S&P 493...

DHL Wealth Advisory - Dec 01, 2023

Thank you, November! Global markets ended a dreadful 3-month period of declines with a bang this month. Both the Dow Jones and S&P 500 finished November with a 8% gain, while the Nasdaq advanced roughly 10%...

Thank you, November! Global markets ended a dreadful 3-month period of declines with a bang this month. Both the Dow Jones and S&P 500 finished November with a 8% gain, while the Nasdaq advanced roughly 10%. The latter two averages had their best monthly performance since July 2022 and are now just 1% away from 2023 highs. Meanwhile, always playing the irrelevant step child, Canada was a minor laggard this month with a 7% gain.

A lot of what we have seen in November is just a realization that the US economy is still doing well, that consumers are resilient and that North American Central Banks are essentially on hold. For 2022, we spent so much time thinking about what could go wrong, and we really didn’t spend any time thinking about what could go right. 2023 is a story of a lot of things going right.

Data released Thursday showed that the US personal consumption expenditures price index—the Federal Reserve’s favorite inflation gauge—rose 3.5% on a year-over-year basis, a slowing from a 3.7% annual gain in prior month. These numbers were the latest in a string of positive inflation data seen in November that caused traders to conclude the Federal Reserve is likely done raising rates and could even begin lowering them in 2024.

The 10-year Treasury yield, which had spooked investors by rising above 5% last month, collapsed this month as the cooling inflation data rolled out, helping to boost sentiment for equities. The 10-year yield traded under 4.3% this past week.

The goldilocks conversation is a little different on our side of the border. On Thursday we learned that Canada’s economy shrank in the third quarter, adding fuel to the narrative that the Bank of Canada will need to lower interest rates soon to avoid a deep recession. Canadian Real GDP fell at a 1.1% annual rate in Q3 versus a consensus call of +0.1%. However, before we let slip the dogs of recession, note that the prior quarter was revised heavily upward to a rise of 1.4% (from -0.2%), thus avoiding the dreaded "two quarters in a row of declining GDP".

Whatever label you slap on this economy, it's basically not growing, despite the artificial sweetener of rapid population growth. But reinforcing the point that it doesn't quite sink to the level of recession, the initial read on monthly GDP for October was a surprisingly perky +0.2%, confounding expectations that activity would shrink in Q4.

For the third quarter, the weakness was broad based, but business investment was especially clunky (-10.1%.). Consumer spending barely grew (+0.1%), but that was about as expected. Net exports and inventories both dragged, with exports (-5.1%) a big disappointment to expectations. The lone high side surprises were government spending (+6.5%; perhaps not where you want to see the growth) and residential construction (+8.3%).

Source: BMO Economics EconoFACTS: Canadian Real GDP (Q3, September)

Bottom Line: There are plenty of unexpected cross currents in yesterday’s Stats Canada release, but the big picture is that the Canadian economy is struggling to grow, yet managing to just keep its head above recession waters. One way to capture that is that in the six months to September GDP rose 0.04%, or basically unchanged. The significant (upward) revisions to Q2 show us to not read too much into the decimal points on this report—don't like today's news?; Just wait, it will change tomorrow. So, overall, the mixed report reinforces the point that the Bank is done hiking rates, but doesn't really advance the cause for rate cuts, as the economy isn't showing signs of further deterioration early in Q4.

Source: BMO Economics EconoFACTS: Canadian Real GDP (Q3, September)

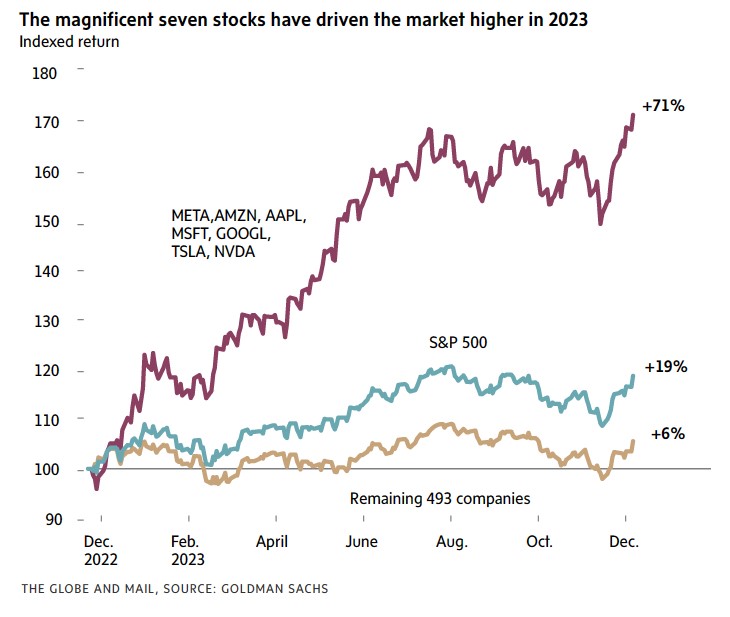

Turning back to the markets, the narrow leadership of the S&P 500 this year can raise questions about the value of diversification. The S&P 500 index has risen by over 18% year-to-date, while the S&P 500 equal-weighted index has seen a more modest 4% rise, highlighting that much of this year's gain has been driven by the indexes' largest companies. In fact, it might be a little early to summarize 2023, but if the year were to end today… There’s no doubt that 2023 could be summarized with just this single chart:

The above illustration shows how much the year-to-date returns of the S&P 500 area concentrated in just the Magnificent 7. Those names are up ~70%; The S&P 500 is up +19%. And the index of the other 493 is a meager 6%... Today, the top three sectors of the S&P 500 comprise over 50% of the index, and the 10 largest stocks account for over 30%.

However, market leadership can change over time. In 2008 the energy sector accounted for a larger portion of the S&P 500 than the information technology sector. Today, Apple alone is nearly double the size of the entire energy sector.

We would acknowledge that the higher weights of the indexes' largest companies and sectors reflect the strong outlook for these businesses, and they certainly have a place as part of a broader diversified portfolio. However, as we saw this past March with the collapse of Silicon Valley Bank, market sentiment can change in a hurry.

2023 has been a notable year so far for small-cap stocks, but for the wrong reasons. The Russell 2000, a proxy for U.S. small-caps, is on pace to trail the S&P 500 by about 15%, the widest margin in a calendar year since 1998. Worries about an economic slowdown and high interest rates on the back of aggressive Fed tightening have been the main culprits for the underperformance. Smaller companies have less pricing power to offset inflationary pressures and lean more on financing to run their businesses than their large counterparts.

But could this underperformance present an opportunity as we turn the page on 2023? While growth is slowing, the economy has proven resilient, inflation has fallen by about two-thirds, and the Fed is preparing to end its tightening campaign. Rates will likely stay elevated compared with history, but as the headwind of rising yields subsides, small-caps and value could play catch-up…

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.