Somebody Tell Yields That It's Fall

DHL Wealth Advisory - Sep 22, 2023

While a solid labour market and a resilient economy continue to be sticking points, the commentary we saw on Wednesday, does not guarantee further hiking but rather reiterate the Fed’s approach to waiting and assessing the data...

Ah, September. Crisp nights, cool weather, pennant races, NFL football, and rocky equity markets. Fully living up to its reputation as the most challenging page on the calendar, this month has already seen a roughly 4% pullback in the S&P 500 as of Thursday, putting it on track to be the worst month since… last September, when it fell 9.3%. (Technically, Dec/22 saw a 5.9% drop, but let’s not fuss with a good story.)

Source: BMO Economics Talking Points: It’s Fall, Except for Yields

There is no mystery whatsoever behind the latest market angst—bond yields ratcheted higher again this week, despite the Federal Reserve keeping the fed funds target range unchanged at 5.25%-to-5.50% on Wednesday, marking the second hawkish pause of the year. While the pause was expected, markets reacted negatively to the FOMC statement and accompanying summary of economic projections which underscored the higher for longer commentary. The fresh projections showed 12 of 19 policymakers favouriting one more rate hike this year amid a resilient economy, a healthy labour market and stubborn inflation. “We’re in a position to proceed carefully at this point,” Fed Chair Jerome Powell said in a news conference after the rate announcement. “A year ago, we proceeded pretty quickly to get rates up. Now we’re fairly close, we think, to where we need to get. It’s just a question of reaching the right stance.”

Source: Early edition (September 21, 2023)

It is important to note that the market reaction is primarily based on projections and expectations going into 2024. While a solid labour market and a resilient economy continue to be sticking points, the commentary we saw on Wednesday, does not guarantee further hiking but rather reiterate the Fed’s approach to waiting and assessing the data. Forward guidance was largely repeated from the prior two meetings, using phrases that offer the Fed the flexibility to accommodate either policy choice a few months from now.

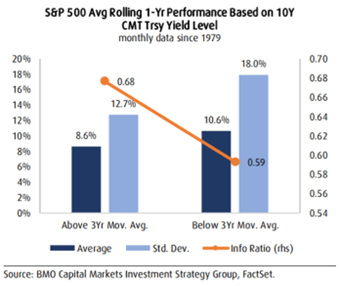

Interest rates will remain a prevalent topic as the 10-year Treasury yield lingers around its highest level in almost 15 years as more investors are accepting the higher for longer story. Once more, this marks a substantial shift from previous decades, when rates had been on a relatively steady downward trend since the early 1980s. While this can be unsettling for some investors, historical market performance shows that higher rates do not always cause stock prices to decline. Instead, as contrasted to lower interest rate levels, we have seen that returns tend to be just slightly below average and surprisingly, less volatile. The S&P 500 average gain during higher interest rate periods is 8.2% vs. 10.6% for lower interest rate periods; However, the standard deviation of those returns is much lower at 12.7% vs. 18% providing a higher average information ratio

Source: Early edition (September 21, 2023)

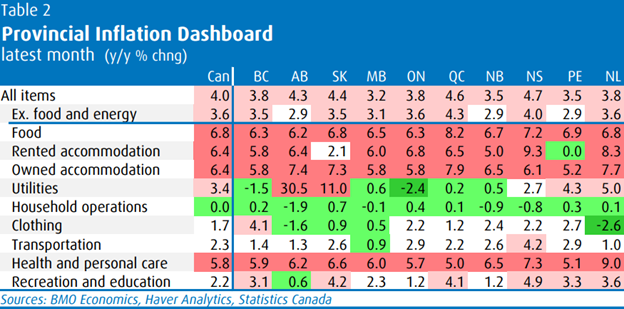

Moving back across the border, inflation remains a lingering challenge from coast to coast and, while the degrees have varied slightly, all provinces have faced a significant inflation shock. Inflation remains well above the Bank of Canada’s 2% target across all provinces. All provinces are seeing inflation rates in excess of 3% y/y as of August, four are north of 4% y/y, and core inflation trends are similarly sticky. Cost-of-living pressures are highlighted by strong inflation rates in food and housing. Nowhere in Canada is food inflation lower than 6% y/y, with a weak loonie, high transportation costs and firm wage pressure acting similarly across provinces. While resale real estate prices corrected, rents continue to run at a strong pace. Some areas where the population boom has been more acute—such as Ontario and Atlantic Canada—are seeing stronger gains, but nowhere in Canada is there much relief. The better news is that goods price inflation has cooled, for the most part, across the country. Inflation in clothing, household operations and recreation/education is running below the Bank of Canada’s target in most jurisdictions.

Source: BMO Economics Provincial Monitor: Leaning Into the Headwind

The summary of the Bank of Canada’s deliberations from the September 6th meeting reiterated a hawkish bias. Recall that meeting saw the Bank pause after two consecutive 25 rate hikes, leaving the policy rate at 5%, or the highest since March 2001. The Bank of Canada is trying to thread the needle between decelerating economic activity, the impact of past rate hikes still working through the economy, but stubbornly persistent above-target core inflation. Rates either aren't high enough yet; or they are high enough but haven't been so for long enough. It's telling that, at this meeting, the Bank "did not want to raise expectations of a near-term reduction in interest rates, given that they only considered keeping the policy rate where it is or raising it further." The bias remains to tighten further if wages and inflation don't cooperate.

Source: BMO Economics EconoFACTS: BoC Summary of Deliberations (September 6)

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.