Investment Insights Spring 2026

Paul D'Elia - May 22, 2026

- Estate Planning

- Financial Planning

- Investment Services

- Portfolio Management

- Retirement

- Special Reports and Newsletters

- Tax Planning

- Total Client Experience

- Wealth Management

In This Issue • Generation Squeeze: 30 Years of Inflation • Beyond Canada: A Look at Global Markets • How Is Investment Income Taxed? • The Wealth Gap: A Two-Speed Economy • Strategic Insurance Planning for HNW Investors

The Diversification Imperative

As trade threats have escalated, they have prompted the question: If the U.S.-Mexico-

Canada free trade agreement (USMCA) were dismantled, what would happen to Canada?

Trade remains top of mind for many investors. While USMCA renegotiations were originally

expected in the months ahead, debate over its future has come back into focus, driven by tariff

rhetoric that continues to fuel uncertainty. Many economists expect the agreement to survive

in some form, as dismantling it would risk disruption in a midterm election year, despite the

increasingly heated tone.

Prime Minister Carney’s provocative speech in January at the World Economic Forum, cautioning that the old rules-based international order is unlikely to return under current hegemonies, was hailed by some as one of the boldest by a Canadian leader in decades. His message was clear: Canada must act decisively with a new economic strategy, and focus on diversifying global trade relationships.

But how feasible is it to reduce dependence on the United States? Exports alone to the U.S.

represent roughly 20 to 25 percent of Canada’s GDP, underscoring the scale of that challenge.

Unwinding integrated trade relationships can carry lasting economic costs. The United Kingdom’s exit from the European Union offers a cautionary example: a decade after the referendum, the UK economy is estimated to be 6 to 8 percent smaller than it would otherwise have been.1

However, a recent study suggests a more tempered outlook. Oxford Economics projects that a

collapse of the USMCA would reduce Canada’s GDP by about 1.8 percent below baseline and cut private investment by 6 to 7 percent; not great, but far less severe than past downturns Canada has absorbed and recovered from.2 In the early 1980s recession, Canada’s economy contracted by around 5 percent, and unemployment peaked at 12 percent, driven by elevated inflation and sharply tightened monetary policy. High trade barriers between Canada and the U.S. are also not unprecedented, having occurred during long stretches of the 19th and 20th centuries.

Not to diminish the potential consequences, but Canada’s inherent strengths provide reason

for broader optimism. We are a nation rich in resources, boasting abundant fresh water, three

coastlines and the most educated population globally.3 Beyond these advantages, Canada’s

stability, both politically and economically, offers a firm foundation for investors, businesses and

policymakers alike. Under current leadership, there is a clear imperative to reorient the economy.

Regardless of political views or opinions on specific trade partners, Carney has been steadfastly

working to diversify trade and attract investment to build resilience into Canadian supply chains.

These lessons extend into investing as well. What seems certain one day can quickly reverse

tomorrow. Nothing lasts forever. Diversification is not just prudent; it is imperative for managing

the risk of change. Markets are inherently volatile, and, at a time when impulsiveness may feel

embedded in the new world (dis)order, discipline during periods of uncertainty is critical as the

range of outcomes can vary widely. Balancing conviction with flexibility enables investors to pivot

when necessary, a core part of our role as advisors in managing portfolios.

While the path ahead may look complex today, Canada has the tools and resilience to navigate it

with resolve. Our capacity may be tested, but the country remains well-positioned to meet the task.

1. “If free trade dies, what happens to Canada,” T. Shufelt, Globe & Mail, Jan. 31, 2026, B10; 2. www.oxfordeconomics.com/resource/usmcascenarios-north-american-trade-at-a-crossroads/; 3. https://worldpopulationreview.com/country-rankings/most-educated-countries

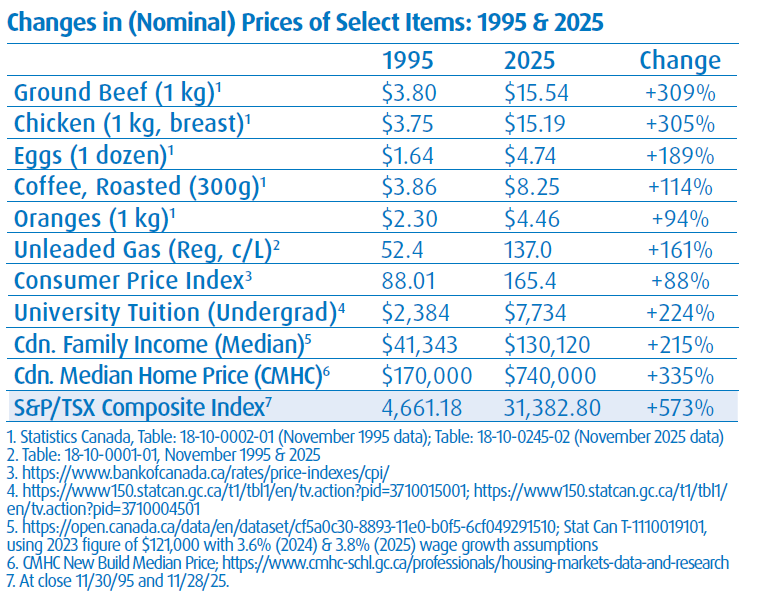

Generation Squeeze: 30 Years of Inflation

Flash back to 1995: Do you remember a time when gas cost 52 cents per litre, and a carton of eggs would run just $1.64?

A market observer recently noted that “quiet compounding”—the silent, gradual growth over long periods—has given rise to some of the most remarkable features of the universe: from towering sequoias and complex organisms to majestic mountains. This concept also holds true in investing: compounding power can yield noteworthy results, though it’s often overlooked because it requires time. As we start a new year, the following may serve as a reminder of its potential impact over time.

With Canadian food prices rising by 6.2 percent in 2025 alone, Canada has recently been dubbed the “food inflation capital” of the G7 (Group of Seven advanced economies). It therefore comes as little surprise that Prime Minister Carney moved in January to introduce a grocery rebate (an enhancement of the existing GST/HST rebate) for low-income earners.

There is little question that inflation has driven up the cost of most goods substantially in recent years. Viewing those increases over a 30-year period provides additional perspective. Many Canadians would be hard-pressed to recall a time when a kilogram of chicken cost just $3.75. While the Consumer Price Index (CPI), the federal government’s official measure of inflation, suggests that average prices have risen by roughly 88 percent over three decades, your grocery bill likely tells a different story.

The good news? Over the same period, investors have seen the S&P/TSX Composite Index rise more than 573 percent (and this is excluding reinvested dividends!). This return has outpaced price increases across every category on the chart, including average home prices during a prolonged housing boom. Of course, this growth did not come without volatility, including four bear markets spanning a combined 40 months, two of which saw declines of more than 45 percent. Still, for investors who stayed the course, equities have proven to be one of the most effective tools for building wealth and offsetting inflation. And, if history is any guide, that’s encouraging news for long-term investors looking ahead to the next 30 years.

Note: Interestingly, we also examined a 20-year period and found similar results—investment in the S&P/TSX Composite index would still have outpaced the price increases across all categories shown in the chart.

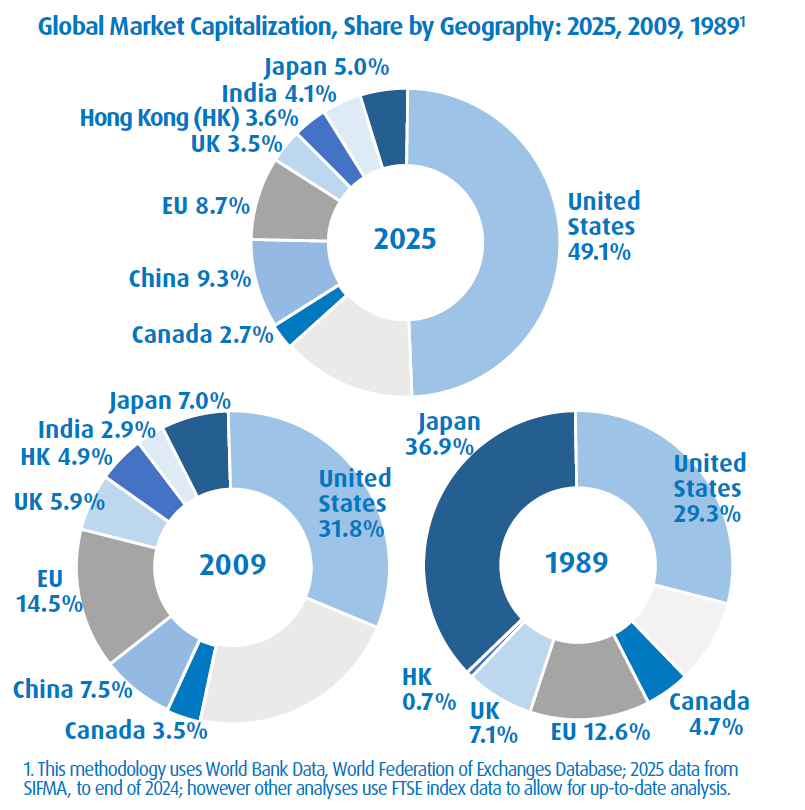

The evolution of market share over the past decades demonstrates that nothing is permanent. Japan’s experience is a reminder that even widely held predictions can be wrong, reinforcing the value of diversification and adaptability in navigating an uncertain future.

How Is Investment Income Taxed?

With tax season in full swing, here’s a refresher on common types of investment income and how each is taxed.

While this overview focuses on investments held in non-registered accounts, keep in mind that the type of account where investments are held impacts tax obligations. While this article doesn’t address investment location, given our role as advisors, we can provide perspectives.

Interest Income — Income earned from interest-producing bank accounts and fixed-income investments, such as GICs, government Treasury bills, bonds and fixed-income mutual funds/ETFs is taxed as ordinary income. It is fully taxable at your marginal rate, making it one of the least tax-efficient types of investment income. During tax season, it’s important to remember that, generally, interest income is taxable in the year it is earned and must be reported on a tax return, regardless of whether it has been received.

Dividends From Canadian Corporations — Canadian dividends are designated as either “eligible” or “non-eligible” and are included in income at a grossed-up rate. However, they generally qualify for the dividend tax credit, which can reduce the taxes you pay. Eligible dividends (typically received from larger publicly-traded Canadian corporations, but also issued by private corporations) qualify for an enhanced tax credit. Non-eligible dividends are typically received from Canadian private corporations to the extent their income is subject to tax at the lower small business rate. In general, Canadian dividend income receives preferential tax treatment compared to interest income. That said, since the grossed-up amount is reported on your tax return, it can potentially impact income-tested government benefits, like Old Age Security.

Dividends From Foreign Corporations — Dividends from non-Canadian corporations are fully taxable at your marginal rate and do not qualify for a dividend tax credit. Additionally, they may be subject to foreign withholding taxes at source. A foreign tax credit may be available to reduce the taxes payable.

Capital Gains — When a capital asset, such as company shares, is sold for more than its adjusted cost base (ACB, generally its cost plus any expenses to acquire it), the profit is considered a capital gain when realized. Since 2000, one-half of a capital gain has been included in computing a taxpayer’s income.

Mutual Funds and ETFs — There are additional considerations for mutual funds and ETFs. In general, when held in a non-registered account, two situations require you to report information on an annual tax return: i) when a fund makes a distribution, and ii) when you dispose of some or all of your fund holdings.

• Distributions — A distribution represents the earnings being passed to the investor/unitholder. Distributions are taxed based on type (i.e., dividends, interest, capital gains) and are taxable whether you receive the distribution in cash or reinvest it in additional units. The amount of the reinvested distribution is also added to the ACB of your investment.

• Return of Capital (ROC) — A ROC may be reported as a distribution and represents a return of your original investment. This generally occurs when the amount distributed exceeds the fund’s earnings (income, dividends and capital gains). ROC is not considered income and is non-taxable, but generally reduces the ACB, as long as the ACB is positive.

It’s important to keep good records of changes to the ACB as a result of reinvested distributions and ROC. When the fund is eventually sold, this must be reported on a tax return and any capital gain/loss resulting from the disposition will be based on the ACB.

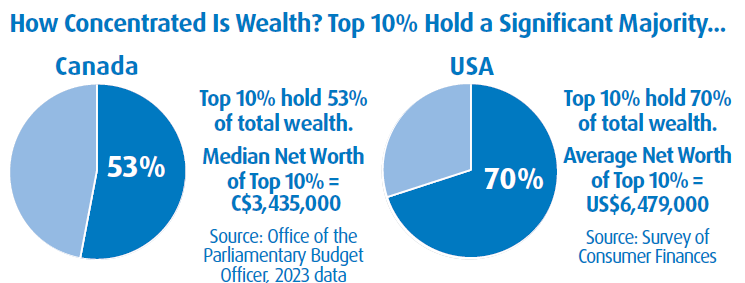

The Wealth Gap: A Two-Speed Economy

Canada’s wealth gap continues to reach historic highs. Recent Statistics Canada data shows the gap between the top 20 and bottom 40 percent of households reached 62.4 percentage points in Q3 2025.1 This divergence is often referred to as a “K-shaped economy”: the upward-sloping arm represents higher-income households, supported by rising income and wealth, while the downward-sloping arm reflects low- and middle-income households facing stagnant wages, rising living costs and mounting debt.

This has implications for investing. In a two-speed economy, consumer segments and the businesses serving them are growing at different rates. Higher-income households continue to drive a disproportionate share of economic activity. In the U.S., where consumer spending accounts for more than two-thirds of total GDP, at one point last year, the top 10 percent of earners accounted for nearly half of all consumer spending. Economic resilience has been driven by wealthy consumers, who have benefited most from asset price appreciation. As a result, softer labour-market data in 2025 attracted less concern since the impact was concentrated among lower-income households with a limited effect on overall consumption.

Where are economies headed? In the U.S., if consumer spending endures and tech capital investments begin to show real returns, markets are likely to continue discounting labour-market weakness. Canada’s picture is more nuanced, challenged by heightened trade uncertainty, slower population growth and an overall cooling labour market. While U.S. tariffs have weighed on exports and jobs in affected industries, substantial spending announced in last November’s Federal Budget is expected to help offset some pressure.

As advisors, we continue to navigate the evolving landscape. The K-shaped economy reinforces the value of time-tested principles such as diversification, quality and ongoing risk management as key to successful long-term wealth management in an increasingly uneven economic environment.

1. https://www150.statcan.gc.ca/n1/daily-quotidien/260129/dq260129b-eng.htm

Strategic Insurance Planning for the HNW Investor

As a high-net-worth (HNW) investor, you likely have more complex insurance needs than the average investor, and not just because you have more assets to protect. With greater wealth comes more complex structures, broader objectives and often a desire to ensure that hard-earned success creates a lasting impact. Here are five ways your needs are unique and how insurance strategies can provide support:

1. Larger, More Diverse Estates to Protect — Many HNW investors have significant wealth tied up in private corporations, real estate and investment portfolios. Here, insurance can provide more than just basic protection: it can help create essential estate liquidity, facilitate succession planning or equalize inheritances when assets like businesses or property are difficult to divide. Unlike Wills or testamentary trusts, insurance proceeds transfer privately (outside of probate). This discretion and control may be valued by HNW individuals who prioritize confidentiality and ease for beneficiaries.

2. Tax Efficiency Is Paramount — Insurance can play a valuable role in HNW tax planning. Permanent insurance offers tax-deferred growth on the policy’s cash value. It can also facilitate a tax-efficient wealth transfer. Given high marginal tax rates and the deemed disposition of assets at death that can trigger significant capital gains tax, strategic use of insurance may help preserve more wealth for beneficiaries.

3. Legacy Goals and Family Planning — Insurance can play a central role in turning long-term intentions into lasting impact. Whether the goal is to support heirs equitably, endow charitable initiatives, sustain a family enterprise or protect vulnerable family members, insurance can help support these outcomes while addressing future tax liabilities without forcing the liquidation of valued assets. Some families also incorporate intergenerational strategies, such as gradually transferring policy ownership to children or grandchildren, allowing wealth to grow tax-efficiently and transition smoothly across generations. Others use insurance to fund a trust to provide long-term care or financial longevity for vulnerable family members, without compromising eligibility for government benefits.

4. Enhancing Investment Portfolios — Often, HNW investors have already maximized contributions to tax-advantaged accounts like RRSPs or TFSAs, and may hold substantial assets in non-registered accounts. As such, they may seek ways to minimize the tax burden associated with non-registered investments. This is where permanent insurance solutions offer an opportunity. The tax-preferred growth of the cash value in participating whole life insurance, along with the tax-free death benefit (and protection from probate fees, where applicable), makes insurance a potential alternative to low-risk fixed-income options. Some policies may even outperform the fixed-income component of a traditional balanced portfolio on an after-tax basis. As a result, alternative wealth strategies using insurance and annuities are increasingly used to complement investment portfolios and provide diversification.

5. Business Support and Succession Planning — For business owners, insurance can help fund buy-sell agreements, cover key person risks or support a smooth ownership transition to the next generation or business partners. It can help ensure continuity and financial stability during periods of change. For estate planning, holding insurance within a corporate structure may offer additional tax advantages, including the use of the capital dividend account to distribute death benefits tax free to shareholders.

Insurance can be a compelling addition to a high-net-worth wealth strategy, not just as a standalone product, but as part of an integrated plan. Tailored insurance solutions help protect what matters most while unlocking opportunities to shape your legacy. If you’d like to explore how insurance can complement your wealth plan, please get in touch.

To Our Clients:

Volatility has returned, not just to financial

markets but also to U.S. policy, driving geopolitical

uncertainty amid widening global conflict. Even

before recent events, there were notable swings

in precious metal prices alongside a declining U.S.

dollar. Technology stocks, despite solid earnings,

were punished for elevated capital expenditures,

and concerns over artificial intelligence disruption

spread across sectors.

Despite this, (at the time of writing) equity market

indices have largely held their own. Perhaps many

have learned from the policy-driven disruption

of 2025 to maintain a longer-term focus, often a

prudent strategy during periods of uncertainty.

After what has seemed like a particularly long

winter for many, take time to enjoy the spring

months ahead. Please don’t hesitate to call should

you require any investment assistance.

D’Elia Wealth Advisory Group

BMO Nesbitt Burns

Paul D’Elia

B.Comm. (Hons), CIM®, PFP®, FCSI®

Senior Wealth Advisor

Senior Portfolio Manager

BMO Private Wealth is a brand name for a business group consisting of Bank of Montreal and certain of its affiliates in providing private wealth management products and services. Not all products and services are offered by all legal entities within BMO Private Wealth. Banking services are offered through Bank of Montreal. Investment management, wealth planning, tax planning, and philanthropy planning services are offered through BMO Nesbitt Burns Inc. and BMO Private Investment Counsel Inc. Estate, trust, and custodial services are offered through BMO Trust Company. Insurance services and products are offered through BMO Estate Insurance Advisory Services Inc., a wholly-owned subsidiary of BMO Nesbitt Burns Inc. BMO Private Wealth legal entities do not offer tax advice. If you are already a client of BMO Nesbitt Burns Inc., please contact your Investment Advisor for more information. BMO Nesbitt Burns Inc. is a Member – Canadian Investor Protection Fund and is a Member of Canadian Investment Regulatory Organization. BMO Trust Company and BMO Bank of Montreal are Members of CDIC. “BMO (M-bar roundel symbol)” is a registered trademark of Bank of Montreal, used under licence.

BMO Private Wealth provides this publication for informational purposes only and it is not and should not be construed as professional advice to any individual. This newsletter was produced by J. Hirasawa & Associates, an independent third party for the individual Investment Advisor noted. While every effort is made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions which are accurate and complete, the author does not accept responsibility or liability resulting from the information or content provided. The information contained in this publication is based on material believed to be reliable at the time of publication, but BMO Private Wealth cannot guarantee the information is accurate or complete. Individuals should contact their BMO representative for professional advice regarding their personal circumstances and/or financial position. The comments included in this publication are not intended to be a definitive analysis of tax applicability or trust and estates law. The comments are general in nature and professional advice regarding an individual’s particular tax position should be obtained in respect of any person’s specific circumstances.

BMO Private Wealth is a brand name for a business group consisting of Bank of Montreal and certain of its affiliates in providing private wealth management products and services. Not all products and services are offered by all legal entities within BMO Private Wealth. Banking services are offered through Bank of Montreal. Investment management, wealth planning, tax planning, philanthropy planning services are offered through BMO Nesbitt Burns Inc. and BMO Private Investment Counsel Inc. If you are already a client of BMO Nesbitt Burns Inc., please contact your Investment Advisor for more information. Estate, trust, and custodial services are offered through BMO Trust Company. BMO Private Wealth legal entities do not offer tax advice. BMO Trust Company and BMO Bank of Montreal are Members of CDIC.

® Registered trademark of Bank of Montreal, used under license.