what has caused this somewhat sudden rotation away from the tech darlings? We believe it came down to a few key data points:

After coming out of the gate hot in 2024, inflation has now surprised to the downside: The rotation perhaps truly picked up after the July 11 U.S. consumer price index (CPI) inflation came in cooler than expected for the second month in a row, with headline inflation now at 3.0% year-over-year. Similarly in Canada, CPI inflation for June came in below expectations at 2.7%, at the lows of the year. In our view, the disinflation trend looks poised to continue, though perhaps not in a straight line lower. Markets now more meaningfully believe in Fed interest-rate cuts in the back half of the year, with markets pricing in three rate cuts: at the September, November and December Fed meetings. Given the better inflation trends and some softening in the labour market, we believe two to three rate cuts by year-end is a reasonable scenario and should be supportive of market leadership broadening. In Canada, the BoC has already cut interest rates twice, bringing the benchmark rate to 4.5%, and we wouldn’t be surprised if we finished the year at 4.0% flat.

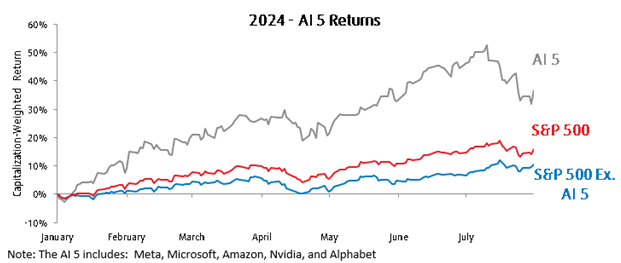

Valuation rotation underway: Finally, one key driver of the rotation may be that valuation differentials between the mega-cap technology space and the rest of the market (e.g., the S&P 500 equal-weight index) had moved too far too fast. For example, the forward price-to-earnings ratio of the technology-heavy Nasdaq index at the beginning of July was about 35 times, versus just 16.5 times for the S&P 500 equal-weight index. Similarly, the Canadian TSX trades at just a 15 times price-to-earnings multiple. After a nice rally in markets, investors may be seeking investments that have more scope for valuation expansion and may also benefit from catalysts like lower interest rates. And this valuation rotation would be supportive of the broader market rotation we've been seeing. Below you’ll notice the near 20% retracement of the AI 5 in July while the S&P500 without those names is essentially flat.

Source: Ernad Sijercic, Portfolio Advisory Team

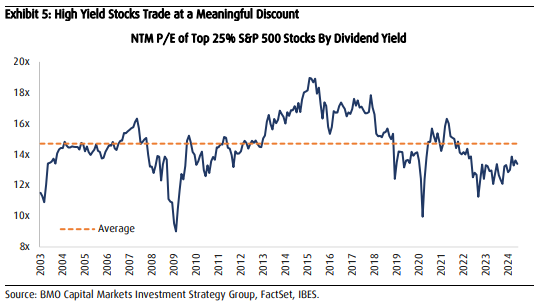

Nowhere is this valuation gap more evident than in the high yield stocks. For instance, despite some increase in valuation for these stocks in recent months the latest level for forward P/E is still at a roughly 10% discount to its historical average (chart below). This contrasts the broader market which has continued to trade at above-average levels. In addition, earnings growth expectations have rebounded in recent months to about-average levels. And when both are put into context it means investors can buy these stocks at a nearly 35% discount to historical averages. Therefore, we believe these trends provide another layer of support for high dividend stocks to outperform in the coming months.

Source: High Dividend Yield Rebound Likely to Persist

Meanwhile, the market ended the week on a low note following a big miss in US employment data. Friday saw the release of U.S. nonfarm payrolls that came in well-below consensus forecasts at 114k compared to estimates of 175k. June’s job gains were revised down to 179k from an originally reported 206k with overall net revisions of -29k in the past two months. Bottom-line, a sizable U.S. labor market slowdown is already well underway at a time when Jerome Powell said he didn’t really want to see any material additional slowing. Not only that, but the unemployment rate unexpectedly increased for the fourth month in a row to 4.3% from 4.1% in June as the number of unemployed increased by 352k last month.

Source: U.S. Employment Slows Sharply and Unemployment Rate Rises in July

Bottom-line: The large miss in July nonfarm payrolls and jump in the unemployment rate underlines what we have been seeing in the overall U.S. economic data for some time now that aggregate demand is softening. This clearly gives the Fed the green light to start cutting rates in September, and the market's attention will now shift focus toward how many and how deep the coming cuts will be.

Source: U.S. Employment Slows Sharply and Unemployment Rate Rises in July

This backdrop of cooling but positive economic growth, easing inflation, and central banks poised to cut rates continues to remain supportive of equity markets broadly, in our view. Overall, despite market and political volatility in recent weeks, we continue to focus on the fundamentals, which we believe remain supportive of the ongoing equity expansion. The economies in the U.S. and Canada, as we learned this month, remain resilient. In the U.S., second-quarter GDP growth exceeded expectations, coming in at 2.8% versus forecasts of 2.0%, largely driven by healthy consumption growth of 2.3%. And in Canada, monthly GDP data in June exceeded forecasts, coming in at 1.1% annually. While we would expect economic growth to cool in both economies in the coming quarters, we believe growth should remain positive, supportive of the "soft-landing" scenario.

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.