Hawks, Doves, and a lot of Parrots

DHL Wealth Advisory - Aug 11, 2023

After a lackluster start to the month of August, spurred by the U.S. debt rating downgrade and mixed data in the July jobs report, markets rebounded slightly this week...

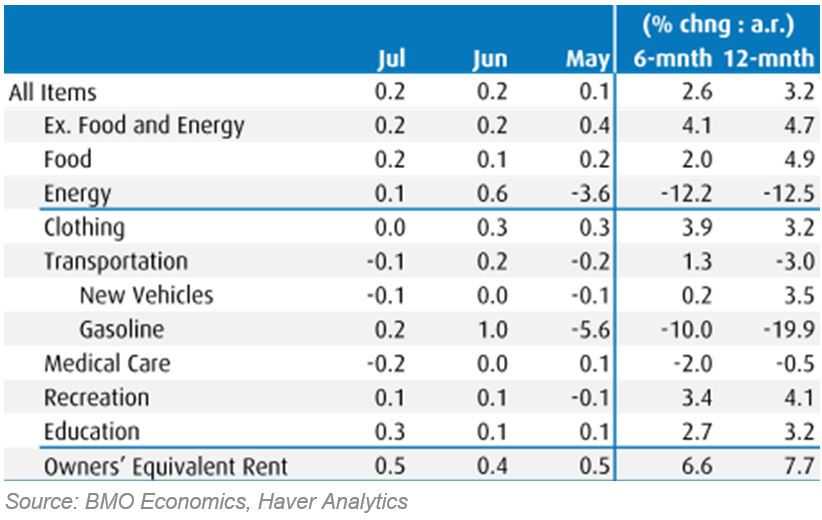

After a lackluster start to the month of August, spurred by the U.S. debt rating downgrade and mixed data in the July jobs report, markets rebounded slightly this week. On Thursday, data showed continued cooling on U.S. inflation for the month of July, bolstering expectations of a soft landing. For a second straight month consumer prices rose 0.2%, marking a three-month annualized increase of just 1.9% - the slowest pace since June of 2020. Food and Gasoline prices rose by similar amounts for the month, followed to the upside by automobile repairing and insuring (up 1.0% m/m, 12.7% y/y), and a second straight monthly rise to shelter costs (up 0.4% m/m) despite moderating rent growth. These increases were predominately offset by a large drop in airfares (down 8.1% m/m), used vehicle prices (down 5.6% y/y), a small drop in new vehicle prices, and another dip in medical services costs.

Source: BMO Economics EconoFACTS: U.S. Consumer Price Index (July)

Core CPI, which excludes volatile food and energy costs, saw a similar increase of 0.16% for the second straight month, bringing the yearly core rate to 4.7%. While still elevated, inflation has slowed every month since a 6.6% peak in September.

Source: BMO Economics EconoFACTS: U.S. Consumer Price Index (July)

While two months of softened inflation numbers indicate progress in the Fed’s fight for price stability and good news for a hawkish market, it does not necessarily define a trend. Looking past this report, Jerome Powell’s Jackson Hole speech later this month combined with further data should help set expectations into the end of the year. With the next Fed policy meeting set for September the consensus is calling for a pause, something we see possible if the current trends continue into the August CPI data which is set to come out the week before the meeting.

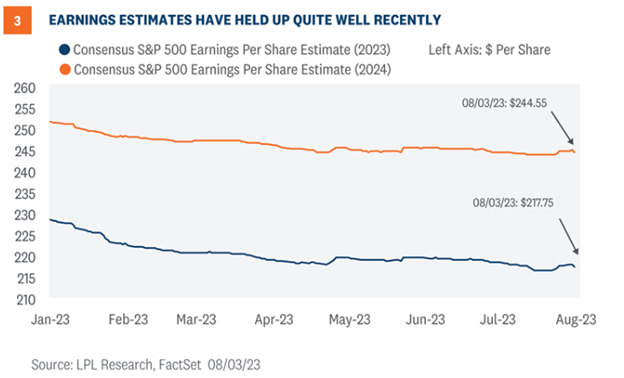

Moving over to earnings, with this season mostly behind us, roughly 80% of S&P 500 companies that have reported beat consensus estimates. While earnings results in Q2 have been better than expected, earnings beats have been extremely flattish one day post-earnings compared to historical data. While some of the larger players (AMZN, META, and GOOG/L) saw their shares rally on results, the overall beats were not as rewarded as they were in years prior. A key reason is that while EPS beats have been strong, revenue beats have been lower than normal, suggesting company performance has stemmed from cost cutting rather then thriving off a strong economy. With the Fed continuing to raise rates, this result was expected but it is still worth applauding the efficiency and effectiveness of corporate America’s cost controls to maintain profitability during this period.

An important takeaway from this earnings cycle is the stabilization of forward guidance. There is not much talk of recession risk from companies as banking stresses have calmed, the jobs market is healthy, and the economy has momentum. Since April, the S&P 500 EPS estimate has held steady, and relatively upbeat guidance has increased potential earnings growth in Q3 and pushed up 2024 Q1 estimates.

We expect to see some volatility over the coming months as the markets will remain sensitive to news and data. However, as analysts and economists continue to align their narratives based on the positive trends we are seeing, markets should respond accordingly.

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.