The Last Time Dow Jones Crossed this Threshold, J.T. Miller had a Full Set of Teeth.

DHL Wealth Advisory - May 17, 2024

Yet another week of record highs for major US indexes in a continuation of an advance that’s been fueled by speculation the Federal Reserve will be able to cut interest rates this year...

Yet another week of record highs for major US indexes in a continuation of an advance that’s been fueled by speculation the Federal Reserve will be able to cut interest rates this year. A slew of data from industrial production to jobless claims and housing only added to the long list of figures pointing to stability or only a gradual cooling of an otherwise resilient economy that’s powering Corporate America.

In a trivial but interesting event, the price weighted Dow Jones Industrial Average jumped above 40,000 for the first time on Thursday. The index had neared the 40,000 mark earlier this year, before a slight April pullback.

Given this historic mark, we thought it would be interesting to give a little history lesson on the index. Founded in 1896 with 12 industrial stocks, the original constituents were American Cotton Oil, American Sugar, American Tobacco, Chicago Gas, Distilling and Cattle Feeding, General Electric GE , Laclede Gas, National Lead, North American, Tennessee Coal Iron and RR, U.S. Leather, and United States Rubber. Of course, GE is the only stock of the original 12 left on the index, despite being dropped twice. It's first drop occurred just two years after its original induction in favor of U.S. Rubber, but it rejoined in 1899 for another two years before dropping off again in 1901. GE's second replacement was U.S. Steel, but after the steel company bought fellow component Tennessee Coal Iron and RR, GE was able to rejoin for good in 1907. Meanwhile on March 15, 1933, the DOW had the largest one-day percentage gain in the index during the 1930s bear market, totaling 15.34%. The Dow gained a mere 8.26 points and closed at 62.10. Today, that 8.26 points would represent 0.02% increase, or a small rounding error. It’s taken ~4 years for the DOW to add 10,000 points. It crossed 30,000 for the first time on November 24, 2020.

Enough of our walk down memory lane and back to today’s ongoing bull market. Recent economic releases in the U.S., like the advanced estimate of first-quarter GDP, the Purchasing Managers' Index, the April job gains, and the big one this week was the release of US Consumer Price Inflation (CPI) all show that at this juncture in the market “OK” or “good” may be better than great as it relates to economic data and market outlook. The reason being is the “Goldilocks” narrative requires a cooling, but still growing economy and labour market. Too much stokes inflation and an aggressive fed. Too little and we get a recessionary environment.

Well, on Wednesday data that showed US inflation cooled for the month of April. U.S. CPI inflation moderated to 0.3% in April from 0.4% in March and February. This was somewhat below consensus forecasts and, on-the-margin, there was a softer pattern to the individual price categories last month that is somewhat Fed friendly. If sustained, it could keep Fed rate-cut expectations for September and December alive and well. Clearly, restrictive monetary policy has more work to do, and the Fed will remain patient and watchful.

Source: U.S. CPI Inflation Shows Some Encourgaing Cooling in April

No doubt a lot of progress has been made since inflation peaked at 9.1% in the U.S. and 8.1% in Canada in June 2022, but we are not there yet. Markets are akin to children in the back of a car, less concerned with how far the journey has progressed, but rather eagerly awaiting the arrival at the destination. After three back-to-back upside U.S. inflation surprises to start the year, confidence that inflation is moving toward the 2% target is shaken, and the journey has got bumpier.

Meanwhile, BMO’s Chief Investment Office Brian Belski has increased his target on the S&P/TSX price target to 24,500 from 23,500. While this is a minor 4% increase to the price target, it reflects multiple signs that both sentiment and revision trends have bottomed and are beginning to improve, which we believe will be a key tailwind for valuation expansion into year-end. As such, his 2024 implied P/E ratio increases to 16.3x from 15.7x, this is still well below the long-term average multiple of 17x. Overall, unlike in 2023 when the big three sectors underperformed (it is difficult for the TSX to do well with that backdrop), two of the three largest sectors in the TSX are sharply outperforming this year. Furthermore, performance is clearly broadening with an increasing focus on fundamentals. In his opinion, this is another strong sign that financials and the other non-big three sectors are primed for a sharp rebound and catch-up trade in the back half of the year.

Source: Canadian Strategy Snapshot: S&P/TSX Target Update

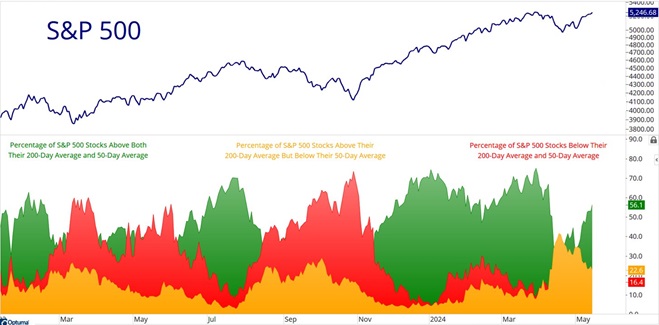

Lastly, from a purely technical perspective, the weight of the evidence is leaning bullish in a strong way. We found the below chart quite telling: Breadth is expanding. Sentiment is not a headwind, there is no stress from credit spreads, and trends and momentum are strong. The market is a lot less messy, and the vast majority of stocks are in uptrends. In fact, roughly 80% of S&P 500 constituents are above either their 50-day or 200-day moving average (or both). The argument that this is purely just a “tech” rally is no longer the case.

Sources: All Star Charts & Grant Hawkings

With uncertainty around the inflation and interest-rate outlooks high, appropriate diversification across asset classes, regions, investment styles and sectors is important. However, the combination of rising corporate profits, the continued economic expansion, and the potential for more downside than upside in yields provides a positive backdrop for markets as the bull market continues.

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.