Not Since Harry Met Sally…

DHL Wealth Advisory - Feb 23, 2024

Global Equities continued their unrelenting march to new highs this week with major benchmarks now higher six of the last seven weeks. Perhaps most topical for markets (outside of Nvidia) was Japan’s Nikkei stock index which finally surpassed...

Global Equities continued their unrelenting march to new highs this week with major benchmarks now higher six of the last seven weeks. Perhaps most topical for markets (outside of Nvidia) was Japan’s Nikkei stock index which finally surpassed its end-1989 peak. (The same year “When Harry Met Sally” hit theaters). Yes, the Japanese market has taken 34 years to regain its prior high… Putting those five different decades into perspective, Britain has had eight different Prime Ministers, Canada six, the U.S. has also had six Presidents, and we’ve lost count of Japan’s leaders over that spell. From a market perspective, the S&P 500 finished 1989 at 353.40 and Exxon Corp (before Mobil got into the mix) and General Electric were the two largest American companies by market cap, $63.84B and $58.2B, respectively. For context, Microsoft just surpassed Apple by market cap and is now worth +$3 trillion and the S&P 500 is trading north of 5,000.

Moving markets higher this week was Nvidia’s blowout earnings report Wednesday afternoon. We wont dive too deeply into company specifics, but the quarter saw NVDA report revenue of $22.10 billion for its fiscal fourth quarter, a rise of 265% year-on-year, while net income surged 769%. These types of growth figures are generally seen in the micro-cap market, not a now +$2 trillion company.

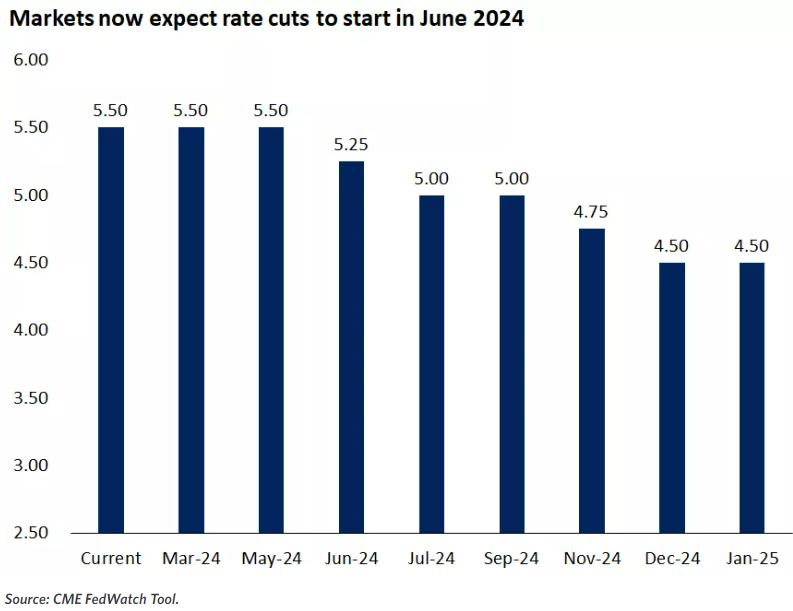

The furious rally in equities makes the Fed’s job even more complicated. Already frustrated by sticky services inflation, and a surprisingly healthy job market early in 2024, the heavy-duty loosening of financial conditions hardly calls out for the need for immediate rate relief. In fact, this week’s FOMC Minutes noted the “risks of easing too quickly”, with some concerned that “progress on inflation could stall”. Market pricing of Fed rate cuts is leaning to fewer and further out, with even the June meeting now in some doubt, and little more than three cuts in total seen for the full year (worth noting that BMO’s economics team is calling for four cuts, starting in July).

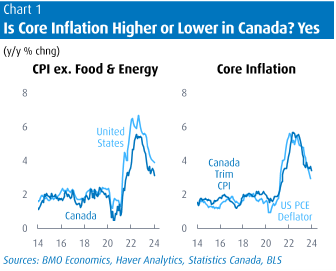

Meanwhile closer to home, Canadian consumer prices were flat in January (and down 0.1% in seasonally adjusted terms), well below consensus and mild enough to carve the headline inflation rate by half a point to 2.9%. The consensus amongst economists was 3.3%, so January’s figure is a big and welcome miss! In fact, aside from a one-month blip last June, this is only the second trip below 3% since March 2021. While there were a few random drivers—such as a deep drop in airfares—the report was broadly lower than expected, with all major measures of core inflation also taking a step back (trim down 3 ticks to 3.4% and median down 2 ticks to 3.3%).

Diving into the numbers a little further, a key feature of the latest Canadian inflation reading was that CPI excluding mortgage interest costs was precisely 2.0% y/y in January. More than one analyst swiftly pointed out that the Bank of Canada had thus achieved its target, since it was only its rate actions that were keeping headline inflation aloft. A modified version of that line is that the Bank should look through, or even ignore, mortgage interest costs (which are up 27.4% y/y, and the number one driver of inflation).

The bottom line is that there is little debate on this one: It's a much milder reading than expected, especially given the high-side surprise seen in last week's round of U.S. inflation reports, a nice contrast. Importantly, January can set the tone for inflation, since firms often take the opportunity to adjust prices for the year in this month—and there was little sign of a big January bump this year. Just as an example, both furniture and appliance prices were up in the month, but both are down from a year ago, as goods inflation fades. While no doubt welcome news, the Bank of Canada will likely remain cautious in the face of still-strong wage gains, but clearly today's result makes rate cuts much more plausible in coming months, and we remain comfortable with our call that the Bank will begin trimming in June.

Source: BMO Economics EconoFACTS: Canadian CPI (January)

These diverging trends in inflation data add to an ongoing debate since the possibility of rate cuts first came into view: Who would cut first, the Bank of Canada or the Fed? We have consistently leaned to the former, given the greater strain on the domestic economy from high rates, and a slightly cooler inflation backdrop. And the latest round of data supports that view, on both growth and inflation. Next Thursday’s National Accounts will likely reveal that Canadian GDP eked out a 1% rise in Q4, versus 3.3% U.S. growth in the same quarter. Still, the market is not fully convinced, with a June BoC cut also priced at just a bit above a 50/50 proposition. The lingering concern about early rate cuts in Canada is not so much about stoking a flaming equity market—no Nvidias in the TSX, sadly—but instead about fanning a simmering housing market. Below is a snapshot of expected US interest rates.

As we’ve noted, we expect inflation to moderate in the U.S. and Canada, although likely not in a straight line lower. This may mean stock markets may encounter volatility along their path this year. But for investors, this could also mean opportunities, especially for those who weren’t able to fully participate in the rapid rally that began late last year.

While pullbacks are likely and even expected in any given year, we do not see the scope for these pullbacks turning into more nefarious bear markets, given the fundamental backdrop. We recommend using market volatility to add to and diversify portfolios, especially ahead of a potentially multiyear central bank rate-cutting cycle that will likely begin later this year.

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.