Goldilocks and the Federal Reserve

DHL Wealth Advisory - Jan 26, 2024

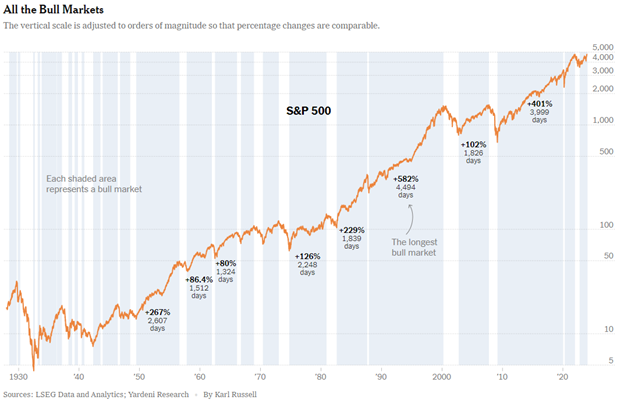

US Markets finish off another winning week, fueling calls that a new bull market has already begun. Despite muted performance today, the S&P 500 has climbed for the past six sessions and closed at a record high for five straight trading days...

US Markets finish off another winning week, fueling calls that a new bull market has already begun. Despite muted performance today, the S&P 500 has climbed for the past six sessions and closed at a record high for five straight trading days, eclipsing the 4,796.56-record set just over two years earlier. While extremely optimistic, the majority of this growth has been relatively narrow, dominated by the larger caps while many smaller stocks have still not escaped the jaws of the bear market. We still expect to see a broadening in the market this year but such strong momentum coupled with positive economic data is comforting for a potential ‘Goldilocks’ landing.

Economic data was also a catalyst for markets this week as the the U.S. economy posted yet another year of solid activity, while price pressures eased. Growth in the fourth quarter came in much stronger than expected, providing a nice handoff to Q1, and setting the stage for the expansion to continue in 2024. This now marks six consecutive quarters with growth of 2% or better. Not a bad run for an economy that was supposed to be struggling under the weight of higher rates..

The Fed is expected to remain on the sidelines next week. But, with the mighty consumer still fueling economic activity, we’re not expecting a pivot anytime soon.

Source: BMO Economics EconoFACTS: U.S. Q4 GDP — An Upside Surprise… Again!

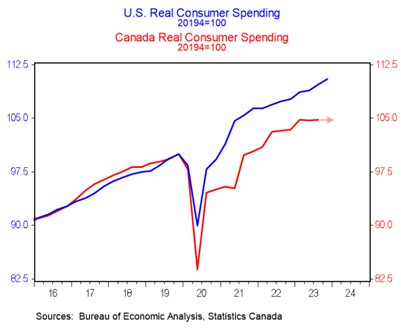

Typically, robust activity south of the border provides a nice lift to the Canadian economy too. But, we've seen a diverging growth profile this cycle primarily due to the stark difference between U.S. & Canadian households. American consumers continued to flex their muscle in Q4 as spending climbed 2.8% annualized. Meantime, Canadians remain under severe pressure. We won’t get Q4 figures from StatCan until the end of February, but it looks like consumer spending stalled for a third straight quarter. There are a few reasons for the divergence. One key contributing factor is the availability of the 30-year fixed rate mortgage in the U.S.—many homeowners were able to lock in mortgages when rates were at rock bottom, effectively shielding them from the Fed’s tightening campaign. Meantime, as the BoC’s recent MPR noted: “many Canadians are facing upcoming mortgage renewals and record-high levels of household debt.” That will result in muted consumer spending this year that will ultimately weigh on growth.

Source: BMO Economics AM Charts: January 26, 2024

On Wednesday the Bank of Canada held policy rates at 5.0% as widely expected for the fourth consecutive meeting. The overall tone was generally cautious about the stickiness of core inflation and the economic outlook, but a couple significant phrases were dropped from the commentary, indicating the next move in rates is likely downward. The key takeaway is that the rapid and sizable rate hikes over the past two years are doing their job, but it looks like we'll be at 5% for a while yet as the BoC wants to see a further slowing in inflation. BMO's call for a June start to rate cuts looks perfectly reasonable at the moment.

Source: BMO Economics AM Charts: Bank of Canada Rate Decision & MPR — Patiently Waiting

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.