Three Strikes; Junes Out!

DHL Wealth Advisory - Apr 12, 2024

Global markets were lower this week as investors digested a hotter-than-expected US inflation report and a potential escalation of events in the Middle East. For the third consecutive month, the core US Consumer Price Index (CPI) increased 0.4%...

Global markets were lower this week as investors digested a hotter-than-expected US inflation report and a potential escalation of events in the Middle East. For the third consecutive month, the core US Consumer Price Index (CPI) increased 0.4%. What was initially dismissed as start-of-the-year seasonal pressure, or some other anomaly, is fast morphing into a trend.

We have seen a strong uptrend in headline inflation so far this year and, really, since a subdued October print. Not the consumer inflation trend that US Fed Chair Jay Powell and the rest of the FOMC want to see to start cutting interest rates. It’s worth noting that half of the increase in inflation last month came from just two components: gasoline (+1.7%) and shelter (+0.4%).

BMO Economics EconoFACTS: Oh Oh Another “Hot” U.S. CPI Report

Core CPI inflation, excluding food and energy, also increased more than forecast, rising 0.4% last month and up 3.8% from a year ago, unchanged from February’s elevated pace. The consensus had been expecting a slowdown to 3.7%. Core inflation has been running at an overheated 0.4% m/m pace for three consecutive months now, double the rate seen last October when the Fed began seriously laying the groundwork to begin cutting interest rates this year.

BMO Economics EconoFACTS: Oh Oh Another “Hot” U.S. CPI Report

As such, the data release calendar now points to July as the earliest policy pivot, no longer June. The market is currently pricing 11% odds of a June move and 40% for July, with a complete rate cut only priced in by November.

Meanwhile the divergence in the inflation battle between Canada and the United States seems to be widening. On Wednesday the Bank of Canada held rates steady at 5%, as expected, for the sixth consecutive meeting. However, the tone of the policy statement was mildly more dovish, acknowledging the slowing in underlying inflation and loosening labour market.

The $32,000 question is how far can the Bank of Canada diverge from the Federal Reserve? That question was swirling this week, with some serious separation in policies moving from the merely academic to a real-world possibility. Wednesday’s confluence of a third clunky U.S. CPI, and mildly dovish remarks from the BoC soon afterwards, had the markets chattering about a deepening policy divide. In a week that saw U.S. Treasury yields post another big push higher, Canadian short-term yields trailed well behind.

BMO Economics Talking Points: You Take the High Road, and We’ll Take the Low

Bank of Canada Governor Macklem was asked very directly about this issue of potentially divergent North American monetary policies, and his response was also quite clear: Canada will do its own thing. However, by exactly how much can the BoC diverge without causing serious blowback in the currency market? Keeping in mind that the starting point is that Canadian rates are lower (5.0% overnight rate, versus 5.25%-to-5.50% for the Fed funds target), strategists suspect that the Bank can cut once independently, and then trim one more time—if a Fed cut appears imminent.

BMO Economics Talking Points: You Take the High Road, and We’ll Take the Low

For the BoC, a June move is “within the realm of possibilities” says Governor Macklem, and we are sticking with that projection for now. No doubt, it will be a close call, and markets see the June meeting as a coin toss. Next Tuesday’s Canadian CPI will have a big say (expectations are for headline inflation to tick up to 2.9%, and the cores to hold steady just above 3%), as could the federal budget on the same day.

BMO Economics Talking Points: You Take the High Road, and We’ll Take the Low

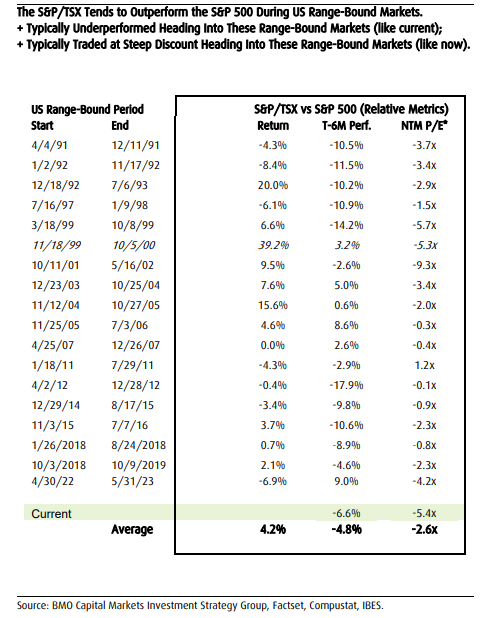

As we have laid out in recent comments, we have been in a period of considerable strength for US markets – essentially an un-interupted rally since October. It is only natural for the pace of gains to slow and we are overdue for a much deserved breather in equity markets. However, despite our expecation for a period of consolidation in the US market, we continue to see value in the Canadian market. In fact, BMO Chief Investment Officer Brian Belski finds that since 1990, the S&P/TSX outperformed the S&P 500 by over 4% on average during US range-bound markets and outperformed in 61% of the periods. Even if we exclude the largest outlier period (11/1999 to 10/2000), the TSX still outperforms the US by over 2% on average. In parallel to the current market environment, the TSX typically underperformed heading into the range-bound markets and typically traded at a steep discount to the S&P 500 heading into these periods. As such, he believes the TSX is well-positioned to outperform even if US equity markets see more tempered and volatile returns over the coming months and quarters.

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.