2024 Market Outlook

DHL Wealth Advisory - Jan 05, 2024

Thank you 2023, you were a welcomed reminder that equity markets can indeed go higher after an absolutely dreadful 2022. With the Canadian and US economies having so far avoided recession, inflation retreating, and visions of rate cuts dancing...

Thank you 2023, you were a welcomed reminder that equity markets can indeed go higher after an absolutely dreadful 2022. With the Canadian and US economies having so far avoided recession, inflation retreating, and visions of rate cuts dancing in our heads, North American equities finished the year riding the coattails of a Santa Claus rally that saw nine consecutive weeks of gains for major indexes. Why?

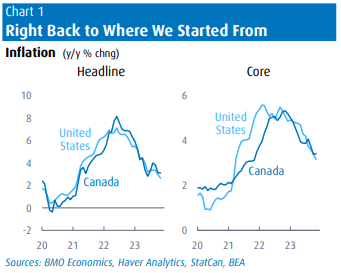

Some of you may recall at this time last year it was widely expected that global economies would plunge in to recession following an unprecedented rate hiking campaign out of global central banks in an effort to combat rampant inflation. Well, inflation has plunged across most major economies from last year’s peak without the assistance of a recession. In fact, most G10 economies performed better than expected in 2023, and yet inflation eased largely on script. And this welcome retreat in headline inflation, with core in tow, is setting the stage for rate relief in 2024. In turn, financial markets enjoyed a relatively solid year, nearly reversing the brutal performance for both stocks and bonds in 2022. Thus, after inflation’s two-year reign of terror, and a sustained episode of rising rates, the switch will flip in the coming year as central banks begin the process of unwinding heavily restrictive policies.

We think 2024 will build on this year’s gains, but not without some bumps along the way. However, before we get into our outlook, let’s look back at how 2023 stacks up against history. Spoiler: It’s in good company. As we mentioned in our opening sentence, this year was a powerful reminder of the importance of a long-term, disciplined investment strategy, and the value of an opportunistic approach during bouts of market pessimism.

Winning streaks

- Stocks extended their winning streak last week, with the S&P 500 rising for nine consecutive weeks – the longest since 2004. In the past 50 years, there have been only three longer streaks, with the last occurring 20 years ago. While the duration is impressive, so too is the gain during this run, up an amazing ~15%.

- This is yet another reminder of how quickly pain can turn to gain in the stock market. Equities were under pressure through the fall as interest rates surged to a new high for the year. Patience was rewarded, however, when rates reversed course and stocks mounted what has now become a run for the record books for the S&P 500.

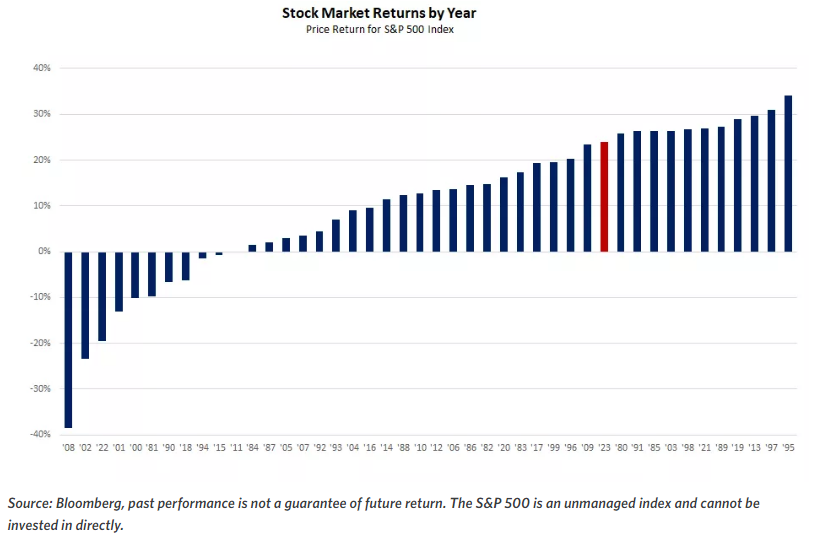

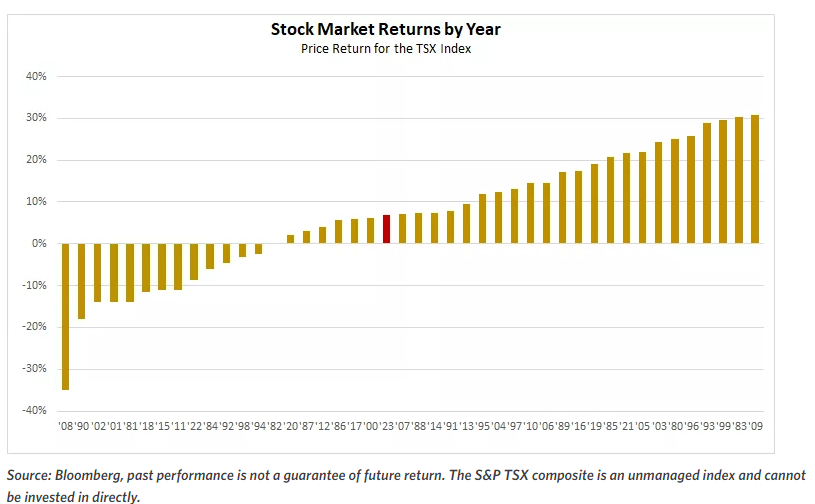

Annual equity returns

- 2023 ranks as the 12th best year for the S&P 500 since 1980. For the 11 that were better, the stock market gained an average of 8% in the subsequent year, indicating strong years often see a favorable encore. In terms of sector performance, it was technology, communication services and consumer discretionary sectors were the clear leaders, with each gaining more than 40% on the year, consumer spending..

- While positive, Canada’s TSX experienced a much more average year given our lack of technology exposure and concentration to Financials, Materials, and Energy. These “value” sectors were laggards for much of 2023.

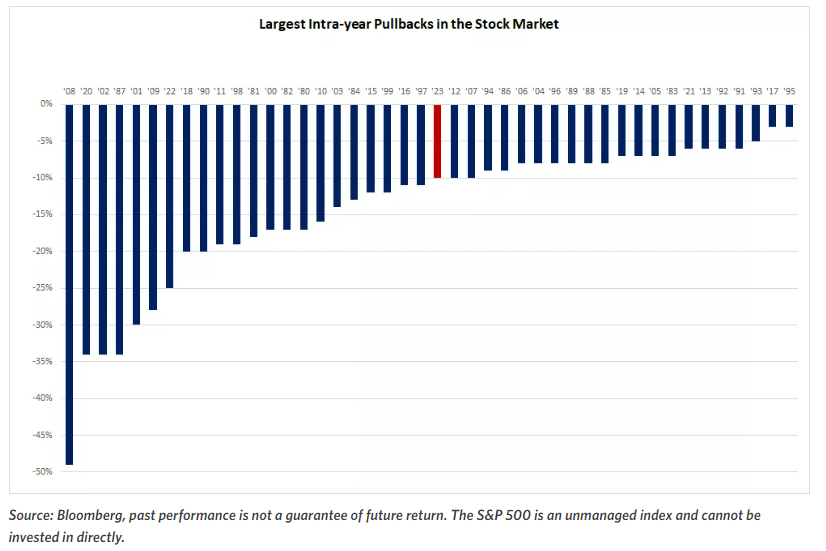

Volatility and Largest pullbacks

- Using the S&P 500 as a broader gauge for equities, 2023 saw two notable pullbacks: an 8% drop during February and March, and a 10% correction from August through October. Looking at the largest intra-year drawdowns in the stock market since 1980, this year’s landed in the middle of the pack. We often remind our readers that “corrections are natural, normal and a healthy part of a market. They just don’t feel like it when you’re in one”.

- The bear market declines in 1987, 2001-2002, 2008-2009, 2020, 2022 are obvious standouts to the downside. Conversely, 1995 and 2017 are remarkable in that the stock market never experienced a pullback of more than 3% during the year.

- The largest intra-year pullback has averaged 14% since 1980, yet during that 44-year stretch, the stock market finished higher for the year 77% of the time. This underscores how important it is to stay the course when the going gets tough. Again, to use one of our favourite cliché’s: It’s not about timing the market, but rather time in the market.

Looking forward, we expect 2024 to be no different and investors will undoubtedly endure a new set of bumps and turns. The first of which may come from a realignment of expectations for central bank policy if markets fail to see rate cuts emerge as soon as hoped, particularly from the U.S. Fed. However, while it might not feel that way in the moment, we think sell-offs will prove to be temporary setbacks within the larger ongoing bull market.

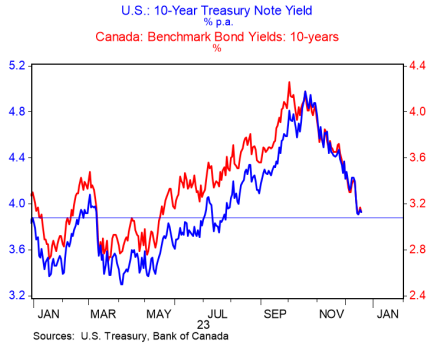

Interest rates

- Oh our favourite topic for the last 2 years… Interest rates have been the driving influence over the market since officials unleashed a wave of inflation following the lockdowns of Covid-19. We think 2023 brought an inflection point in the overall interest rate backdrop, with the October peak in yields proving to be the high-water mark for this cycle.

- 10-year benchmark interest rates have fallen sharply to finish out 2023. The 10-year Government of Canada bond yield topped 4% in October, the highest since 2007, but is now on the verge of falling through 3%. While we don’t expect the slope of the decline to persist in the near term, we do expect moderating inflation and eventual BoC and Fed rate cuts to normalize the yield curve.

Economic growth

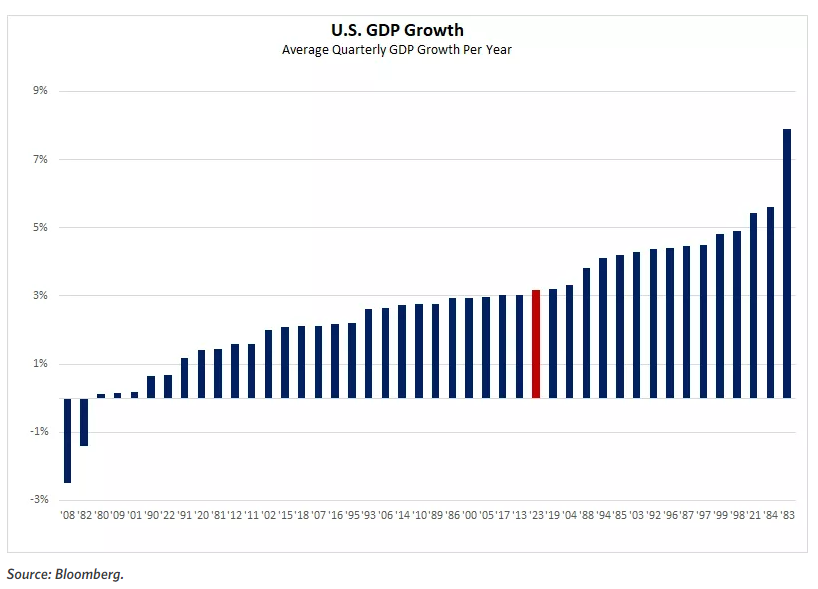

- Domestic quarterly GDP growth has averaged less than 1% through the first three-quarters of 2023, with the Canadian economy contracting last quarter as economic momentum has waned. Meanwhile, average quarterly U.S. GDP growth in 2023 topped 3% for just the 16th year since 1980.

- The consumer was the star of the economic show in 2023, driven by a historically strong labour market. In fact, Canada's unemployment is up only slightly from the historic low of 4.9% while the U.S. unemployment rate reached its lowest point (3.4%) going back to 1980.

- It is only natural for the strong US economy to lose some steam through the first half of 2024 as the effects of restrictive monetary policy continue to work their way through the system. In addition, we expect the pace of consumer spending growth to slow, with excess savings drawn down and wage gains moderating. Importantly, however, we expect the labour market to soften rather than crack, preventing a more severe downturn or even a traditional recession. As the BoC and Fed start cutting rates and other components of the economy — such as capital investment and manufacturing — pick up, we think GDP growth will see renewed strength in the back half of 2024.

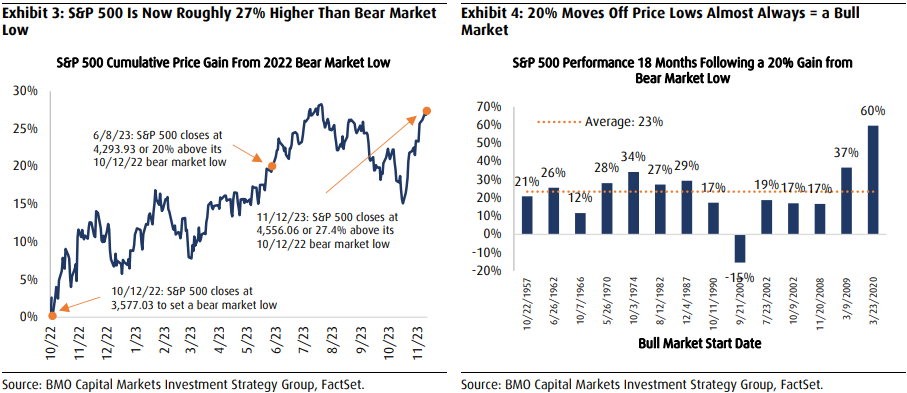

Turning our attention to 2024, we continue to believe that US stocks are in a bull market that has now entered its second year. Why? The S&P 500 closed more than 20% above its 10/12/22 bear market price low on June 8, a feat commonly accepted to mark the start of a new bull market. In fact, once the overall market has climbed 20% above its previous price low, that low signaled the start of a new bull market in all but one of the prior 14 instances (Exhibit 3)

However, it will be difficult for the market to replicate the gains of 2023 given historical bull market performance patterns that suggest lower, but still solid gains, in the second year of a bull market. For context, BMO strategists find that the S&P 500 has historically gained an average of 11.1% during year two of bull markets, much smaller than the 38.3% average gain seen in year one, but still a double-digit return, nonetheless.

Stating the obvious, Canadian investors weren’t rewarded the same way as our neighbours to the South. In fact, the S&P/TSX posted its worst performance versus the S&P 500 since 2015. Yes, this comes after strong outperformance relative to most other developed markets, including the US, in 2022. However, for our part, we believe the depth of underperformance underscores the paralyzing pessimism that traditionally persists in Canada relative to the increasingly clear fact that recent softness in domestic economic activity is more than priced in at current valuations. Furthermore, the economic “Armageddon” that most investors have been basing their investment decisions on for the past several months has not occurred and has once again been way overblown. Indeed, given the strong value position of the TSX relative to other global markets, we continue to believe Canada is well-positioned for an extended period of NORMALIZATION that we expect to unfold over the coming years.

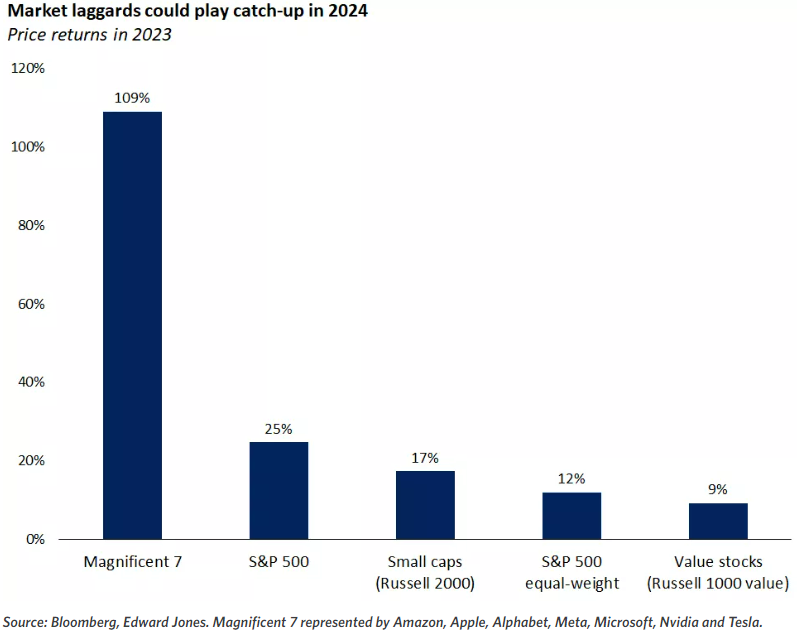

It is no secret that 2023 S&P 500 gains have been primarily driven by a handful of mega-cap stocks – most obviously depicted when looking at the Magnificent 7: Apple, Microsoft, Amazon, Meta, Tesla, Nvidia and Google. If you didn’t own any of these stocks, you didn’t generate much alpha.

We believe it is highly unlikely that these trends can continue into 2024 and expect the rest of the index to perform significantly better on a relative basis next year. So, what does this mean from an investment perspective? In a simple sense, we believe investors will need to own a little bit of “everything” and not tilt too far in one direction or another from a sector, style, and size perspective – a sharp contrast to the trends that prevailed during 2023. However, this should not be interpreted as a recommendation to be more passive when making decisions – to the contrary, we believe active investment strategies will be even more important next year as many of the largest stocks that drove performance within sectors are unlikely to maintain that momentum in 2024, forcing investors to search for other opportunities further down the market cap spectrum.

There’s little doubt that 2023 proved to be a positive year for investors: We saw strong gains across sectors, styles and market caps. A very different picture than 2022 where cash was the only positive asset class. 2023 is yet another reminder for investors to the importance and value of staying invested, even as click-bait headlines consistently paint a less-than-rosy picture.

No doubt 2024 will bring its own twists and turns in the market narrative: We have a US Election, geopolitical conflict, still high, but slowing inflation, and an interest rate backdrop that is still the highest in almost 20 years. But there are reasons for optimism as we head into the new year. Interest rates have likely peaked as the Fed starts paving the road for rate cuts, inflation continues to moderate, corporate earnings are rebounding, and valuations outside of the big year-to-date gainers remain reasonable. The markets have endured two World Wars, a Cold War, Covid 19, Spanish Influenza, a Great Depression, political assassinations, and terrorist attacks. Yet despite all this, the S&P 500 is currently less than 1% away from a new all-time-high…

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.