Super Cool Supercore

DHL Wealth Advisory - Jun 14, 2024

US markets cooled off Friday as investors looked to lock in gains after the benchmark S&P 500 and Nasdaq posted four straight days of record closes. Tech giants have been at the forefront of these gains and despite the consecutive new highs...

US markets cooled off Friday as investors looked to lock in gains after the benchmark S&P 500 and Nasdaq posted four straight days of record closes. Tech giants have been at the forefront of these gains and despite the consecutive new highs, the NYSE breadth has actually been negative (more decliners than advancers) more frequently for the last two weeks. At the same time less than half of the stocks in the index are trading above their 50-day moving averages leaving us with the big question of whether or not the mega-cap growth stocks will be able to continue offsetting what is happening to most of the other stocks in the index.

Wednesday was arguably the most important day of the month in terms of market moving economic data. The May U.S. CPI report and FOMC announcement were crammed into an exhilarating six-hour window with CPI delivering a welcome jolt of surprisingly good news, a refreshing change from the string of non-stop meaty increases seen earlier this year. However, some of that good news was diluted by a cautious Fed, which downshifted its consensus view on this year’s expected rate cuts from 75 bps to a parsimonious 25 bps, albeit followed by 100 bps next year. Still, this didn’t overly discourage markets, since the opinion among Fed members is diverse (with nearly half still looking at two cuts this year), and the good inflation news kept coming with declines in May producer and import prices.

Source: BMO Economics Talking Points: The French Disconnection

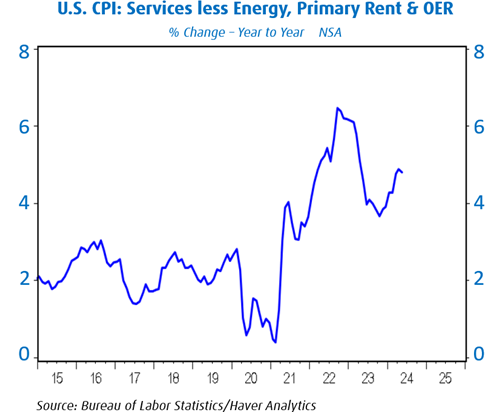

What really set this report apart is that core-core services prices (excluding energy and rent) actually fell for the first time since September 2021, and the dip was somewhat broad based. Mind you, this followed a blistering 7.4% annualized gain in the first four months of the year, which is keeping the yearly rate elevated at 4.8%. Still, it could be an early sign that looser labour markets are bearing some disinflation fruit.

Source: BMO Economics AM Charts: June 13, 2024

Canada was largely a spectator to this week’s many important developments. But the heavy-duty bond market rally seeped into GoCs, slicing yields nearly as much as for Treasuries. The reality is that even with all of the brave talk from the Bank of Canada about carving an independent policy path, it would make additional rate cuts much easier if the Fed is also cutting. The important five-year yield fell 20 bps on the week, following an 18 bp drop last week, taking it to 3.3%. That’s more than 100 bps below last Fall’s highs, and, through the longer-term mortgage rate channel, could provide some important additional support for the housing market.

Source: BMO Economics Talking Points: The French Disconnection

Of course, almost no one is hoping for a quick rebound in Canada’s housing market. The one key data release this week was the Q1 national balance sheet, and it revealed a further welcome pullback in household debt ratios. After peaking at nearly 185% of disposable income in mid-2022, household credit market debt has eased almost 10 ppts to 175%, even below pre-pandemic levels. While still on the high side of international norms, the debt burden is gradually moderating, and even debt-service costs dipped slightly in the quarter (albeit still high at nearly 15%, versus less than 10% stateside). As this week’s Focus Feature details, getting housing affordability back into reasonable shape could take a multi-year workout, and that goes for household debt as well. Lower borrowing costs could play a role, provided they don’t spark another flare-up in home prices. That’s a very big “if”, given Canada’s recent history.

Source: BMO Economics Talking Points: The French Disconnection

Next week’s calendar will bring the latest on Canadian housing in May, prior to this month’s rate relief, with both starts and sales due Monday. There could be a pop in starts, presaged by a spike in permits the prior month, but sales and prices have had a very quiet spring (not a bad thing). We’ll also get a read on the health of consumers, with retail sales due from both the U.S. (on Tuesday for May) and Canada (on Friday for April). We suspect both reports will post small gains, suggesting that spending is cool, but hardly faltering. As a result, inflation will continue to be the primary policy guidepost, and this week’s mild U.S. results were a massive step in the right direction.

Source: BMO Economics Talking Points: The French Disconnection

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.