Are We There Yet?

DHL Wealth Advisory - Nov 03, 2023

It was an enormous week for global equites (best since Oct 2022) following the US Federals Reserves decision to leave rates unchanged at 5.25-5.50%. Moving markets, however, was the expectation of future interest rate hikes, or lack thereof...

It was an enormous week for global equites (best since Oct 2022) following the US Federals Reserves decision to leave rates unchanged at 5.25-5.50%. Moving markets, however, was the expectation of future interest rate hikes, or lack thereof. After almost two years of aggressive monetary tightening, the world's biggest central banks are taking time out before weighing up their next move.

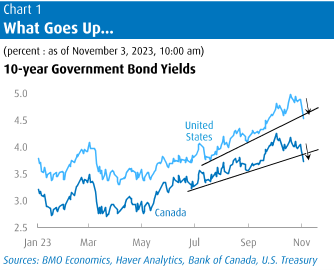

When we all look back at this highly unusual and extremely eventful cycle, it may be no exaggeration that this week will be viewed as a watershed. A confluence of major events came together in recent days to apparently break the fever in long-term interest rates, the U.S. dollar, and perhaps even bearish sentiment among consumers and businesses. The major spark was Wednesday’s FOMC meeting, which helped drive a 40 bp plunge in 10-year Treasury yields over a matter of three sessions. After piercing the 5% level only recently, this week’s huge rally took them down below 4.5%.

Source: BMO Economics Talking Points: The Global Pause that Refreshes

While the no-hike was expected, there was considerable uncertainty over where the rate-setting Federal Open Market Committee would go from here. Judging from documents released Wednesday, the bias appears toward more restrictive policy and a higher-for-longer approach to interest rates. Projections released in the Fed’s dot plot showed the likelihood of one more increase this year, then two cuts in 2024, two fewer than were indicated during the last update in June. That would put the funds rate around 5.1%.

As we have discussed in prior editions, talking tough by the Fed is almost as important as acting tough. Leaving the door open for one additional hike keeps financial conditions sufficiently tight and inflation expectations in check. As we learned by the Canadian “pause” experiment earlier in the Spring when the Bank of Canada formally announced a “pause” or “end” to its interest hiking campaign, financial conditions loosened much too quickly and inflation picked up. Instead, officials will be data dependent from meeting to meeting while leaving the possibility of additional hikes on the table.

In recent public appearances, Fed officials have indicated a shift in thinking, from believing that it was better to do much more to bring down inflation to a new view that is more balanced. That’s partly due to perceived lagged impacts from the rate hikes, which represented the toughest Fed monetary policy since the early 1980s.

There have been growing signs that the central bank may yet achieve its soft landing of bringing down inflation without tipping the economy into a deep recession. However, the future remains far from certain, and Fed officials have expressed caution about declaring victory too soon. While a share of past policy tightening is still in the pipeline, the Fed can go into wait and see mode, hence the pause.

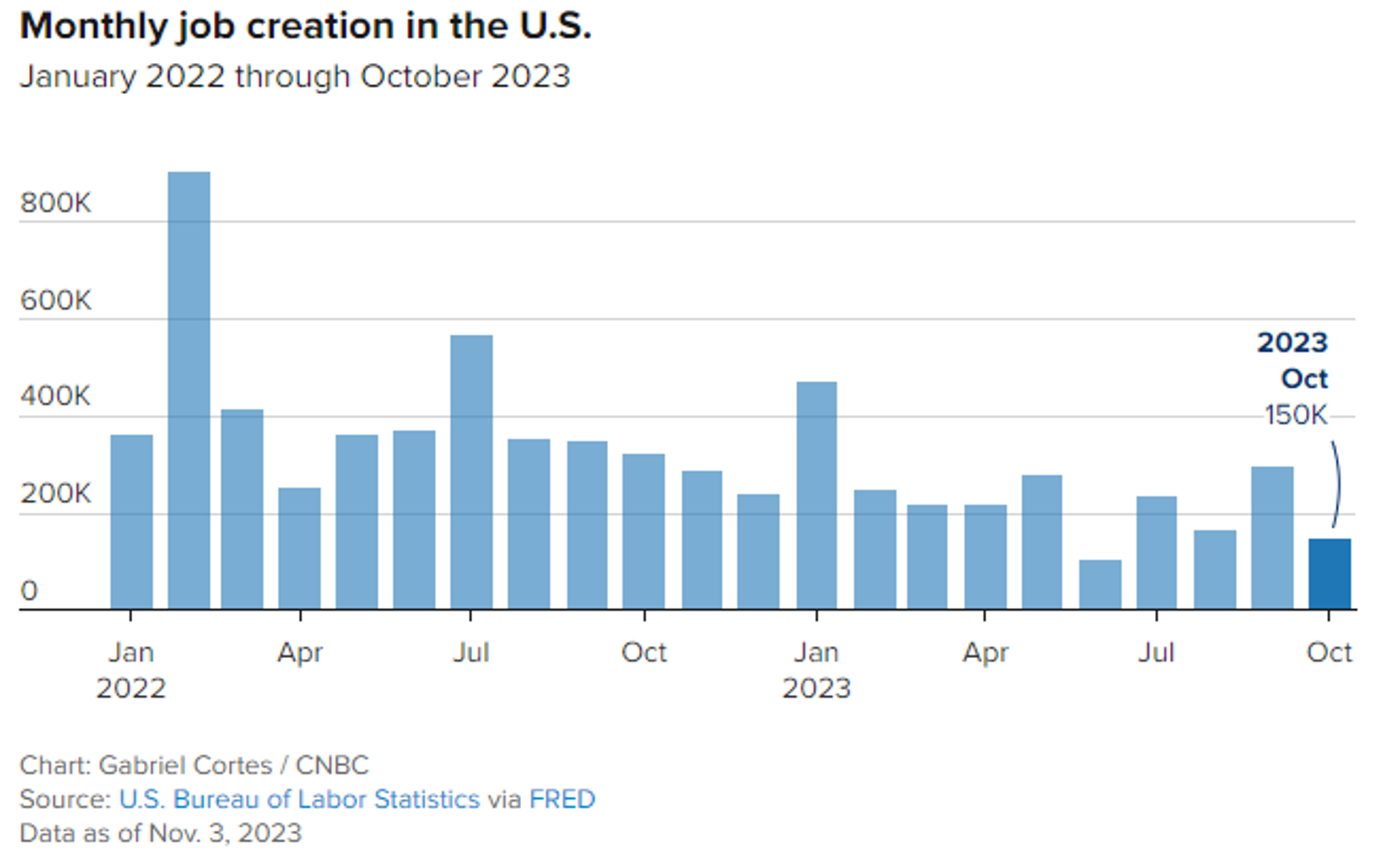

Further strengthening the case of a pause and possible end to hiking is the US Labour market. On Friday we saw the U.S. economy add fewer jobs than expected in October, confirming persistent expectations for a slowdown and possibly taking some heat off the Federal Reserve in its fight against inflation. Nonfarm payrolls increased by 150,000 for the month, below the consensus forecast for a rise of 170,000.

The unemployment rate rose to 3.9%, the highest level since January 2022, against expectations that it would hold steady at 3.8%. A more encompassing jobless rate that includes discouraged workers and those holding part-time positions for economic reasons rose to 7.2%, an increase of 0.2 percentage point. The labor force participation rate declined slightly to 62.7%, while the labor force contracted by 201,000.

Average hourly earnings, a key measure for inflation, increased 0.2% for the month, less than the 0.3% forecast, while the 4.1% year-over-year gain was 0.1 percentage points above expectations. The average work week nudged lower to 34.3 hours. Following Friday’s jobs data, markets further reduced the probability of a rate hike in December to just 10%, according to a CME Group gauge.

Yet while this week may mark a watershed, we can forgive future financial historians from wondering precisely what the trigger was for such widespread jubilation. After all, the Fed’s decision to pause was not new—it’s the third FOMC meeting this year on hold—nor was it the least bit surprising, as Fed speakers had well-telegraphed the outcome. Some pointed to the mention of tighter financial conditions in the Statement, but many, many Fed officials had noted that in recent weeks. (As well, the furious rally of recent days has gone a long way to reversing said “tighter” conditions.) And Chair Powell’s remarks at the press conference were appropriately guarded, with precisely zero promise that the Fed was done. Even so, markets have almost fully priced out any odds of additional hikes and are expecting cuts by the middle of 2024.

Source: BMO Economics Talking Points: The Global Pause that Refreshes

This week’s heavy onslaught of economic data was not especially shocking either, although the skew was fairly consistent to the soft side of expectations. Friday’s jobs report for October was arguably the perfect tonic for an ailing market. We will studiously refrain from the tired cliché of calling it a Goldilocks result, even if it was neither too hot—hourly earnings cooled to 4.1%—nor too cold—job gains were still 150,000—but just right: the unemployment rate nudged up a tenth to 3.9%. Papa bear may note that the household survey, which often catches turning points earlier than its payrolls sibling, reported a deep 348,000 job loss. Besides a cooler jobs result, both the factory and services ISM came in well light of expectations, reinforcing the view that GDP will decelerate noticeably in Q4 after the 4.9% Q3 blowout. We remain comfortable with our call of just under 1% this quarter; and note that the Atlanta Fed’s early read on its GDPNow is 1.2%.

Source: BMO Economics Talking Points: The Global Pause that Refreshes

The better news for bonds was not exclusively a U.S.-driven story. Last week saw both the Bank of Canada and the ECB also choose to pause, while the Norges Bank and the Bank of England joined the cool kids on the sidelines this week. Actually, the truly cool kid is the central bank of Brazil, which led on the way up and slashed its Selic rate 50 bps this week, the third such cut this year.

Source: BMO Economics Talking Points: The Global Pause that Refreshes

Meanwhile Canadian GDP remains in a funk, with flat the new up. After a burst of activity in the opening month of 2023, the Canadian economy has since seen essentially no growth, as measured by the monthly GDP reports. Some analysts point to a series of special events as causing the prolonged lull, but that excuse wears thin after eight months of no growth. Canada may not be in a recession, but it’s the next worst thing. The employment report reinforced the point, as the jobless rate rose another two ticks to 5.7% in October, even as the economy managed to add 17,500 jobs. But with raging population growth, that’s simply not nearly enough to keep the labour market from softening on net—the economy now requires about 50,000 new jobs per month to keep the unemployment rate stable. Adding insult, all of the latest jobs were part-time positions, keeping total hours worked steady.

Source: BMO Economics Talking Points: The Global Pause that Refreshes

The Bank of Canada thus now looks more firmly pinned to the sidelines. While Governor Macklem sounded somewhat even-handed last week, he has also more openly talked about what could start to bring rates down, and how we don’t need to see inflation back at 2% to begin the proceedings. The modest recovery in the Canadian dollar in the past week also removed a pressure point on the Bank.

Source: BMO Economics Talking Points: The Global Pause that Refreshes

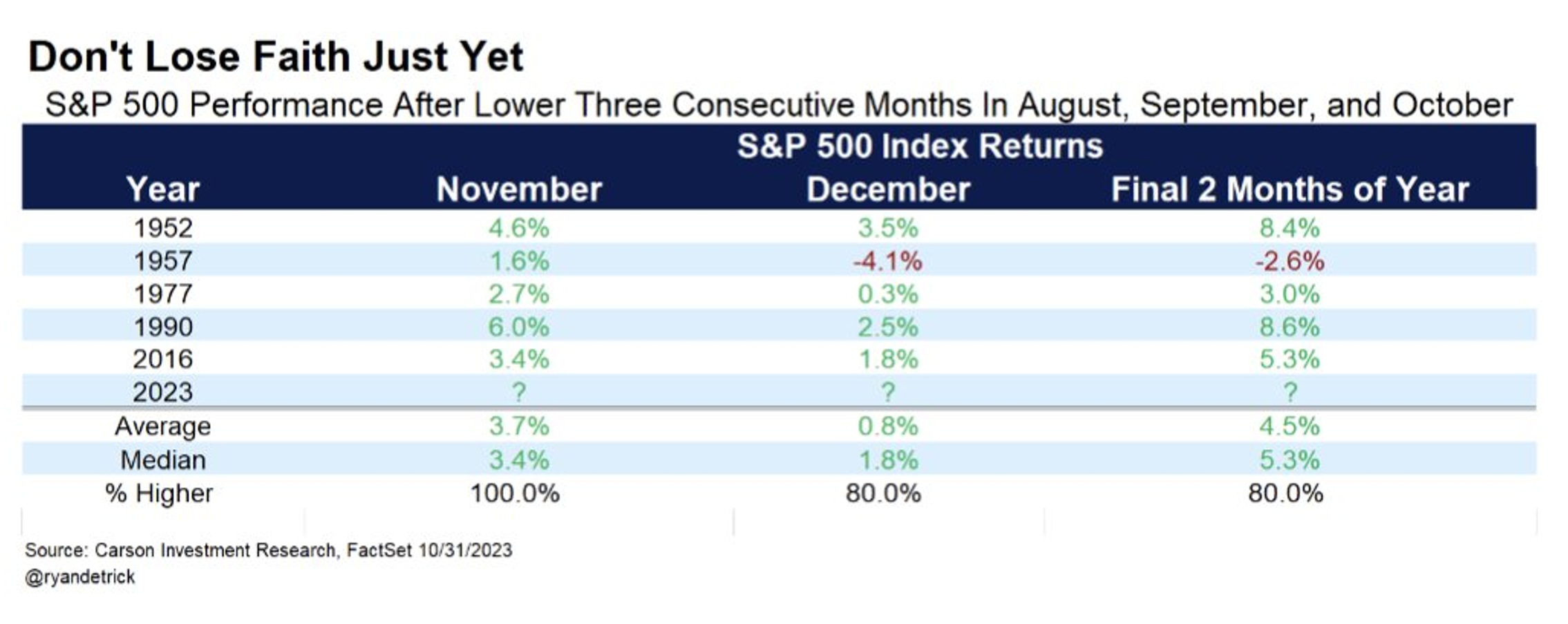

Lastly, we saw this chart earlier in the week and thought it was worth sharing. Markets were down in Aug, Sept, and Oct … that has only happened 5 times since 1952. Pretty rare, but the good news is November has been higher all 5 times. December does fairly well also.

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.