Keep Calm And Carry On.

DHL Wealth Advisory - Dec 08, 2023

North American benchmarks took a much-deserved breather this week following a string of five consecutive weekly gains for most major indices. Nothing in particular was driving markets as we enter a seasonally quiet period...

North American benchmarks took a much-deserved breather this week following a string of five consecutive weekly gains for most major indices. Nothing in particular was driving markets as we enter a seasonally quiet period. However, investors did have the Bank of Canada on deck Wednesday with a widely expected “hold” on interest rates for a third consecutive meeting.

The tone of the policy statement didn't provide much drama either, balancing the weakening economic backdrop with the still-elevated level of inflation and wage growth. The Bank stated that they are "still concerned about risks to the outlook for inflation and remains prepared to raise the policy rate further if needed." While there was some focus on the fact that the Bank did not repeat October's phrase that "inflationary risks have increased", that initial comment had frankly been a bit of a surprise at the time and didn't jibe with their other remarks.

It's now crystal clear that the economy is weakening, and the Bank reiterates that it sees that slowdown. Even so, inflation just isn't quite there for a more dovish official message—not with core still parked around 3-1/2%. The Statement also highlighted that wage growth remains elevated in the 4%-to-5% range. Yet, the Bank also states that "the economy is no longer in excess demand", pointing to a further slowing in inflation ahead on balance.

Source: BMO Economics EconoFACTS: BoC Policy Announcement

The Bank again gamely said that it is "prepared to raise the policy rate further", even if no one is looking for further hikes, and the conversation has completely moved on to when cuts will commence. Maintaining the hiking bias is likely driven entirely by a desire to continue dampening Main Street inflation expectations and keeping a lid on housing speculators, even as markets are pricing in more than 100 bps of cuts next year.

Source: BMO Economics EconoFACTS: BoC Policy Announcement

Bottom Line: Given the Bank's goal of restoring its inflation-fighting credibility among the broader public, the BoC could very well wait as long as possible before shifting to a dovish bias and then to cuts. Assuming the economy doesn't weaken materially further in the next few months, the policy rate trajectory is entirely dependent on the evolution of inflation. We suspect that while the underlying trend in inflation will improve in 2024, there will be bumps along the way, keeping the Bank on hold a bit longer than the market currently anticipates. But it is safe to say that the countdown clock to rate cuts has begun, even if the Bank isn't saying so.

Source: BMO Economics EconoFACTS: BoC Policy Announcement

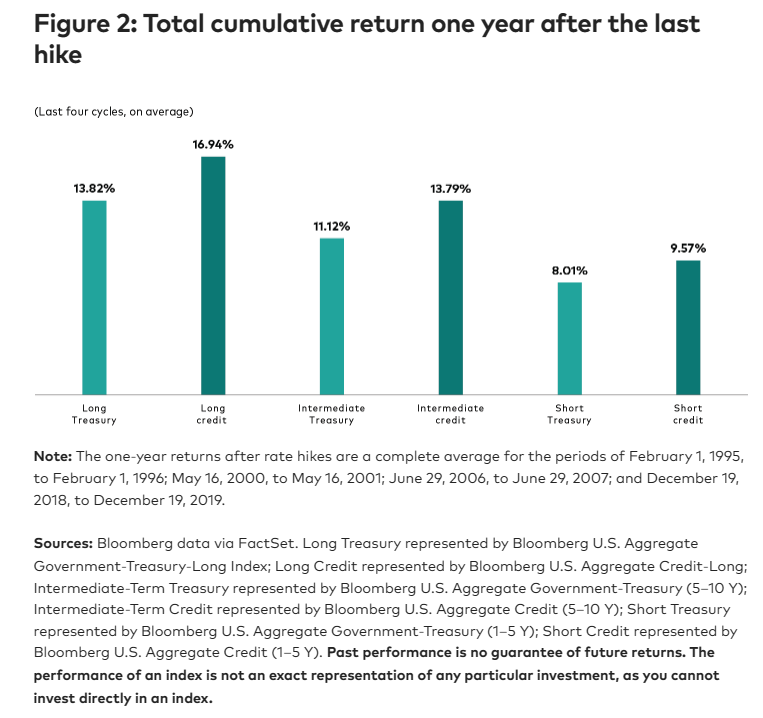

So what does history tell us if we are getting closer to a confirmation of peak rates? Well, with each passing week we are seeing more and more data that suggests the same outcome: Be constructive on financial investments. We noted in late October that we believed rates could be peaking, which could be a catalyst for a rally. The below table illustrates the 12-month return of the prior four interest rate cycles for the fixed income space. The takeaway is that after an awful 2022 and a flatlined 2023, the beaten-up fixed income space could show some signs of life – an asset class we have been adding weight to in our discretionary mandates in recent months.

Meanwhile, leadership in recent weeks has come from cyclical areas of the market, as well as those areas most sensitive to the drop in interest rates. Small-cap stocks have outperformed, gaining more than 13% since late October. Leadership also came from the financial services and consumer discretionary sectors, as well as technology and real estate, with the former reflecting a favourable outlook for the economy, while the latter benefited from relief on the rising-rate front. All four of those sectors rose more than 10% over the last month. Historically these are not the areas of the market that do well if we were teetering into a recession. In fact, they would mostly all be cratering as the market would be developing a much more defensive posture.

The complexion of market recoveries is often affected by the factors that induced the bear market. Thus, the current march toward previous highs will, in our view, be directed by the path ahead for inflation, which will set the stage for central bank interest-rate decisions, ultimately influencing the health of the economy.

The good news here is that inflation is headed in the right direction. The heart of the November rally was the latest consumer price index readings, which showed inflation remains in a downtrend, even as the economy has shown some resilience.

We think the year ahead will bring some challenges (shifting Fed policy expectations, a potential economic growth scare, political and geopolitical uncertainties) that will spark periodic pullbacks, but a return to new highs is likely in the cards. The upshot: Looking back at the recoveries since 1980, when the market finally reaches the previous peak, stocks have typically gone on to deliver a double-digit return in the ensuing year, reflecting, in our view, the progression of renewed economic, monetary-policy and earnings cycles.

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.