Took Almost Two Years, But...

DHL Wealth Advisory - Mar 22, 2024

We hinted at it in our last edition two weeks ago and this week it became a reality. After the S&P 500 notched its 20th new high of 2024 on Thursday, Canada’s overlooked TSX jumped on the global bandwagon this week and traded in record territory...

We hinted at it in our last edition two weeks ago and this week it became a reality. After the S&P 500 notched its 20th new high of 2024 on Thursday, Canada’s overlooked TSX jumped on the global bandwagon this week and traded in record territory. The TSX hit fresh all-time highs after topping the 22,000 level for the first time since April 2022 late Wednesday afternoon.

Our view on Canadian equities heading into 2024 was that the investing climate was way too negative. Thus, we invoked our Winnie-The-Pooh “Eeyore” mantra to describe the psychological wherewithal (or lack thereof) of Canadian investors. Namely, we believed sentiment was resoundingly negative and becoming worse. As we approach the end of the first calendar quarter of 2024, we maintain the view that analysts and investors remain overly cautious – fundamental metrics such as earnings, valuation, and operating performance in several areas are showing definitive signs of troughing.

Source: Canadian Strategy Snapshot: No Signs of 'Tigger' Yet

However, “troughing or bottoming” is not quite the fuel to spawn the return to the “Tigger” revival that we still expect to transpire. For instance, fourth-quarter earnings season was uneventful and provided little forward guidance. Furthermore, analysts continue to revise estimates lower and the growth outlook for the TSX is now in the mid-single-digit range out to 2025. In our view, we believe these more defensive outlooks are setting the stage for very beatable quarters ahead. As such, we continue to believe Canada remains the contrarian call in terms of developed markets in 2024, even as the TSX hits a new all-time high. As the reality of a more resilient economy (for both Canada and the US), coupled with increasingly stable interest rates become clear in the second half of 2024, we believe earnings growth will begin to rebound faster than currently expected. Furthermore, with US price action likely to be more volatile over the forthcoming months, this could potentially prompt investors to shift their focus back towards Canada given its value proposition, growth-at-a-reasonable-price characteristics, and strong income potential.

Source: Canadian Strategy Snapshot: No Signs of 'Tigger' Yet

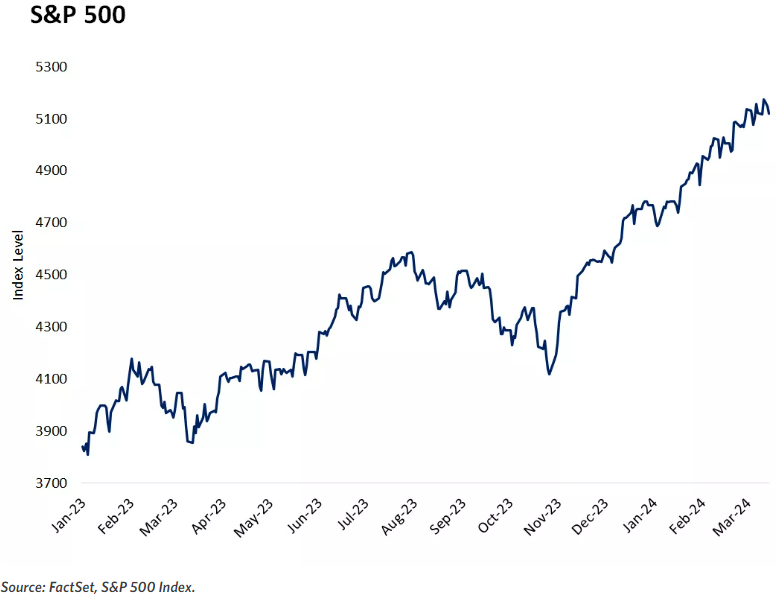

Moving markets higher this week was the US Federal Reserve after it signaled that it’s on track to cut interest rates for the first time since the onset of the pandemic. In a historic move, the S&P 500 topped 5,200 on speculation that the end of the most-aggressive Fed hiking cycle in a generation will keep fueling Corporate America’s profits. Gains in equities were almost broad-based, with areas that have been lagging this year — like small caps — rallying.

Fed officials maintained their outlook for three cuts this year and moved toward slowing the pace of reducing their bond holdings, suggesting they aren’t alarmed by a recent uptick in inflation. While Fed Chair Jerome Powell continued to highlight officials would like to see more evidence that prices are coming down, he also said it will be appropriate to start easing “at some point this year.”

Meanwhile closer to home we learned that Canada’s inflation rate unexpectedly fell last month and underlying price pressures are quickly fading, opening the door for the Bank of Canada to discuss lowering interest rates. The Consumer Price Index rose 2.8% in February on an annual basis, down from 2.9% in January. Analysts were expecting an upturn to 3.1%. This was the second consecutive month that CPI growth has undershot estimates on Bay Street by a wide margin.

The inflation rate has also resided within the Bank of Canada’s target range of 1-3% for two consecutive months – the first time that’s happened since early 2021. (The bank aims for the midpoint, 2%, of that range.)

The results suggest monetary policy is working to bring inflation under control, and likely on a faster timeline than central bankers expected. In January, the Bank of Canada projected that annual inflation would average 3.2%in the first quarter. Now, money markets are pricing in a 73% chance that the Bank of Canada delivers a quarter-point cut at its June meeting, up from 50% before the report.

The Canadian data differ from that of the United States, where inflationary pressures are still running warm and the economy is posting solid growth. By comparison, the Canadian economy has slowed to a crawl as it contends with restrictive interest rates. Consumers are facing some of the highest debt payments on record, as a percentage of disposable income, while others face a payment shock when their mortgages come up for renewal. On average, consumers have reduced their spending.

It’s been almost 18 months since the October 2022 lows and in that time we have seen the stock market go from recovery to excitement. The S&P 500 up a staggering ~45% from the low of 3577 on October 12. That rally was powered by falling inflation and hopes that the Fed wouldn't be required to further tighten policy. Now, the bull market has built a full head of steam, with the mood brightening into what is looking increasingly like full-blown optimism. It’s worth noting that since last spring's dip, we've experienced only one notable phase of volatility, with equities seeing a 10% correction from August through October.

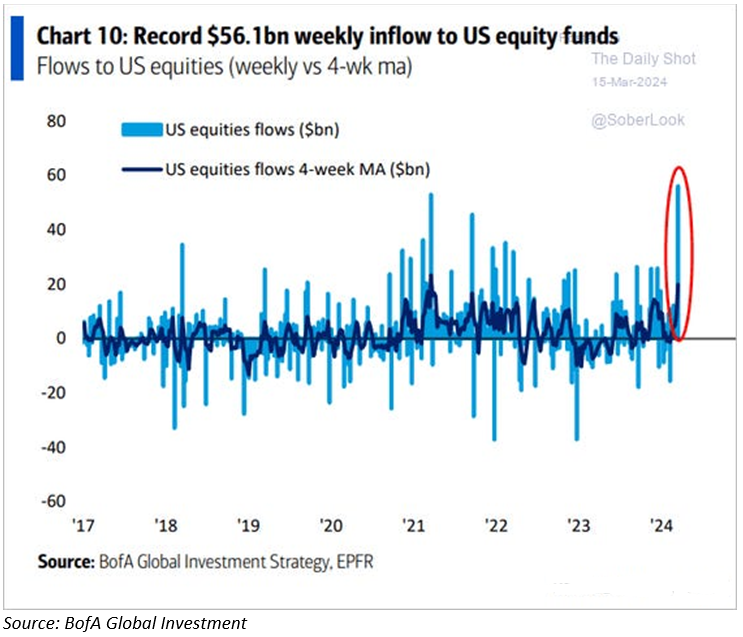

We don't expect a sequel to the correction in 2022 or the mini banking crisis last Spring, but the stock market's sharp run higher, combined with low volatility and glimmers of what we'd describe as complacency, does make this market susceptible to knee-jerk reactions (dips) in response to any disappointing data or headlines. Relative to this time last year when a recession appeared more probable, the fundamental backdrop of economic and corporate profit growth as well as eventual Fed rate cuts would, in our view, make any pullbacks a compelling buying opportunity for investors. Afterall, there still remains an outrageous amount of money waiting on the sidelines…

Last week saw record inflows into US Equity Funds of $58 bln in one week… sounds big but there is $6 trillion in Money Markets.

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.