No Eggs Laid This Quarter...

DHL Wealth Advisory - Mar 28, 2024

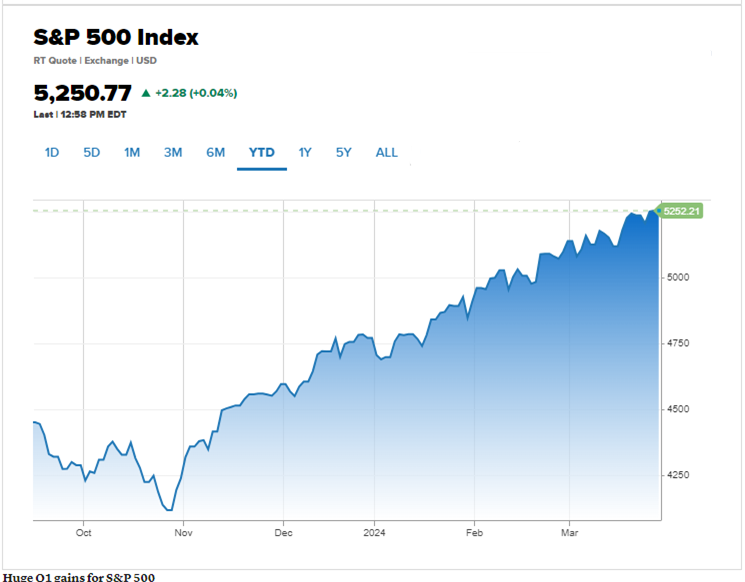

The curtain closed on a historic first quarter for North American benchmarks. The S&P 500 was flat Thursday as it wrapped up its best first-quarter performance in five years. For the quarter, the S&P 500 was up 10%...

The curtain closed on a historic first quarter for North American benchmarks. The S&P 500 was flat Thursday as it wrapped up its best first-quarter performance in five years. For the quarter, the S&P 500 was up 10%. Its best first-quarter gain since 2019, when it rallied 13.1%. The 30-stock Dow, up 5.5% during the period, had its strongest first-quarter performance since 2021 when it advanced 7.4%. As a welcomed change of pace, the Nasdaq wasn’t the clear winner this quarter, up 9%. Canada’s TSX was a minor laggard, up ~6%.

As we reiterated last week, we believe Canada remains the predominant contrarian call in terms of developed equity markets in 2024. Granted, the TSX composite has recently eclipsed all-time price highs, but overall index performance pales in comparison to its neighbour to the south. From our lens, Canadian small cap stocks are an even deeper contrarian call within an already contrarian context with respect to overall Canadian equities – an asset class that we believe is primed for a catch-up trade that could even eclipse the large cap stocks.

Source: Canadian Strategy Snapshot: Canadian Small Cap Primed for Catch-Up Trade

In fact, while the S&P/TSX small cap index has managed to keep pace with its large cap peers so far this year, the index remains well off its 2022 historical high. Furthermore, our work suggests the fundamental underpinnings are improving faster than its large cap peers, with earnings growth set to rebound to double digits over the next twelve months, well ahead of the single-digit growth expectations for the overall S&P/TSX composite. As such, we believe investors should be looking within the Canadian small cap universe for both value and growth opportunities with a tilt toward traditional cyclical areas of the market. To this point, within our discretionary mandate we started a new position in a mid-cap Canadian industrial company and added to an existing position of a Canadian airliner.

Source: Canadian Strategy Snapshot: Canadian Small Cap Primed for Catch-Up Trade

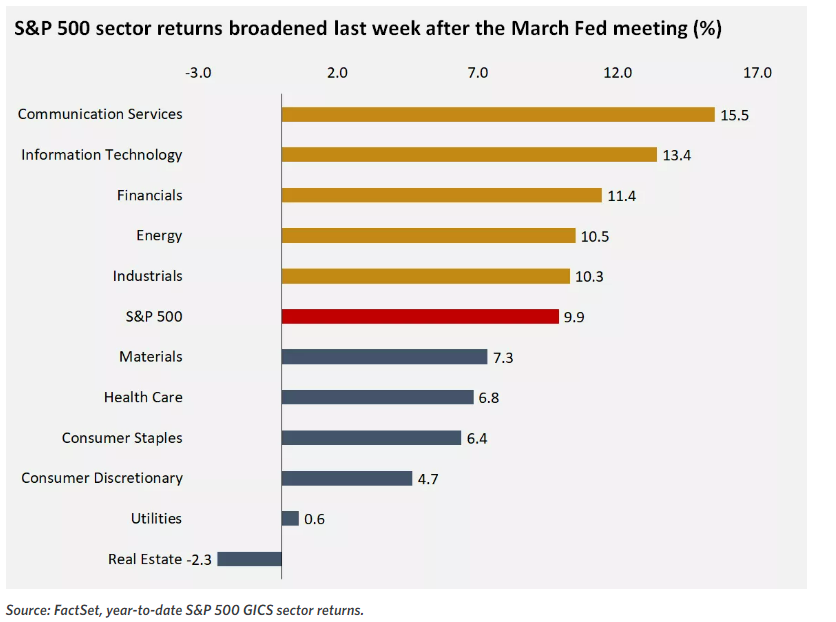

Something we have been discussing in ongoing edition is our expectation for market breadth to expand. It’s no secret that the bulk of the returns witnessed in the last 5-6 months has been centered around a handful of mega-cap technology stocks. Well, in recent weeks we have begun to witness a broadening of the rally out of technology and into new sector leadership. Notably, the small-cap and mid-cap indexes have outperformed the broader S&P 500 after the Fed meeting last Wednesday. These included cyclical sectors like financials, energy, and industrials. And we expect these trends to continue for the balance of 2024.

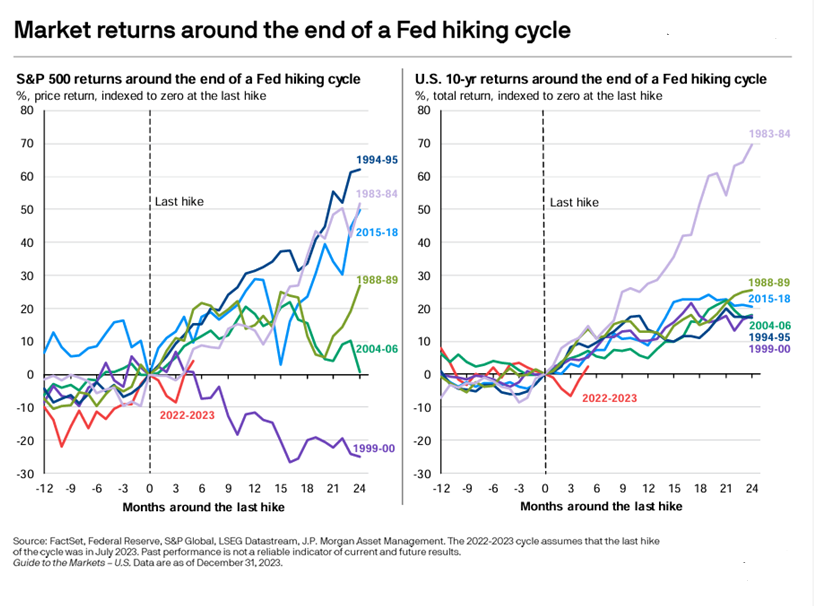

Ending this week with an interesting chart out of JP Morgan, their team did an analysis of market returns around the end of a Fed hiking cycle. While we haven’t had complete assurance of this just yet, recent Fed Commentary would largely suggest the next move out of the US Fed is a move lower, not higher, and the last rate hike witnessed in July 2023 might very well be the last in this cycle. The analysis shows that after a rocky few months last summer, the market is now in the early innings of a new bull cycle.

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.