Fed Up

DHL Wealth Advisory - Sep 29, 2023

Good riddance September. Markets closed out the month and third-quarter on a mixed note Friday, in what was the weakest month of 2023. September saw the S&P500 shed ~4.5% as resilient economic data strengthened yields and acted as a headwind...

Good riddance September. Markets closed out the month and third-quarter on a mixed note Friday, in what was the weakest month of 2023. September saw the S&P500 shed ~4.5% as resilient economic data strengthened yields and acted as a headwind to equites. Seasonality was also at play with September living up to its historical reputation as being the weakest month for the market.

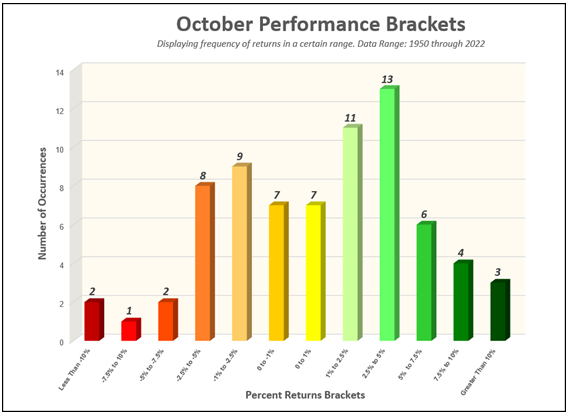

If readers were curious, October has historically been a much friendly month for market participants. Purely from a data point of view, the histogram below is a visual that helps illustrate October's past behavior. It categorizes each October's return into a performance bracket, allowing us not only to see that there have been more up Octobers than down Octobers, but also the degree to which they have been up or down. If we look at the extremes, notice that only five Octobers since 1950 (including 2018) have experienced a decline worse than -5%. The most common experience in October has been a gain in the range of 2.5% - 5%.

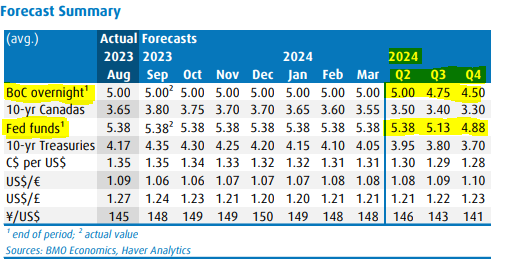

As we get closer-and-closer to confirmation of peak rates, we suspect that over the next few weeks, and probably into year-end, both the Fed and Bank of Canada will continue to communicate that its job on inflation is not done, and keeping the additional rate hike on the table was a good way for the Fed to do this. Since last week's meeting, markets now expect the Fed to remain largely on hold, although the probability of a December hike has increased, slightly. The first rate cut is also now expected in July 2024, pushed out from the June rate cut priced in before the meeting. This is something that is echoed out of the BMO Economics team. For added colour, below is their Forecast Summary for CDN and US Funds rates.

In our view, for the both the Fed and BoC, the next move may depend more on the trajectory of the economy. If the consumer or broader economy does weaken, the central banks may decide to cut rates sooner or deeper than expected next year. If growth holds up and inflation continues to gradually ease, then we think the market's current view is credible, and over time the Fed and BoC will steadily normalize rates down toward a neutral level.

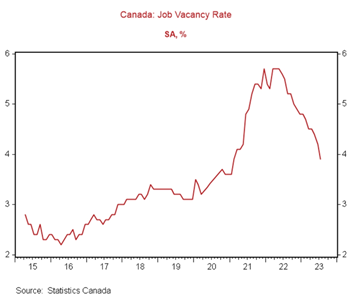

While both the U.S. and Canadian economies have held up thus far, we see early signs of some easing in both consumption and the labor market. As the summer travel season comes to an end, the consumer is facing an extended period of higher rates and tighter borrowing standards, oil prices are elevated, and excess savings post-pandemic have been largely drawn down. And although the job market remains solid, some early warning signs, like fewer job openings and lower quits rates, have emerged as well. Take for instance the Canadian Payrolls report for July. Job vacancies are sliding way down the other wide of the mountain.

Meanwhile, on Friday, we had data that showed the Canadian economy rebounded slightly last month but still saw little growth, backing a case for the central bank to keep rates on hold despite inflation remaining elevated. Preliminary data suggest gross domestic product edged up 0.1 per cent in August, Statistics Canada reported Friday, as declines in the retail and oil and gas industries partly offset increases in the wholesale and finance sectors.

The economy is now on track to expand at a 0.2 per cent annualized rate in the third quarter, if September output is flat. That’s weaker than the 0.4 per cent consensus estimate. Although that means Canada could escape a technical recession with this rebound after a second-quarter contraction, the pace of growth is far weaker than the 2.6 per cent seen during the first three months of this year.

The bottom line here is that there is more evidence that Canada’s job market and economy are softening, albeit from extreme levels. It’s still premature for this to feed into wages and, therefore, inflation, so the Bank of Canada will remain on high alert. But, it does suggest that the Bank might be able to keep leaning on the economy and inflation with rates at current levels.

In our view, while the central banks may continue to signal that they are not done raising rates, there may be a confluence of factors that keep them on the sidelines. Inflation, and especially core inflation, continues to gradually move lower; the labor market has shown early signs of cooling; and the consumer, which has been the backbone of the economy, has been drawing down their excess savings. While market volatility may remain elevated in the near term, we would expect any pullbacks to be in line with normal corrections. Long-term investors can consider using volatility as an opportunity to add to or diversify portfolios.

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.