Don't Throw A Fit-ch

DHL Wealth Advisory - Aug 04, 2023

Global equities took a breather this week as investors digest corporate earnings and more data that continues to show a resilient US economy. Earnings season is more than halfway through with results coming in stronger than expected...

Global equities took a breather this week as investors digest corporate earnings and more data that continues to show a resilient US economy. Earnings season is more than halfway through with results coming in stronger than expected. Of the 79% of S&P 500 companies that have reported, about 82% have posted positive surprises, according to FactSet data.

The consensus amongst economists entering the year was for a recession at some point in 2023. Now, the base case is for a soft landing, or no recession at all. And this has been reflected in markets through a broadening of leadership. Economically sensitive parts of the market, including small-cap stocks and cyclical sectors, have outperformed in recent weeks. However, after a ~17% increase in the S&P 500 and ~6% rise in the Canadian TSX this year, we would caution against drawing a straight line higher for markets in the second half of the year. Many on Wall Street have also noted that the market has been long overdue for a pullback, or slight correction, after hitting rally-mode for the better part of the year.

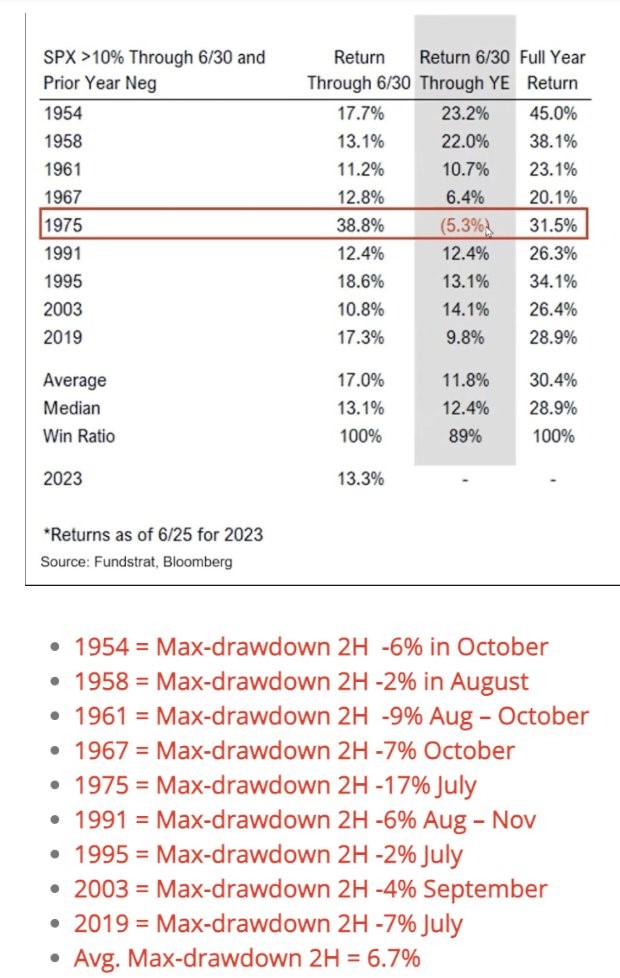

Interestingly, since 1954, there have been 9 occurrences when the S&P 500 is up > 10% through the first half of the year. In nearly ever instance, the second half returns have been strong up +12% on average. However, the average max drawdown in the second half has been -6.7% with most drawdown starting in July, but the second half has typically finished positive — with a Win Ratio is 89% (positive 8 out of 9 times).

Source: Seth Golden @SethCL Twitter

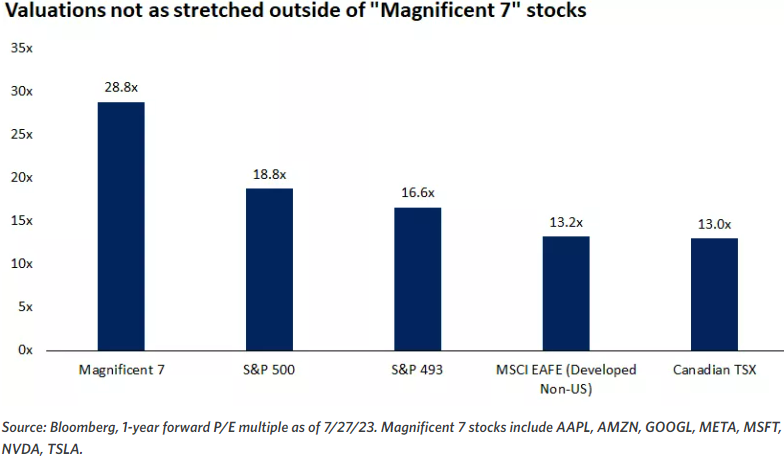

Diving into the specifics, we continue to see market breadth expanding outside of the so-called “Magnificent 7”. These are the seven stocks that have a combined market cap of ~$11 trillion and are responsible for most of the gains the S&P 500 this year ( their combined worth is also triple the size of Germany’s GDP…) They are Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla.

While valuations in the so-called magnificent seven are stretched, the valuation of the rest of the market remains more reasonable. If fact, as the table below illustrates, if we were to strip out these seven stocks from the S&P 500 then the price multiple is 18.8x. For context, the historical average for the market is ~20x. So the broader market still screens as affordable. And if interest rates and yields are indeed flat lining and economic growth continues to remain resilient and improves next year, we should see better performance and perhaps some valuation expansion from the broader market. This is why we would favour not necessarily chasing the magnificent seven, but rather complementing growth stocks with Canadian value in cyclical sectors such as financials, industrials and materials.

Lastly, the decision by the rating agency Fitch to downgrade the U.S. credit rating to AA+ from AAA was met with a mixture of bewilderment (“why now”) and scorn (“totally unjustified”) - and, of course, a rally in the U.S. dollar. Moving past this mini version of the seven stages of grief, the reality is that who can realistically question the decision? Consider the circus act in Washington several weeks ago over the debt ceiling. There’s no question that the standard of government in that country have been steadily deteriorating over the last 20 years (and those are Fitch’s words, not ours!). In financial markets, the move was met with what amounts to a shrug.

Source: BMO Economics AM Charts: August 3, 2023

Whilst the Fitch US downgrade is newsworthy, we don’t think this will have a significant impact from an investment perspective – investors are much more focused right now on inflation (where we are seeing a gradual easing based on recent data) as well as confirmatory signals from the Fed that we are now near the peak of the hiking cycle. With signs that we may be getting closer to a soft landing scenario rather than an outright recession, as well as a fairly upbeat earnings season thus far, we think there are reasons to believe markets can sustain their recent gains. The general consensus among strategists and fund managers has been that the rating cut should have a limited impact on equities, with Wells Fargo & Co. saying any pullback will be “short and shallow” and Liberum Capital describing the news as a “tempest in a teapot.”

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.