Happy Thanksgiving!

DHL Wealth Advisory - Oct 06, 2023

The S&P 500 ended a streak of four negative weeks despite global markets undergoing another week of volatile trading as the recent surge in interest rates has been the dominant driver across financial markets of late...

The S&P 500 ended a streak of four negative weeks despite global markets undergoing another week of volatile trading as the recent surge in interest rates has been the dominant driver across financial markets of late. This has been prompted primarily by a recalibration of expectations for upcoming U.S. Fed policy, with market sentiment getting caught up by Fed commentary suggesting monetary-policy settings will remain restrictive for longer than investors previously anticipated.

It's been our view that the US Fed would err on the side of caution when it comes to dropping interest rates to account for slowing inflation. We're not surprised by the rhetoric that the policy rate may stay higher for longer. After all, inflation is somewhat a self-fulfilling prophecy: As consumers spend more now in anticipation of something costing more in the future, the velocity of money increases, further boosting inflation and contributing to inflationary psychology. So for officials, talking tough is just as important as acting tough. However, we're also not convinced the Fed will have to do much more tightening at this stage. Instead, it's time, not further rate hikes, that is needed to see inflation moderate back toward the target. In other words, it may be more bark than bite from here. In any event, that bark has sent rates higher and stocks lower, a reaction that we think may be creating an opportunity. Why?

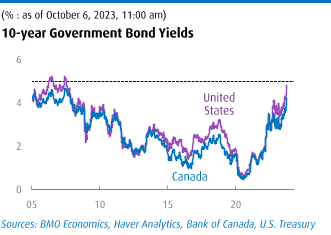

Peak rates would provide a catalyst for stocks to rally, and the 10-year U.S. Treasury yield jumped above 4.89% at one point last week, its highest since 2007. Interestingly, Friday saw a massive beat on the US Jobs report for the month of September. The data could easily have forced rates to break through recent highs, but we actually saw a big mid-day reversal and resistance against new highs. Beyond the crackling headline gain of 336,000—double expectations—net upward revisions added 119,000 which, together, lifted payrolls 2.1% above year-ago levels. It wasn’t a full flush of strength: the companion household survey reported a modest 89,000 job gain, keeping the unemployment rate steady at 3.8%. Moreover, wages were a tad cooler than expected, up a modest 0.2% m/m, and clipping the annual rate a tick to 4.2%. Aside from a brief dive in 2021, that’s the calmest since pre-pandemic days and a marked moderation from last year’s apex of 5.9%.

Source: BMO Economics Talking Points: Ride of the Vigilantes

Canada also saw jobs double expectations last month with a 63,800 advance, which was only enough to keep the unemployment rate steady at 5.5% amid soaring population trends. The near-universal view was that the headline flattered the strength of the economy, as all the gains were in volatile education (“Wait, what? They hire teachers in September?”), and most were in part-time jobs.

Source: BMO Economics Talking Points: Ride of the Vigilantes

Where does this brutal bond market and solid employment gains leave the central banks? Notably, even amid the spike in long-term yields, two-years were little changed on the week, with a slight rise in the U.S. and a dip in Canada. The reality is that the fierce back-up in longer rates is doing a lot of the tightening work for policymakers, reducing the need for further hikes. This week, that was mostly offset by solid data. Thus, in terms of odds of additional hikes, what the job markets giveth, the bond carnage taketh away. We are still clinging to the view that the Fed and Bank of Canada have done enough and that, with patience, the forceful tightening of the past 18 months will subdue underlying inflation.

Source: BMO Economics Talking Points: Ride of the Vigilantes

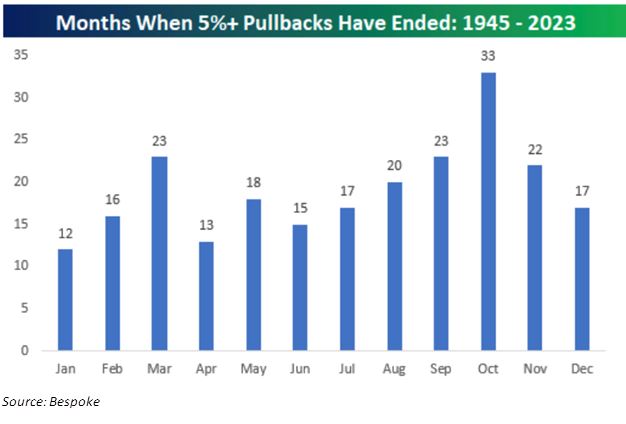

October is such a misunderstood month. Sure, it can be temperamental and has had its issues for stocks over the years—see 1987, okay and 1929, well, and 2008, and 1978, all right and many others—but it really isn’t such a bad month. In fact, since that slight mishap in 2008, the S&P 500 has risen on average by 2.4% in the 14 Octobers since. And, while it saw the single worst month in the post-war era (1987, down 21.7%), it also had the single best such month (1974, up 16.4%). Since 1990, we count eight separate bear markets in the S&P 500, or very near-bears (there were no less than four peak-to-trough declines of between 19%-to-20%). Of those eight tough markets, five of them hit bottom in the first half of October—in 1990, 1998, 2002, 2011, and 2022. So, contrary to its sullied reputation, October has in fact often been the month of salvation for stocks. Too bad we can’t say the same thing here in Mudville for the Blue Jays.

Source: BMO Economics Talking Points: Ride of the Vigilantes

And here’s our imperial evidence to support this argument. The below chart illustrates the number of times since 1945 that a 5%+ S&P pullback has ended by month: Jan: 12 Feb: 16 Mar: 23 Apr: 13 May: 18 Jun: 15 Jul: 17 Aug: 20 Sep: 23 Oct: 33 Nov: 22 Dec: 17.

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.