We Reiterate our view: Only Bear Market here is Elias Petterson's production... STILL.

DHL Wealth Advisory - May 10, 2024

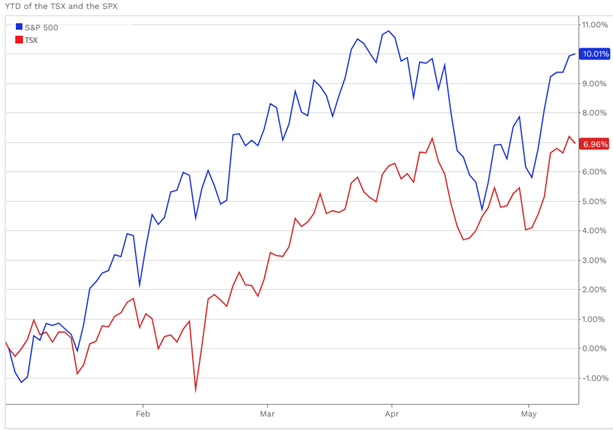

Following some April showers markets have welcomed May with the longest winning streak of the year in the Dow Industrials average and major benchmarks once again hovering near record territory...

Following some April showers markets have welcomed May with the longest winning streak of the year in the Dow Industrials average and major benchmarks once again hovering near record territory. We won’t yet sound the all-clear horn for market volatility as we expect continued swings around the timing and pace of rate cuts, but we do highlight the broadening of market strength outside of mega-cap tech as incredibly healthy for the longevity of a bull market.

Leading the charge higher has been strength in financials, utilities, and materials. In fact, there has been both a fundamentally driven broadening out of performance and definitive shift toward more cyclical factors this year. And it’s worth remembering that Canada’s S&P TSX is heavily titled to these areas of the market vs our tech heavy neighbours to the South.

From our perspective, this fundamentally driven broadening out of performance will be a key tailwind for Canadian equities through the second half of the year. Additionally, the Canadian market has seen a clear cyclical shift from value to growth factors. In 2023, the more defensive valuation and capital usage factors were the only factors to outperform. This year, more cyclical factors such as growth (both trailing and forward growth) and high-risk factors have been the top-performing categories.

Source: Canadian Strategy Snapshot: Factor Performance Observations of the TSX

Interestingly, this is the mirror image of US factor performance, where more cyclical factors outperformed in 2023, and now valuation and capital usage factors are top [1] performing categories year-to-date. From our perspective, this is yet another sign that Canadian equities are poised for a strong catch-up trade in the coming quarters and something we have been talking about all year. Overall, we expect this dynamic to proceed throughout 2024 as the market continues along its normalization process.

Source:Canadian Strategy Snapshot: Factor Performance Observations of the TSX

And it wouldn’t be a 2024 Market Watch Weekly without some commentary around interest rates… (We’re sorry). We still believe the next Fed rate move will be a cut, we suspect it will take at least three or more consecutive months of improving inflation readings before the Fed will take that step, meaning a fall or even late 2024 cut is a reasonable, but not inevitable, timeline. Remember, one or two months of data doesn’t make a “trend”, and a “trend” is what the Fed wants to see. Markets have been obsessed with the precise timing, but we think the more important factor is direction.

And speaking of direction, we wrote to this a few weeks sago. Historical returns in periods of steady rates offer some encouraging results. The Fed held the Fed Funds rate steady from September 1992 to January 1994, with the stock market returning 16% during that time. After hiking rates aggressively through 1994, the Fed kept its policy rate on hold from February 1996 to February 1997, with stocks gaining 26% over that stretch. Following a brief hike, the Fed paused again from March 1997 to August 1998, with stocks adding 45%. The Fed remained on hold again from June 2006 to August 2007, with the S&P returning 16% in that time. While the markets have experienced some recent indigestion with the prospect of delayed rate cuts, these instances suggest an extended pause by the Fed doesn’t have to be detrimental to market performance.

Perhaps the most consistent element of the investment backdrop for the last few years has been the significant strength of the labour market and the resulting boost that has provided to the consumer and overall GDP growth. We started 2024 with US unemployment only slightly above historic lows and monthly job gains that averaged 250,000 through 2023, key factors that enabled the economy to avoid a recession, which we thought was a reasonable outcome after the Fed’s historic policy tightening (rate hike) campaign through 2022.

As far as favourable conditions go, a healthy labour market is near the top of the list. Our view has been that the labor market can remain in sufficiently healthy shape to support an ongoing expansion. Our prior expectation for an economic slowdown was largely based on other segments of the economy (manufacturing, capital investment, housing investment) that were contracting following 2022’s rate hikes. There is evidence that these areas are now rebounding, taking some of the pressure off the consumer to hold up GDP growth.

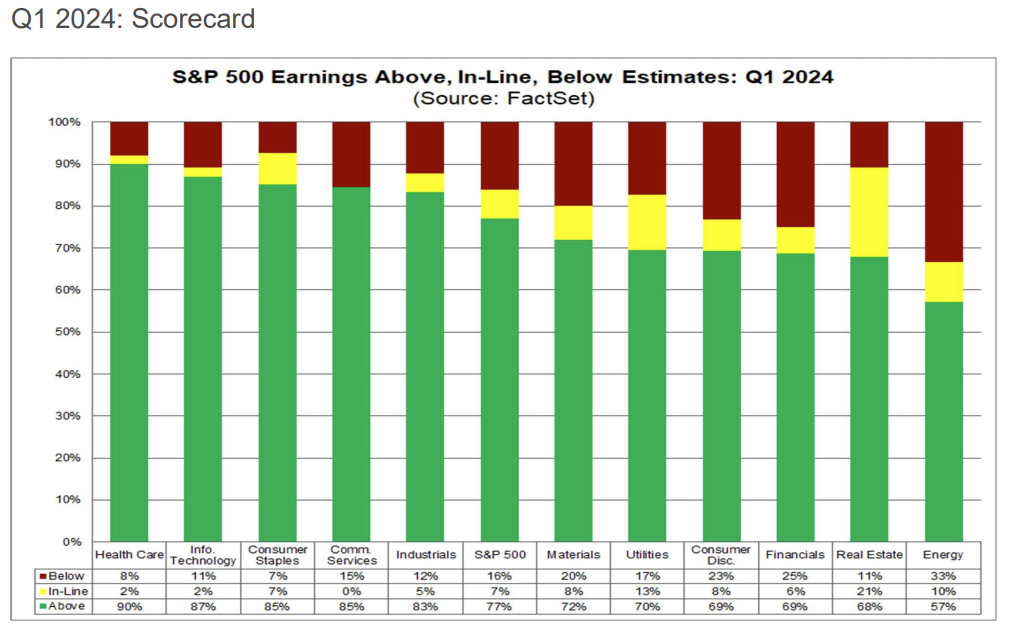

We think the market can be tolerant of high rates for longer, as long as the economic backdrop remains sufficiently solid to support current expectations for earnings growth. With valuations having already risen in anticipation of higher earnings, we think this year’s market gains will be largely driven by the pace of earnings growth. To that point, over 80% of S&P 500 companies have reported Q1 results, and earnings and revenue beats are tracking in-line with 5-year averages. Analysts are now calling for 2024 earnings to rise 11% year-over-year.

Source:Earnings Insight Factset

This suggests to us solid upside for equities this year, though unlikely to match last year’s sharp gain. In any event, our overweight recommendation to equites reflects our view that stocks can outperform bonds and cash, even though we think lower rates over time will also support more compelling bond returns.

This won’t, in our view, come without additional bouts of volatility ahead, so portfolio diversification and an opportunistic view of temporary pullbacks looks to us to be an appropriate stance. We’re encouraged to see both earnings and performance leadership broadening beyond mega-cap tech, as we think this builds a healthy base for the bull market to extend.

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.