Goodbye Summer; Hello Pumpkin Spice, Everything...

DHL Wealth Advisory - Sep 01, 2023

Global equities closed out the month of August on a high note despite the S&P 500 and NASDAQ suffering their first monthly decline since February. As we spoke in last week’s edition...

Global equities closed out the month of August on a high note despite the S&P 500 and NASDAQ suffering their first monthly decline since February. As we spoke in last week’s edition, strength in US Treasuries and general seasonal weakness were mostly to blame for negative returns. That said, the last two weeks of the month saw treasuries pull-back and the market re-accelerate.

We are starting to hear talk in the media lately about how September is traditionally the weakest month of the year for stocks and strictly speaking that's absolutely true. Over the past few decades the average return for the S&P/TSX Composite in September is -1.57%, and -0.66% for the S&P 500. However, BMO’s technical team believes this year has the potential to be different since all of the gauges in their short-term timing model have given a combined set of new buy signals for the first time since March.

Source: BMO Daily Action Report - 09-01-23

We generally shy away from highlighting these types of reports as they encourage short-term trading and emotional behaviour vs the proven fundamental philosophy of buy good companies and let that value accrue. However, this technical team has been spot on thus far in 2023 and their call for the market to potentially break-out in the coming quarters leads us to break our rule just this one time.

The team says that in terms of the current price action, all of the major averages have recently broken above their 50-day moving averages which clears the way for the rally to extend back to their July peaks. (TSX: 20,677, SPX: 4607, Nasdaq: 14,446) Breakouts there would likely result in the S&P 500 and Nasdaq Composite challenging their all-time highs at some point in late Q3 or early Q4. (SPX: 4818, Nasdaq: 16,212). Here in Canada the main number you really have to pay attention to is the upper end of the ten month trading range at 20,843. A breakout there would signal a resumption of the long-term uptrend and clear the way for it to challenge its all-time high at 22,213.

Source: BMO Daily Action Report - 09-01-23

Their favorite sectors include Industrials, Information Technology, and Consumer Discretionary, where each of these indexes have recently reversed back to the upside from successful tests of their rising 200‐day moving averages. Within our discretionary mandates we have been adding to these sectors in the past few months. If readers would like a copy of the technical report, please don’t hesitate to reach out. The team does a deep dive on their favorite names for new money in the Consumer Discretionary sector.

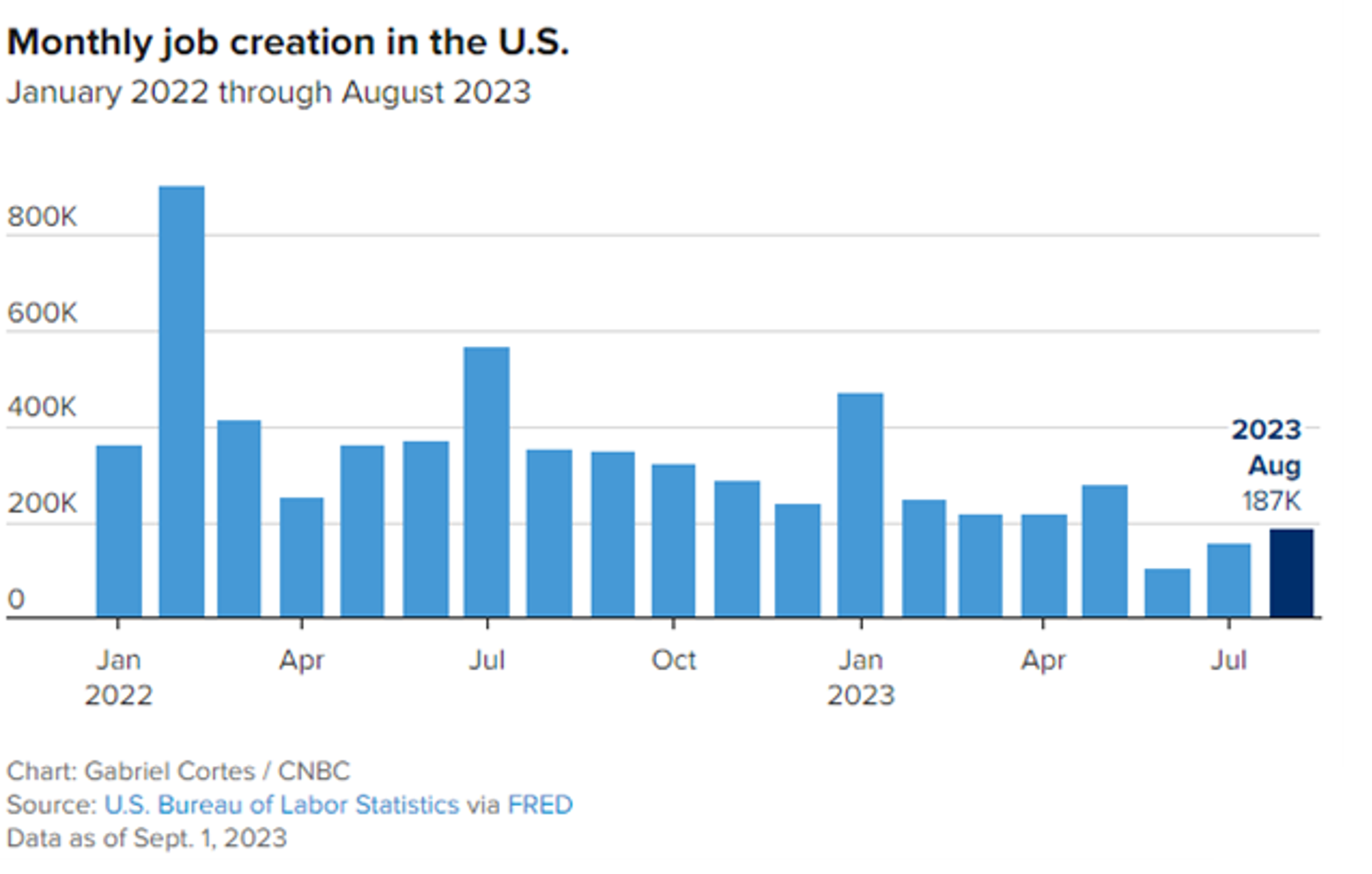

Turning back to our bread and butter: Fundamentals. Economic and corporate data continues to suggest the “soft landing” narrative is alive and well. On Friday we had US jobs data that shows the US Labour market is holding steady despite interest rates sitting at 22-year highs. August saw the US Nonfarm payrolls increase by 187,000, ahead of the estimate for 170,000. However, the counts for June and July were revised considerably lower with the July estimate moved down by 30,000 to 157,000. June was revised lower by 80,000 to 105,000, making that the smallest monthly gain since December 2020.

Source: BMO Economics EconoFACTS: U.S. Nonfarm Payrolls (August)—187k = 205k

Even at the beginning of this year, employers were adding as many as 517,000 jobs a month, as seen in February. But over the last few months, the number of new jobs has started to slow. Other recent data has pointed to easing in the labor market, including BLS’s Job Openings and Labor Turnover Survey (Jolts), which showed there were 8.8m job openings in July, 338,000 fewer than in June. There were 1.5 job openings for every unemployed worker, according to the survey, the lowest rate since September 2021.

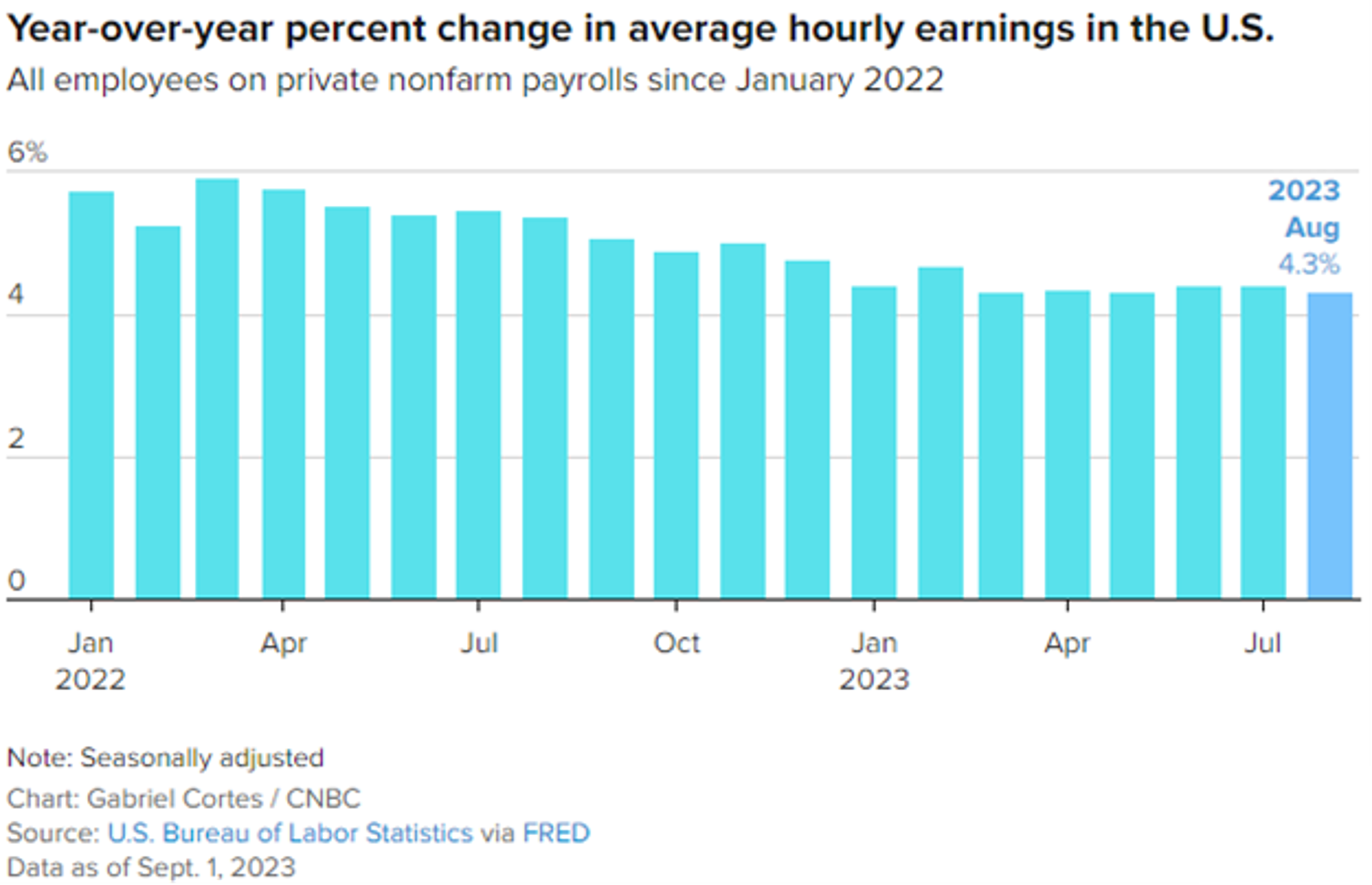

Meanwhile the unemployment rate ticked up sharply from 3.5% to 3.8%. That reading is the highest unemployment rate since February 2022, but looking under the hood the rise was due to a big increase in the labour force participation rate (new entrants entering the jobs market that hadn’t been looking for work). The rolls of the unemployed grew by 514,000, while the household count of those employed increased by 222,000. An increase in the labour force and a slowing of job gains is a welcome signed for officials as it helps to offset pressure in wage inflation. Average hourly earnings increased 0.2% for the month and 4.3% from a year ago. Both were below respective forecasts of 0.3% and 4.4% and another possible sign that inflation pressures are easing.

Meanwhile Canadian Gross Domestic Product data on Friday showed a notable slowdown in the economy in Q2. After a fast start to 2023, as a series of challenging events through the spring and early summer weighed heavily on activity. Real GDP surprisingly dipped at a modest 0.2% annual rate in Q2 (consensus was looking for a 1.2% rise), down from +2.6% in Q1 (revised lower from 3.1%). And, the latest monthly results suggest activity will remain sluggish in Q3—June GDP fell 0.2% (as foreshadowed by the flash estimate), while the July flash is for a flat reading. For reference, the Bank of Canada had penciled in 1.5% growth for both Q2 and Q3 in its July forecasts, so activity is coming in far on the low side of official expectations. The small pullback in Q2 GDP lines up well with the recent rise in the unemployment rate, and reinforces the point that growth is cooling markedly, even when looking through the many special factors in recent months.

Source: BMO Economics EconoFACTS: Canadian Real GDP (Q2 & June/July)

We are sticking to our view that Canada will experience a mild contraction, and today's surprisingly soft Q2 obviously makes that outcome much more likely. The broad softening in the domestic economy will almost certainly move the Bank of Canada to the sidelines at next week's rate decision after back-to-back hikes. Between the half-point rise in the unemployment rate, the marked slowing in GDP, and some cooling in core inflation, it now looks like rate hikes are over and done. Now, the Bank of Canada just has to be patient as they wait for inflation to come their way…

Source: BMO Economics EconoFACTS: Canadian Real GDP (Q2 & June/July)

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.