A GDP Report Full of Tricks & Treats

DHL Wealth Advisory - Oct 27, 2023

Markets remained on edge this week as investors monitor the situation in the Middle East and the rapid rise in government bond yields. Virtually ignoring over 500 bps of policy rate hikes...

Markets remained on edge this week as investors monitor the situation in the Middle East and the rapid rise in government bond yields. Virtually ignoring over 500 bps of policy rate hikes in the past 19 months, the U.S. economy accelerated at its fastest pace in nearly two years in Q3. On Wednesday we had the release of Real US GDP which soared to a 4.9% annualized rate, modestly above the consensus view. This marked a major pickup from the 2.1% pace in Q2 and growth of 2.9% in the past year--the latter is the most since the Fed began tightening in 2022/Q1.

Clearly the U.S. economy has defied calls for recession this year, maintaining an above-trend growth rate for the first three quarters of the year. The stronger-than-expected growth puts upward pressure on Treasury yields as yields partly reflect the growth prospects of the economy over time.

The stellar performance reflected an acceleration in consumer spending to a 4.0% clip, with broad gains across goods and services, with even discretionary items like recreational goods and vehicles showing strength. While a 1% decline in real disposable income didn't help (after two big quarterly gains), personal spending was supported by a dip in the saving rate (to 3.8% from 5.2%; though some studies suggest most low- and middle-income households now have exhausted their stockpile of excess pandemic savings). The mid-year bounce in consumer confidence due to rallying equity markets and steadier gasoline prices likely contributed to the spending surge, though the recent pullback in share prices, alongside resumed student loan payments, could weigh in Q4.

Source: BMO Economics EconoFACTS: U.S. GDP (2023 Q3 Advance)

This is one of those rare environments where good economic news is a negative readthrough for equity markets. Investors and Fed Officials want to see a slowing economy as evidence the high interest rate environment is doing its job to slow growth and, by extension, slow inflation. Well, don’t expect the big Q3 GDP number to roll into Q4. Economists expect growth to downshift sharply in Q4, weighed down by the lagged response of past rate hikes, some rewind in inventories, dwindling excess savings, student loan repayments, the autoworkers' strike (though there is progress on this front with Ford's tentative deal with the UAW), and the risk of a government shutdown in mid-November.

That’s not to say we’re bearish on the macro outlook, but we do expect, and want, the torrid pace of economic growth to normalize. Some special factors have juiced the U.S. economy this summer, including a surge in defense spending and equity market rally. These special forces will moderate in Q4, which should temper economic growth and allow Fed officials to continue their more dovish tone that’s been the mantra in the last few meetings.

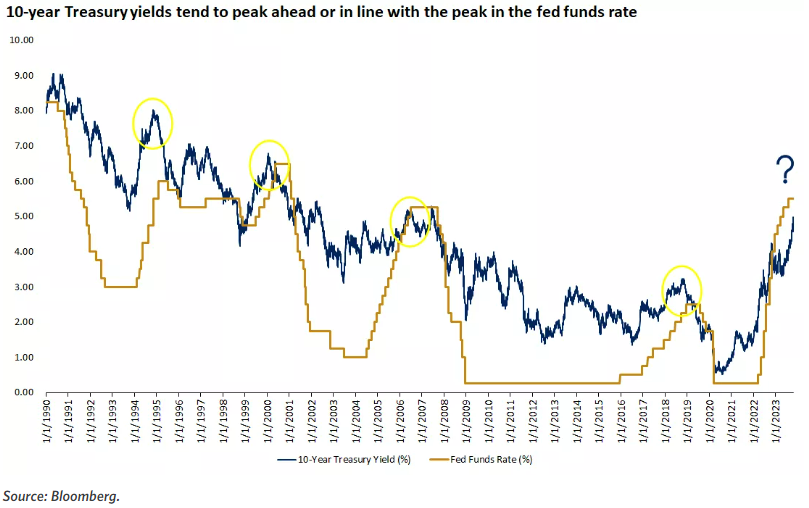

Circling back to the US Treasury market and yields, it’s worth noting that from 1990 through 2019 (pre-pandemic), the average 10-year Treasury yield was around 4.5%, and the average Canadian 10-year government bond yield was around 4.75%, so the current range of 4% - 5% is only somewhat above long-term averages.

Historically, the 10-year yield can be viewed as a proxy of real GDP growth plus inflation over time. If, for example, we believe the real U.S. GDP growth rate will average 1.5% to 2% and core inflation will settle to around 2% to 2.5%, then the range of the 10-year yield should be around 3.5% to 4.5% long term. However, we do believe that over time, 10-year yields will consolidate and eventually peak. This may happen as the Fed, BoC, and central banks around the globe pause their rate-hiking cycles and over time move rates lower, putting some downward pressure on 10-year yields. In fact, historically, 10-year Treasury yields tended to peak ahead of or in line with the peak in the fed funds rate. If we expect the Fed is nearly done raising rates, then yields may be closer to peak levels, as well.

While we do see some relief over time in the 10-year yield, keep in mind that bond yields will not likely return to the lows of the post-2008 era. After the 2008 financial crisis, for example, the fed funds rate spent years at zero, while the 10-year Treasury yield hovered in the 1.5%–2.5% range. As rates normalize in this cycle, we would expect the fed funds rate to be positive and 10-year yields to settle in a higher range, perhaps 3.5%–4.5%.

Meanwhile, the Bank of Canada kept its key overnight lending rate unchanged this week at 5.0% as widely expected, the second consecutive meeting on hold. Whether this translates into a more extended pause or not will depend critically on whether the economy has cooled enough to bring underlying inflation even lower in the coming months. Judging by the Bank's tone, they remain unconvinced. While pointing to the many signs of cooler demand and some relief on price pressures, the final paragraph of the Statement notes in conclusion that "inflation risks have increased". Not wanting to repeat the misfire earlier this year, the Bank then flatly states that it "is prepared to raise the policy rate further if needed." Zero ambiguity around the bias there.

Source: BMO Economics EconoFACTS: BoC Policy Announcement and Monetary Policy Report

The Bank also released its quarterly Monetary Policy Report (MPR), replete with a fresh set of economic forecasts. The main point there is that the GDP growth estimates for this year and next have been carved down to size, partly due to downward revisions to earlier quarters, but also because of the dampening impact of the rapidly rising rate environment. They are now mostly in sync with strategists, albeit a tad higher for this quarter and next, looking for roughly 1% GDP growth on average for this year and next, before a return to 2.5% in 2025. Unfortunately, the inflation forecast has traveled in the opposite direction (mostly, but not entirely, due to energy prices), with the Bank now expecting inflation to average 3.0% next year, a meaty half-point higher than the July call and even above-consensus view.

Source: BMO Economics EconoFACTS: BoC Policy Announcement and Monetary Policy Report

Bottom Line: We have long believed that 5% rates are plenty high enough to eventually quell underlying inflation, but it will take time and patience. Strong wage growth and firm core inflation trends are going to test the Bank's patience. However, all signs suggest that the economy is struggling mightily to grow—despite the artificial sweetener of a surging population—with Q3 GDP about flat, housing halting, consumer confidence crumbling, and the Business Outlook Survey pointing south. Still, price and wage growth remain too fast for the BoC to back off its hawkish rhetoric just yet. To act on that hawk talk would take either a big rebound in growth, a renewed acceleration in inflation, or perhaps a considerably weaker Canadian dollar. We assume none of those forces will weigh in, and look for the Bank to remain on hold for the first few quarters of 2024.

Source: BMO Economics EconoFACTS: BoC Policy Announcement and Monetary Policy Report

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.