Intern's First Update at CrowdStrike And....

DHL Wealth Advisory - Jul 19, 2024

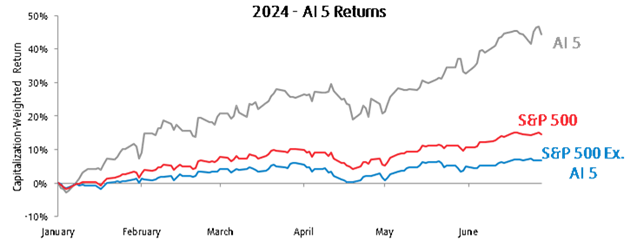

It was an interesting week for North American markets which witnessed record highs, but also a 5-7% correction in a matter of days. It’s been no secret the lions share of market gains have been centered in a handful of mega-cap stocks this year...

It was an interesting week for North American markets which witnessed record highs, but also a 5-7% correction in a matter of days. It’s been no secret the lions share of market gains have been centered in a handful of mega-cap stocks this year, as evidence by our chart below. In fact, through the end of June, the five largest S&P 500 stocks by market cap outpaced the broader market by more than 20% YTD, which ranks the outperformance in the 97th percentile for all historical rolling six-month relative returns since 1991.

Source: Market Outlook Does Not Depend on “MAG-X” Stocks

Source: Ernad Sijercic, Portfolio Advisory Team & S&P Dow Jones Indices

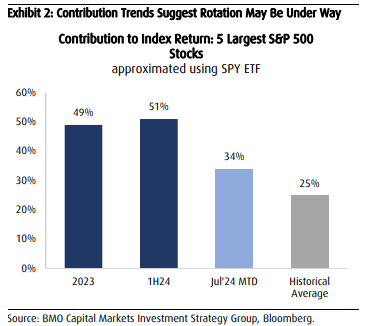

However, trends during July appear to slowly be reversing from a contribution-to-return perspective. For instance, these stocks had been responsible for roughly half of the S&P 500 return for 2023 through 1H24. During July that figure has dropped to about 34% (and that was before Wed-Friday selloff) and despite still being much higher than the historical average (Exhibit 2), has some investors worried that market momentum cannot persist without these stocks continuing to lead the way with historically impressive performance. Although we agree it was inevitable for these outperformance trends to start to subside, we disagree with the notion that the market cannot perform reasonably well without such a significant contribution from these stocks.

Source: Market Outlook Does Not Depend on “MAG-X” Stocks

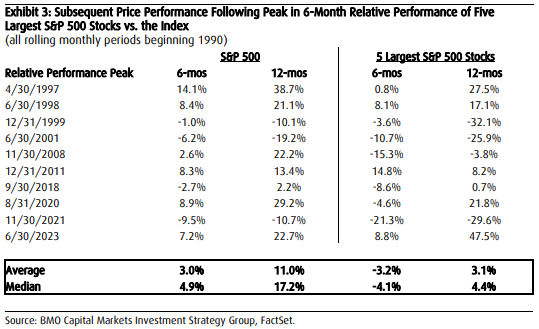

To determine if market troubles occurred following past periods of subsiding mega-cap outperformance, we identified relative performance peaks above +1 standard deviation for rolling six-month periods of the five largest stocks versus the S&P 500 going back to 1990 and examined performance patterns in the subsequent months (Exhibit 3). According to findings, the S&P 500 was able to deliver incremental gains in the six months following such peaks and achieved double-digit returns one year later, on average. And interestingly, aside from the period following the Tech Bubble (a period we continue to believe bears no resemblance to the current environment), stock prices of the five largest stocks remained relatively intact with incrementally positive average gains during the following year. So, despite their admittedly outsized influence on index levels, we believe this stat should help to assuage some of the worries that are out there currently and suggests to us that if relative performance for the five largest market cap stocks does indeed peak, the broader market can hold up just fine in the coming months and beyond.

Source: Market Outlook Does Not Depend on “MAG-X” Stocks

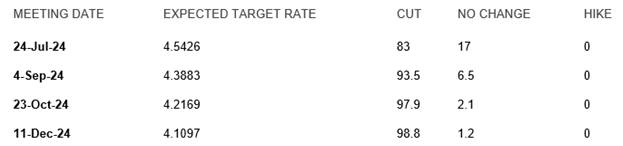

Meanwhile, we had Canadian CPI inflation data on Wednesday that came in well below expectations and kicked wide open the door for another interest rate cut out of the Bank of Canada next week. The market is now pricing in a 92% chance of a BoC quarter-point rate cut at its upcoming policy meeting. Nearly three more quarter-point cuts are now priced into markets by the end of this year, which would bring the bank’s overnight rate to 4%.

Source: ‘A July rate cut should now be a done deal’: How economists and markets are reacting to today’s inflation data - Globe & Mail

Coming into this month, probabilities for an interest rate cut on July 24 were essentially down to a coin flip. But several economic reports since then - most notably a weak June Canadian jobs report - had markets increasingly pricing in a July 24 quarter-point rate cut by the BoC. Several economic reports and dovish Federal Reserve market commentary out of the U.S. in recent days also now have markets nearly fully pricing in a Fed rate cut in September - which has raised confidence levels further that the BoC will soon cut rates a second time.

Source: ‘A July rate cut should now be a done deal’: How economists and markets are reacting to today’s inflation data - Globe & Mail

Canada’s annual inflation rate cooled a tick more than expected to 2.7% in June, largely due to softer growth in gas prices, while core inflation measures were marginally down. Analysts had forecast the inflation rate would tick down to 2.8% from 2.9% in May. Here’s the outlook for the balance of meetings in 2024.

Source:‘A July rate cut should now be a done deal’: How economists and markets are reacting to today’s inflation data - Globe & Mail

Source: ‘A July rate cut should now be a done deal’: How economists and markets are reacting to today’s inflation data - Globe & Mail

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.