S&P 4,999.89 Doesn't Quite Have the Same Ring...

DHL Wealth Advisory - Feb 08, 2024

Stocks have rallied sharply the last 3-4 months. In fact, the S&P 500 hit a new record of 4,999.89 in Wednesday trading – a mere 0.0002% away from the 5000 level. Directionally, we think the market has this right, with the recent rally powered...

Stocks have rallied sharply the last 3-4 months. In fact, the S&P 500 hit a new record of 4,999.89 in Wednesday trading – a mere 0.0002% away from the 5000 level. Directionally, we think the market has this right, with the recent rally powered by expectations for the Fed to pivot toward looser monetary policy, which has historically been a tailwind for market returns. That said, the market was prone to overreactions over the last year, with pullbacks last February and August-October coming as the market adjusted its expectations.

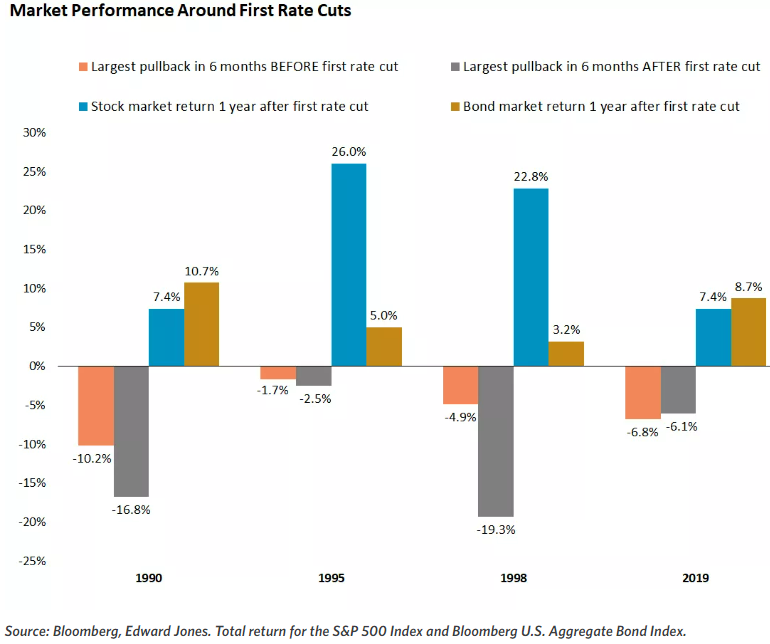

While a shift toward less restrictive Fed policy this year is broadly favorable for financial markets, it won't come without hiccups. Looking back at initial Fed rate cuts in 1990, 1995, 1998 and 2019 (this excludes the rate cuts in 2000 and 2007 that were accompanied by popping market and housing bubbles, conditions that we don't see as parallels to today), noticeable stock-market pullbacks occurred before and after the rate cut (save for 1995, which didn't experience even one 5% pullback during the year). However, these spates of market weakness proved to be buying opportunities for both stocks and bonds. In fact, the average return 12 months after the first cut is a very respectable 15.9%.

We don't think the market is set up for a dramatic downturn, but we do think investors would be well served to anticipate a few bumps as we advance. We'd highlight that it was particularly encouraging to see that markets didn't use the hotter-than-expected U.S. wage-growth number as a catalyst to sell off (under an interpretation that wages will disrupt the inflation trend and keep the Fed in a restrictive stance for longer). We think this was a rational (non)reaction in equities (though bond yields did erase their midweek decline), and, in our view, reflects the wider view that the healthy economy is good for rising corporate profits, which we believe will be the main character in further equity-market gains in 2024.

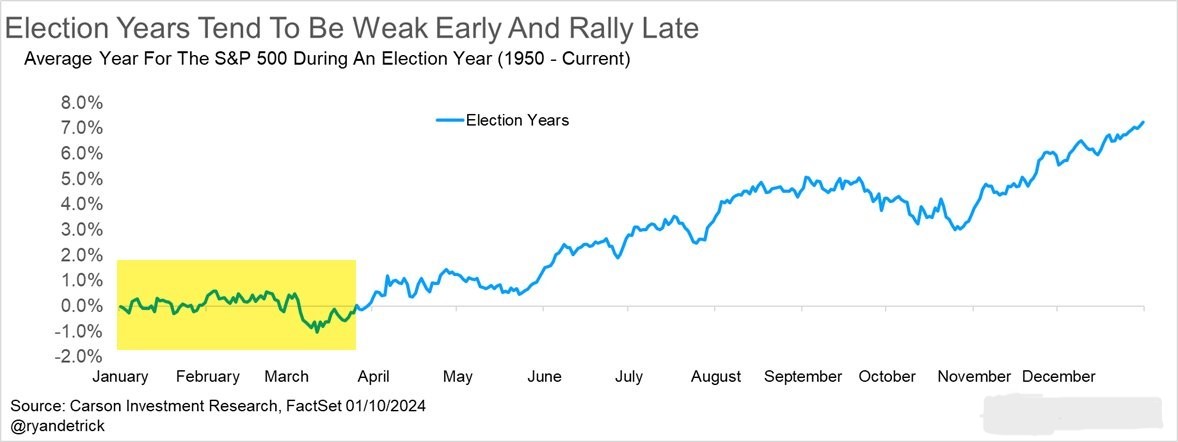

We will end today’s shorter edition with another interest table. In addition to the tailwinds of a first rate cut, market tends to do well in Election years, which is something we will see this fall. Looking back, history would show that stocks tend to start slow in an election year but really pick up in the Spring, which could also coincide with the first rate cut…

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.