Keep Calm and Carry On.

DHL Wealth Advisor - Jul 21, 2023

Global equities continued their unrelenting march higher this week as we had a series of better-than-expected inflation figures out of major Western economies. Price pressures in Britain dropped to the lowest level in 15 months on Wednesday....

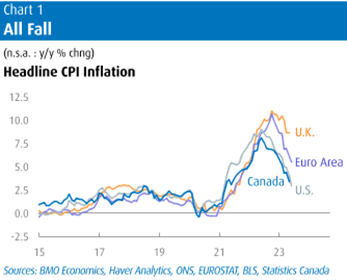

Global equities continued their unrelenting march higher this week as we had a series of better-than-expected inflation figures out of major Western economies. Price pressures in Britain dropped to the lowest level in 15 months on Wednesday: The headline rate of inflation fell from 8.7% in May to 7.9% in June, a bigger drop than the fall to 8.2% that economists had been expecting. Meanwhile on Tuesday we also had Canadian CPI numbers that were a few ticks below consensus.

Canadian consumer prices rose 0.1% and 2.8% y/y in June, 2 basis points better than expected and the slowest yearly pace since March 2021. On a seasonally adjusted basis, CPI also rose 0.1% following May's flat reading, the tamest two-month pace since 2020. Base effects played a role this month as well, as prices were still firm a year ago, helping cut the yearly pace. However, the next couple of months were much tamer in 2022, so it will be more challenging for inflation to slow in the near-term. Nonetheless, the better-than-expected headline result is encouraging as it is a step in the right direction bringing down inflation expectations.

Source: BMO Economics EconoFACTS: Canadian CPI (June)

Investors are now seeing evidence of easing price pressures in the US, UK, Canada and elsewhere which are bolstering hopes that a campaign of monetary tightening is drawing to a close and a soft landing may well be the base scenario.

Even for those of us of the inflationist persuasion for the past 30 months, there can be little debate that the June CPI was good news indeed for the U.S. economy—very good news. For the first time in over two years, most of the top-line figures could be considered “normal”. Whether it was the mild monthly US headline rise of 0.18% and 0.16% on the core, both of which matched the pre-COVID 10-year median, or the yearly overall increase of 3% (less than a third of last June’s grotesque 9.1% peak), most of the results were back in familiar and much more comfortable terrain. One sticking point: while core was tamer than expected, it’s still up 4.8% y/y, and even the three-month trend is still just above 4%, a pace not seen since the early 1990s.

Source: BMO Economics Talking Points: Soft Landing: Mission Possible?

One analyst said that the calm June CPI showed that the “fever had broken” for inflation. We would assert that, in fact, the fever broke last fall when energy prices cooled considerably, and the supply chain normalized. But the question has always been how long the recuperation period would last. And while the latest figures are encouraging, the real battle begins now, as the easy base effects are now behind us. (Note that between last June’s 9% peak and this year’s 3%, inflation has averaged a towering 6% over the past two years, even with energy prices little changed on net over that period.)

Source: BMO Economics Talking Points: Soft Landing: Mission Possible?

As the disinflationary force of lower energy prices fades, that will leave us dealing with the underlying 4% trend in core. Slowing rents will almost certainly help, but to truly crack core will likely require a more significant slowing in the economy. On that front, most of this week’s indicators displayed ongoing resiliency. Small business sentiment perked up to its best level of the year in June, with a normal share reporting they plan to hire or increase capital spending. Initial jobless claims dipped again to below 240,000 and are showing no serious signs of stress after a spring hiccup. The one flash of potential softness was from consumer credit, which saw its smallest increase in nearly three years in May at $7.2 billion (versus a 12-month average of $23.8 bln), potentially signaling that consumers are fading after the wave of rate hikes. However, University of Michigan consumer sentiment bounced in July to a near 2-year high, even as 5-year inflation expectations perked back above 3%.

Source: BMO Economics Talking Points: Soft Landing: Mission Possible?

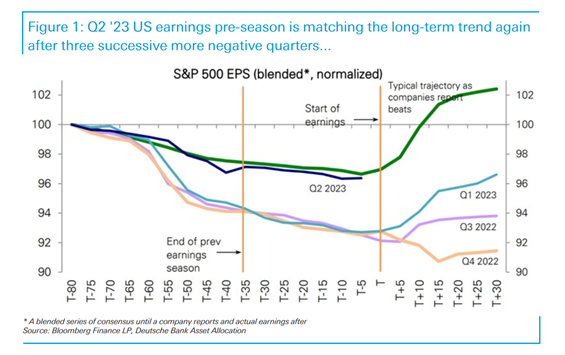

Beyond inflation, the BoC and the Fed, investors' attention will turn to corporate profits, as U.S. banks kicked off the second-quarter earnings season last Friday. Since equity markets bottomed nine months ago, the market rally has been exclusively driven by valuation expansion. But with the benefit of rising valuations likely mostly behind us, earnings will now have to do the heavy lifting to drive gains in the back half of the year. To that point, of the S&P 500 companies that have reported earnings thus far, 74% have exceeded expectations, FactSet data shows. Bolstering optimism for a soft landing for the economy. The good news is that if estimates prove true, the second quarter will mark the worst quarterly earnings decline for this cycle but also the end of the earnings downturn. To this point, S&P 500 earnings are expected to fall before growth turns positive in the third quarter and rebounds further in 2024. Another good omen for markets is that earnings season is beginning to normalize on long-term trend.

Despite that lingering quibble on core, markets have seized on the inflation relief with both hands... Equities kept rolling, with the S&P 500 pushing above 4500 for the first time since March 2022, and now up more than 25% from last October’s nadir. And lest one believes this is just a tech story, the MSCI World Index is also up more than 20% from the lows, and now just 7% below the late-2021 peak. Even the TSX got into the game, rising more than 2% to back above 20,000.

Source: BMO Economics Talking Points: Soft Landing: Mission Possible?

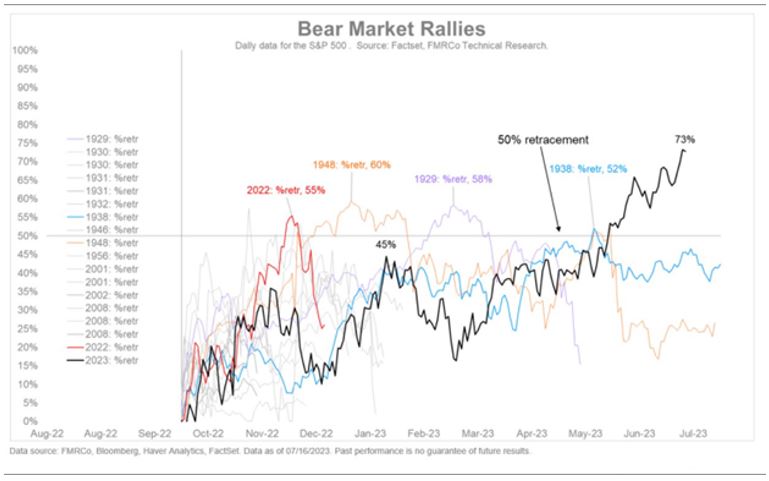

With these gains, the S&P500 has regained nearly three-fourths of the ground it lost last year. Interestingly, bear-market rallies don’t retrace much more than half their preceding decline. When they do, they are usually new bull markets. With our current 73% retracement, history seems to be on the side of the bulls here. We could still be in a long trading range (like the 1940s), but the market has now spent a year and a half—a long time—bucking the long-term uptrend.

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. ("BMO NBI"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO Nesbitt Burns or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. NBI will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.