Feds Version of Capital Punishment.

DHL Wealth Advisory - Apr 19, 2024

North American markets remained volatile this week as investors continue to digest economic data for clues as to when we’ll see the first interest rate cut out of the US Federal Reserve...

North American markets remained volatile this week as investors continue to digest economic data for clues as to when we’ll see the first interest rate cut out of the US Federal Reserve. Interest rates worries have re-emerged in recent weeks following several hotter-than-expected US inflation prints and a series of upside surprises from key economic reports.

This combination has seemingly shifted investor Fed rate cut expectations significantly, with the market now pricing in only two 25 bps cuts for 2024 vs. the seven expected at the start of the year. As a result, the US 10-year Treasury yield has jumped more than 50 bps since early March, the largest uptick since the ~90 bps move higher during September-October 2023. Once again, this move has many investors contemplating how much longer the 2024 YTD market rally (10% in the first quarter — the strongest start to a year since 2019) can last should interest rates continue to rise or stay elevated, even after accounting for the continued strength in the economy.

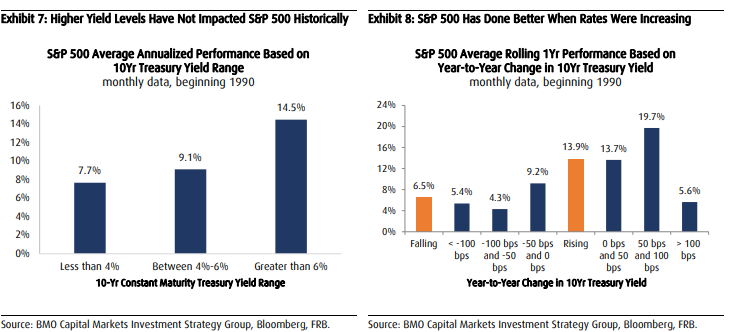

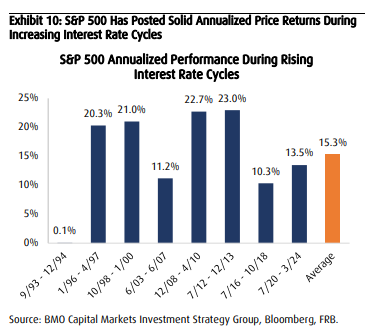

However, our work shows that investors should not fear higher rates, despite current conventional thinking to the contrary. In fact, we found that some of the strongest periods of S&P 500 performance have coincided with rising or higher levels of interest rates over the past few decades. For instance, we analyzed all rolling one -year periods, as well as cycles where interest rates increased for at least one year since 1990, and calculated S&P 500 performance under these various interest rate scenarios. We summarized our findings in the exhibits below. The highlights of our analysis are as follows:

- Low levels of interest rates are not necessarily the best environment for US stock market performance. For instance, the S&P 500 delivers stronger average price returns and has a higher probability of gains at higher levels of interest rates compared to lower levels of interest rates. This makes sense to us since lower rates can be reflective of sluggish economic growth and vice versa.

- Rising interest rates have seemingly benefited US stock market performance. In fact, the S&P 500 has posted an average price return of 13. 9% during periods of increasing rates compared to just a 6.5% average gain during periods of falling rates. In fact, moderate yield level increases (i.e. , between 0 -100 bps) have exhibited the strongest returns of all periods. In addition, during the eight interest rate cycles we identified since 1990 in which yields increased for prolonged periods, the S&P 500 logged an average annualized price gain of ~15%. From our perspective, rising interest rates can mean that the bond market is correctly anticipating future economic growth and staying ahead of inflation – things that typically benefit stock prices

To be sure, however, the era of “easy money” investing is likely behind us, and the transition to a more “normal” rate structure is likely to be challenging, causing many fits and starts for market performance in the coming months as it adjusts to this reality, in our view. Thus, we believe it is important for investors to fall back on their disciplines and maintain an active approach when searching for opportunities.

Otherwise all eyes in Canada were on this week’s 2024 Federal Budget. As expected, Budget 2024 highlighted the government’s objective to increase the housing supply (3.87 million new homes by 2031) and to support renters and lower the costs of home ownership, through key measures such as an enhanced Canadian Mortgage Charter, a new Canadian Renters’ Bill of Rights and increased withdrawal limits from the Home Buyer’s Plan. In addition, affordability measures and the stated goals of growing the economy in a way that’s shared by all, enhanced productivity, innovation and empowering entrepreneurship, were also highlighted. However, Budget 2024 seeks higher tax revenue from the wealthiest Canadians – $21.9B over 5 years – and aims to improve the fairness of the tax system by achieving more equitable tax rates across revenue sources and income levels. Budget 2024 anticipates a deficit of $40B for 2023-24 – slightly below the stated fiscal objective outlined in the 2023 Fall Economic statement – which is scheduled to improve to a $20B deficit in 2028-29.

From a personal and small business tax perspective, the most significant measure is the introduction of a higher capital gains inclusion rate (from one-half to two-thirds) for all capital gains realized by corporations and trusts, and for individuals on annual capital gains exceeding $250,000. Conversely, an increase in the Lifetime Capital Gains Exemption (LCGE) and a lower capital gain inclusion rate to incent business owners – through the new Canadian Entrepreneurs’ Incentive (CEI) – were also introduced.

To us this the Budget is generally neutral on balance. The TSX impact remains uncertain but perhaps near-term relief for some sectors (grocers, oil & gas, telcos) given lack of more targeted tax hikes. However, the new taxes will likely to weigh on business investment, given that Canada already has highest corporate tax rates among AAA-rated G7 economies. In addition, growth ahead will make it tougher to meet fiscal anchors without additional tax increases.

To read a full BMO Review of the Budget, please see the below link.

2024 Federal Budget Review - BMO Private Wealth

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.