Beware the Ides of March, or not?

Markets saw the typical and seasonal pullback in the last half of February after a bull market going all the way back to late 2023. However, we still continue to emphasize that this is an overdue and expected decline to restore health to the market, shake out the speculators and lose the weak. The catalyst, of course, was the fear over the Trump tariffs, which created investor uncertainty and fear, compounded by the strong emotional response that Trump evokes.

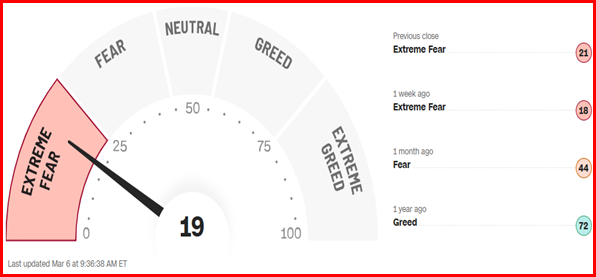

Uncertainty creates volatility, and we saw the “volatility index” jump the past couple weeks, but not to a point where we are seeing the market move into the yellow or red zones. We have, however, seen our short-term charts and indicators break, and that indicated to us that our portfolio needs to take a more defensive stance, but our mid to longer term indicators are all still intact and we remain in the Green Zone. There may be some more volatility here and possible further pullback, but we believe markets are now close to, if not, “oversold”. As a matter of fact, when we look at the CNN Fear and Greed Index, which is currently in the extremes, it is usually a signal of a bottoming and the potential for an upcoming reversal. The fear may create new opportunities to move back on full offense in the near future and put new money to work.

There are concerns and we will discuss those below, and should they cause the market to weaken much further, we are always prepared to go fully on defense, including raising cash. However, the bottom line is that we still consider the current pullback as “normal”. As of writing here early Thursday morning, we are seeing a draw down again, but not below the lows of the week. As such, the Bull Market so far, is still intact.

The fourth chart below is the U.S. SP500. Note the upward channel “trend” going back all the way to October 2023. The lower line of the channel has been slightly broken, but only barely. From a technical view, a return bounce to the upside is still very much the higher probability. As long as we hold here and continue to remain above the pink and green lines just below, we remain positive on the continuation of the market to the upside.

Figure 1 SOURCE: SIACHARTS.com

Figure 2 SOURCE: https://www.cnn.com/markets/fear-and-greed

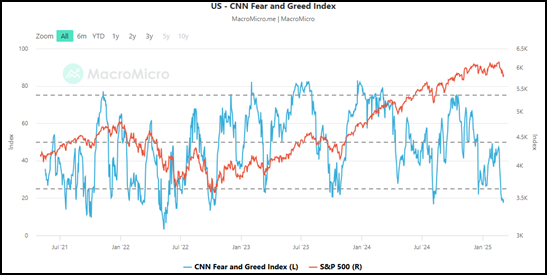

Figure 3 Source: https://www.cnn.com/markets/fear-and-greed

Figure 4 Source: Investing.com

The Trump Trade

We are seeing investor uncertainty as a result of the new round of tariffs, even given the exemptions for automotive parts as of Thursday. This has been the overdue catalyst for at least some downside and pullback, especially given the fact that the latter half of February tends to be historically weak. That said, we do think that the selloff is close to, if not, overdone. As of writing Thursday morning, the markets are still holding their lines. Here are some highlights:

Canada:

- President Trump signaled that broad-based tariffs on Canadian exports will come into effect on March 4th.

- If enacted, these tariffs would hit just when the economy is on the mend. Canada’s economy advanced at a healthy 2.6% annualized rate in Q4, bolstered by consumer spending.

- Although markets currently judge it as a near 50/50 proposition, we think the Bank of Canada will cut their policy rate on March 12th.

U.S.:

- The Fed’s preferred inflation metric, core Consumer Spending, rose 2.6% year-on-year in January, in-line with expectations and continuing to converge with the Fed’s 2% target.

- The Conference Board’s Consumer Confidence Index showed a material decline in February, as tariffs weighed on sentiment and boosted inflation expectations.

- The President announced an additional 10% tariff on China set to take effect on March 4th, in concert with the previously announced 25% tariffs against Canada and Mexico

We have seen the fear created by these tariffs, especially in the tech stocks. However, we must point out again that this market has had a great run and this pullback is normal. We believe investor sentiment, again as highlighted by the Fear and Greed chart above, is an example of investors generally over-reacting to news.

We are also seeing the large numbers of investments coming into the U.S. as Trump has pushed, with hundreds of billions pledged from tech and industrial companies alike. They would not be doing so if they were not positive on the U.S. outlook.

On that note, we present an excellent clip from our own BMO Capital Markets Chief Investment Strategist, Brian Belski. He was a guest on FOX Business on Wednesday (and has been on CNBC all week) and discussed the market changes due to President Donald Trump’s policies. He reiterates our same theme that this is a pullback in a long upside market but really feels worse than it actually is, and that more reassuringly, the tech stocks that were the generals in this bull will resume their course. To watch the segment, click on the following link: Investment strategist is ‘feeling bullish’ about markets despite tariff uncertainty and growth concerns | Fox Business Video

Earnings Fundamentals

We would also like to point out that the last round of reports showed that company earnings are still coming in strong, which is not the sign of a market or economy breaking down:

FactSet reported that the Q4’24 blended, year-over-year (y-o-y) earnings growth rate for the Index stood at 18.2% as of 2/28/25, marking the sixth consecutive quarter of y-o-y earnings growth for the Index.

Should this hold, it will mark the highest y-o-y earnings growth rate for the Index since Q4’21 when it surged by 31.4%. What makes the current quarter’s earnings growth rate even more impressive is that Q4’21’s results reflect favorable comparisons due to the COVID-19 lockdowns.

With 96.2% of companies reporting, the Index’s fourth quarter earnings growth rate currently stands at 18.2%, the highest since Q4’21. Notably, analyst estimates for 2025 and 2026 imply continued earnings growth. The Index’s earnings per share are estimated to total a record $271.28 in 2025 and $308.88 in 2026, according to data from FactSet (as of 2/28/25).

The Technicals

As the fourth chart above on the SP500 highlights, this market is pulling back off the channel, but so far holding. These are the lines we watch. Again, we provide additional comments from our own BMO Nesbitt Burns Technical Analyst, Russ Visch:

Daily Action Report – “In our first missive of the new year we highlighted our medium-term timing model, where deterioration across the spectrum of indicators suggested the likelihood of a more pronounced/prolonged corrective process at some point late in the first quarter which brings the major indexes back to their 200-day moving averages. Two months later the S&P 500 is down 6.75% and the Nasdaq is down 11.12% from their all-time highs. The good news is that both indexes appear to be stabilizing at their rising 200-day moving averages while short-term momentum gauges are beginning to turn positive from oversold extremes. That sure looks like a trading low to us. We would allow for some more near-term volatility until we get more clarity on the tariff situation but "oversold and at a rising 200-day moving average" is one of the best buy set-ups there is in technical analysis.”

USD and Interest Rates and Gold

Typically, when the U.S. dollar and U.S. Bond rates rise, it is because investors are worried on a global level. They then tend to flock to those safe havens, which also includes gold. We have not seen that so far. The U.S. dollar has been declining, as have the rates on U.S. bonds. Investors and money have been leaving those assets since the beginning of the year. Gold is up year to date, but it pulled back in the last half of February just like stocks. It has not been acting as the safe haven one would expect.

Historically, when the US dollar and bonds are declining as they have been, it is a positive tailwind for stocks to move higher going forward.

Bottom Line:

Fear has driven the market down, but the fundamentals and technical analysis all indicate we are seeing a normal pullback in the markets after a long run up. The short-term charts have had us raise some cash and become more defensive, but we expect that it will be short lived as we may approach what might be a bottoming process. Should it hold here, then based upon the fact that we are still well into the Green Zone in our mid to longer term indicators, we may soon look to get fully reinvested.

As always, we do not subscribe to buy and hold, and should the facts change, our strategy will follow suit. We are watching “price” and the charts and signals closely in the meantime.

- John, Victor & Megan