*Breaking News* McDavid Is Really Good.

DHL Wealth Advisory - Jun 21, 2024

Another mixed week for North American indexes as our neighbours to the South enjoyed new highs in the S&P500 and NASDAQ, while other major indexes were lower...

Another mixed week for North American indexes as our neighbours to the South enjoyed new highs in the S&P500 and NASDAQ, while other major indexes were lower. It’s been no secret in June that technology has been the only sector leading broader markets higher. The breadth of the ~9-month- rally has stalled and major indexes are only seeing new highs because of a handful of mega-cap stocks (NVDA, AAPL, MSFT, etc). Somewhat similar to the final few months of 2023 where if you didn’t own one of the “Magnificent 7” stocks, you were almost assured to be in the red for the year. More on all this later.

There’s isn’t a particular reason why market breadth has stalled. Economic data continues to come in largely positive, albeit slowing from a torrid pace. Positive, but slowing, data is what strategists and policymakers want to see to keep the soft-landing narrative intact. In fact, the US Fed projects that U.S. GDP growth will remain at or above 2.0% through 2026, while the unemployment rate will remain steady between 4.0% and 4.2% over the next three years. Despite months of restrictive interest rates, the Fed does not see any meaningful deterioration in the economy or outsized softness in the labour market. In addition, the Fed still believes inflation will fall to 2.0% by 2026, even as economic growth remains steady.

In our view, this soft landing continues to remain a base-case scenario for the U.S. economy. Productivity in the U.S. has more recently trended higher (most likely driven by labour shortages) and may continue to do so, as artificial intelligence (AI) efficiencies are realized across sectors. While consumption and the labour market may cool, this slowdown may indicate normalization from elevated economic growth rather than a meaningful deterioration. If inflation does moderate and the Fed embarks on a rate-cutting cycle, this could also spark better economic momentum in the years ahead.

The risks to this soft-landing view are, of course, that either inflation does not moderate as expected – and perhaps even reaccelerates – or that the economy or labour market deteriorates more than anticipated. In our view, neither of these scenarios are currently supported by the data or leading indicators of the economy. We continue to see healthy consumption patterns, relative strength in the labour market, and most recently, inflation data that have eased more than expectations.

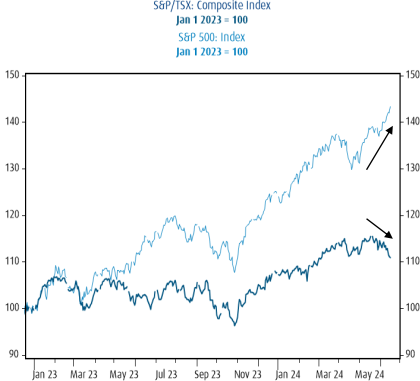

Meanwhile, Canadian stocks, which are always a valuation darling but rarely an outperformer, have returned to their lagging ways. Since the end of April, the TSX has struggled to stay positive, while the S&P 500 has pushed nearly 10% higher to record levels. As is often the case, this is mostly the result of composition. Banks and energy have struggled heading into the summer, which is always a tough backdrop for the TSX. In the meantime, technology has lurched more than 20% higher in the S&P 500 (with a more than 30% weight).Even within the S&P 500, outsized gains in a few technology names are playing a big role. While the standard index is up almost 10%, the equal-weight S&P 500 is up just 2% since the start of May.

Source: Cdn Equities Back to Lagging

Source: Cdn Equities Back to Lagging

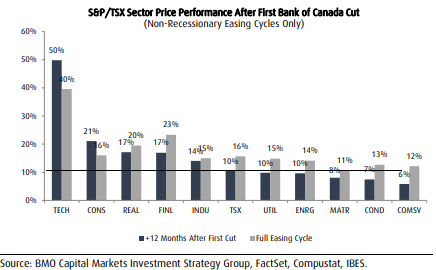

Last week we highlighted that “proactive” easing cycles have historically been a strong positive catalyst for TSX performance, with the S&P/TSX posting solid double-digit gains on average 12 months after the first Bank of Canada rate cut. Under the surface, analysis shows an increasingly broad fundamental outperformance transpires following such “proactive cuts.” This is especially evident with respect to quality and capital usage factors, while more growth-heavy factors typically underperform.

On a sector basis, cyclical sectors like Technology, and interest rate-sensitive areas like Financials and Real Estate tend to outperform during this environment. While all cycles are certainly not the same, we believe the strong value and quality profiles of Financials, Real Estate and Communication Services suggest these areas are well-positioned to benefit from easing interest rate pressures.

In addition, we continue to believe underappreciated Canadian small cap stocks are ripe for a “catch-up” trade and have historically outperformed large cap TSX during these types of easing cycles. To reiterate, we believe the Bank of Canada proactively entering the easing cycle early could be a clear catalyst for our long-awaited Canadian “catch-up” trade which we believe will benefit many of the underperforming areas of the equity market.

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.