New Year, Same Market?

Welcome to our first e-Newsletter of 2026! How time flies. We are wishing you and your families a happy, prosperous and healthy new year.

While we didn’t get as much of the seasonal Santa Claus rally last month as we’ve seen in years past, markets have started off 2026 with a fair bit of momentum before pulling back in the last few days. We initially raised some cash at year end, but as of writing, we are almost fully invested and in the Green Zone across all of our longer-term indicators.

Housekeeping Items

Registered retirement savings plan (RRSP)

The RRSP contribution limit for 2026 has increased to $33,810 from $32,490 in 2025. The amount is calculated as 18 percent of your previous year’s income up to the maximum, plus any unused contribution room carried forward.

The RRSP contribution deadline for the 2025 calendar year is March 2nd, 2026. We encourage any clients that want to make contributions to do so as early in the year as possible.

Tax free savings account (TFSA)

As of January 1st, adults in Canada can add another $7,000 in contribution space to their Tax Free Savings Accounts (TFSAs). That’s in line with the $7,000 annual threshold for the past two years, making the cumulative contribution limit for eligible investors who have never contributed to their TFSA since its introduction in 2009 to $109,000.

2026 Market Outlook

As of writing Thursday afternoon, the markets have pulled back slightly after pushing to highs coming out of the Santa Claus rally earlier in the week. A large part of the downside can be attributed to profit taking, especially in financials and precious metals, both of which had been on a tear. We expect that any weakness here to be relatively short-lived.

Many have expressed concerns that US markets, especially in the tech and artificial intelligence space, are in “bubble territory” and that the bull run we’ve seen in the last few years is on its last legs. We believe, however, that the expansion of market participation outside of the “Magnificent Seven” stocks is a healthy indicator that there is still room to grow.

Brent Joyce, BMO’s Chief Investment Strategist, wrote the following back in December regarding hi thoughts on global markets in 2026:

“The bull market is “middle-aged,” not overextended. Risks from overvaluation or policy missteps remain low for 2026. Globally, there is a powerful alignment of stimulative monetary and fiscal policy, combined with solid economic and earnings growth that supports further gains, albeit

at a moderated pace.”

This is in line with our expectations for 2026 as well. We do not expect the significant run-ups like we’ve seen in the last 2 years or so, but high single digit growth for US equities would be reasonable target for the upcoming year, barring any unforeseen circumstances.

As we previously mentioned, the broader market backdrop remains healthy and intact, and participation outside of US big tech is a positive signal for markets. For example, mid-caps are resuming higher in 2026 from their secular uptrend. The most important difference between mid-caps and large-caps shows up immediately in sector exposure, starting with technology. The Mid Cap 400 Index only carries a 16% weighting in tech, in contrast to the large-cap S&P 500, where technology companies make up more than 35% of the index. Mid-caps also lean far more heavily into industrials. The S&P 500 allocates roughly 7% to industrials, while the S&P 400 comes in closer to 22%. It doesn't stop there – mid-caps offer more financials, consumer discretionary, energy, and materials than its large-cap counterpart. In other words, investors are on the receiving end of a much broader mix of economically sensitive sectors, with far less dependence on a single theme carrying the market. That diversification matters, and it is not exclusive to the US.

Brent Joyce also offered the following commentary in his 2025 year end recap:

“The bull market has broadened out, but we don’t see this as a sign of mania. It’s a healthy development if the broadening is supported by solid earnings growth – which it is. Annual earnings growth expectations for 2026 across the major equity market indices of Canada, the U.S., Europe, Japan and emerging markets range between a solid 12% and 16%. We haven’t seen that level of uniform strength for at least five years.”

Russ Visch, BMO’s Technical Analyst, echoed similar thoughts on Tuesday:

“We also noted in yesterday's report that we're still not seeing any signs of outperformance in the traditionally defensive areas of the market...It's mostly still the economically sensitive areas of the market that are outperforming, which is one of the main reasons we remain bullish and constructive on 2026 overall.”

However, it’s not all rainbows and butterflies. Despite outperforming expectations in 2025, the US economy is starting to show signs of potential weakness based on recent manufacturing and jobs data. Moreover, trade policy is expected to be heavily spotlighted in 2026, and is an area where

tensions may flare. We will be watching the market impact of these areas of concern closely. The good news is that inflation in the US seems to be under control, and all signs are pointing to further interest rate cuts by the Federal Reserve after trimming 75 bps in 2025. As we’ve mentioned in past Newsletters, easing monetary policy will be supportive in providing tailwind for stocks.

The Venezuelan Impact

The major headline this week revolved around the US incursion into Venezuela and their capture of President Maduro last weekend. Without

delving too deeply into the politics or the morality of the circumstances, there were some legitimate concerns over potential volatility in the financial markets in response to the action. However, markets seemingly shrugged off any unease and opened the week quite strongly (especially in the oil sector) before pulling back in recent days. It looks as if they are digesting the geopolitical impact on a day-to-day basis but are not panicking in response to any speculation. The Volatility Index (VIX), which measures signals of fear and turbulence in the

markets, opened the year at 14.95 and closed at 15.45 on Thursday. Anything under 20 is considered to be normal territory.

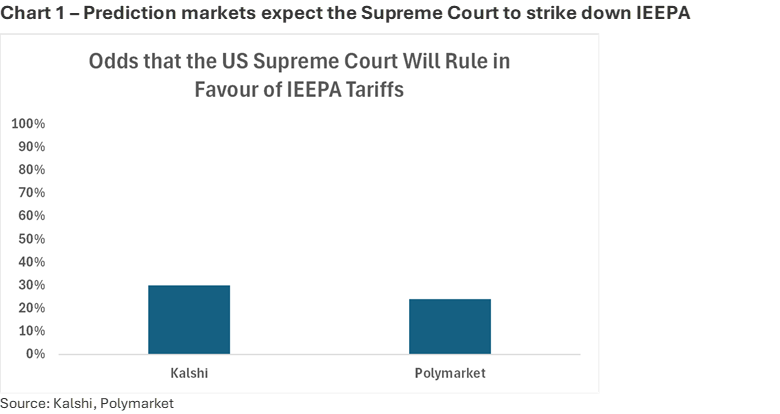

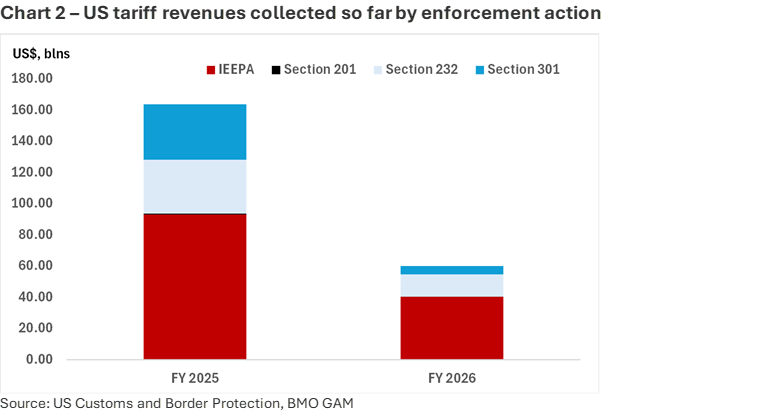

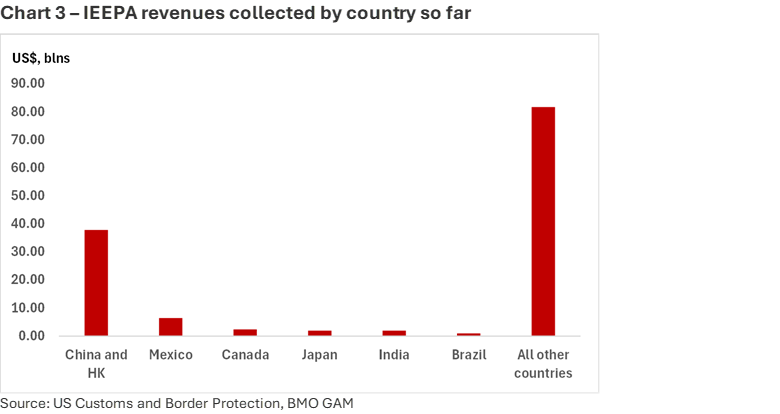

Tariff Update

All the talk about Venezuela has temporarily shifted the focus in the US away from trade, but interestingly, by the time this Newsletter

is released, we may be seeing some news from the Supreme Courts regarding the legality of Trump’s tariffs.

Douglas Porter, BMO’s Chief Economist, wrote in his 2026 Economic Outlook:

“On the tariff front, the second half of 2025 brought some relative stability, though little clarity on policy direction. The Supreme Court could rule that the international emergency duties that account for the majority of new tariffs are illegal. This would only partially curb the Administration, likely resulting in new duties under other trade acts. The USMCA will be reviewed this year and we assume talks will extend at least into next year. While Canada and Mexico have more to lose if the U.S. withdraws (after giving six months' notice), the economy would slow moderately amid disrupted supply chains and new counter-duties. We also assume the U.S. will extend a one-year trade truce with China, averting a sharp rise in tariffs between the two countries.”

While we are waiting on the ruling, BMO Global Asset Management has prepared the following charts that help contextualize the impact of the tariffs so far.

It is clear from the data so far that the tariffs have been more beneficial than harmful to the US economy, but time will tell whether they are fully enforceable or not. We expect that the Trump administration will likely pivot to other acts and provisions if the ruling is not in their favour.

Bottom Line

We’ve been preaching cautious optimism regarding the markets quite regularly, and that sentiment has not changed as we turn our calendars to

2026. The broadening of participation in uptrends is indicative of a healthy market. Traditionally defensive sectors are not outperforming, which is a clear sign that investors are still willing to take on risk and are still being rewarded for it. As such, we remain (almost) fully invested, and in the Green Zone. However, should the markets show signs of sustained weakness, we will not hesitate to pivot to safer assets classes as needed.

As always, should you have any questions regarding your portfolios or planning, or if you would like to meet in person or by phone or video conference, we are pleased and ready to do so. Once again, we’d like to sincerely wish all of our readers a wonderful new year.

Regards,

John, Victor and Megan