Paraskevidekatriaphobia or not. Its still Friday

DHL Wealth Advisory - Oct 13, 2023

It was a full week of headlines as markets digested the escalating violence in Israel, concern in China’s property markets, and slightly hotter than expected inflation. Despite the volatility, major indices close off back-to-back weekly gains...

It was a full week of headlines as markets digested the escalating violence in Israel, concern in China’s property markets, and slightly hotter than expected inflation. Despite the volatility, major indices close slightly up for the week showcasing the resilience of the global economy. Of course, these reactions are not top of mind after the past week’s human tragedy which continues to unfold. Our thoughts are with those impacted and we stand with the global community in mourning the loss of innocent lives.

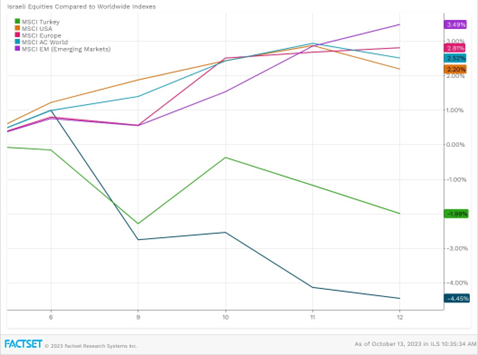

Monday saw oil prices surge as fears of the violence spilling over in the Middle East panicked investors. Crude jumped roughly 5% but has since retreated as energy experts describe the spike as a “knee-jerk reaction”. Neither Israel nor the Gaza Strip host major oil and gas infrastructure and any significant impact to global demand would stem from an escalation into the wider Gulf region and most notably Iran. Despite turbulent historical relations, Israel’s other neighbors offer declining support for the Palestinian cause. On the off chance there is any sort of expansion, it is still unlikely that pump prices will increase dramatically in the near term given the current seasonal shift that has cut demand. Amidst this uncertainty, oil is back in the USA as U.S. crude production hit its highest level ever in the past week bringing output full circle since the prevailing COVID levels in early 2020. If the oil supply chain was choked off, the U.S. would have the capacity to lean on domestic production through the winter. After the initial shocks to global equities it appears that most worldwide indexes are unaffected while Israeli equities have fallen due to war worries.

On the inflation front, September CPI on a month-to-month basis showed significant price easing in several items including energy and gasoline, down from 5.6% to 1.5% and 10.6% to 2.1% respectively.

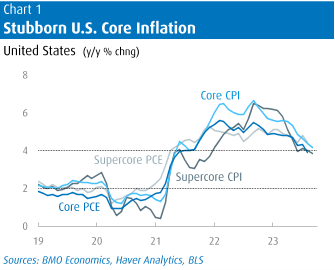

Without getting drawn too far into the weeds, the main takeaway from the CPI was that both headline and core seem to be settling into a 4% zone, or double the target (Chart 1). And this persistent underlying inflation issue has moved far beyond the supply chain pressures of days of yore (2021/22). In fact, core goods prices were unchanged from a year ago, matching the pre-COVID norm of no goods inflation. Instead, it’s all about services now, with these prices rising 5.7% y/y, and picking back up on the three-month annualized trend to 5.4%.

Source: BMO Economics Talking Points: Risks On

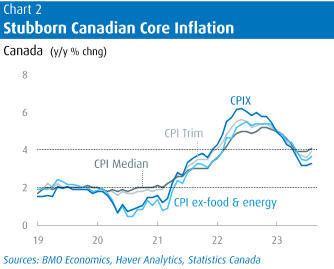

It’s a broadly similar story for Canadian inflation (Chart 2). We look for next Tuesday’s CPI release to post another headline increase just north of 4%, and most core measures to be hovering near that mark as well. (The main reason that Canada’s headline inflation is above core trends, whereas it’s the opposite in the U.S., is the weak loonie is pressuring both food and energy prices.) This report is the last major data release before the Bank of Canada’s next rate decision (Oct. 25), and will thus hold some serious sway. Market pricing points to a meaningful chance that the Bank could hike at that meeting, albeit less than 50-50, and rising in the out meetings.

Source: BMO Economics Talking Points: Risks On

Along with CPI data, we received the minutes from the September 20th FOMC Meeting which showed growing sensitivity from the Committee to the risks of their current restrictive monetary policy stance and echoed a much more dovish tone than what was expected. Notably, the probability of another Fed rate hike at the November FOMC meeting plunged to just 9.8% in the Fed funds futures market, following the release of the Minutes, with the probability of a December hike at around 19.9%. This is in-line with our forecast for no more rate hikes from the Fed, but a higher-for-longer hold in 2024.

Source: BMO Economics EconoFACTS: FOMC Minutes (September 19-20)

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.