Weather is heating up. Stocks may be cooling down.

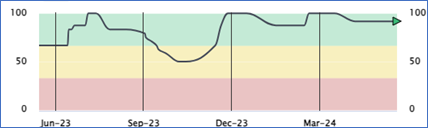

It’s June and the continent is indeed heating up. With the latest El Nino, the weather gurus are projecting the worst hurricane season in years. Globally stocks, on the other hand, may still see some cooling after such a long run from the lows of last October. This could indeed be setting up as an example of the mantra “sell in May and go away”. We are still, however, well into the Green Zone in our Stoplight (Equity Action Call) and stocks are still the favoured asset class. We also continue to outperform both our Canadian and Global benchmarks and have taken steps to protect those profits.

Source: SIACHARTS.COM

That said, stocks, particularly the Growth Stocks like Netflix and Nvidia (which makes a lot of the microchips for cars and phones) are hitting their highs again on Wednesday as they are viewing the potential catalyst of lower interest rates to break out and move higher.

Rate cuts?

The general catalyst for the markets this past year has really been the inflation outlook and interest rates. Many thought U.S. rates would begin to come down in March. When inflation was still showing stickier than the central banks had anticipated, the Fed telegraphed that it could be higher rates for longer and markets pulled back. Data continues to be mixed but as recent as early this week, there were some reports beginning to show a bit of a slowdown in manufacturing and jobs and the Growth stocks are responding by pushing to the top again. Whether they can break through and go higher becomes the question and what we are watching closely for.

The concern, and one we had earlier in the year, is the failure of the broader market and the small to mid size companies, as well as the Canadian market, to take part in these moves. Their performance has been half or less of the “growthier” markets. That is an indicator that the overall economic situation is still rather tenuous going forward.

In Canada, our economy is showing to be consistently weaker in comparison to our neighbours down south. Even the recent rollover towards commodities, of which Canada is considered heavily weighted in our economy (35% of our stock market), did nothing to really spur our market, our economy or our Loonie. As Douglas Porter, CFA and our Chief Economist and Managing Director of Economics put it last week:

“In other words, the U.S. economy has outpaced Canada’s by more than 2 percentage points in the past year, a very wide gap indeed. U.S. core CPI is running at 3.6% y/y, almost a full point above the comparable measure in Canada. And the U.S. unemployment rate has nudged up a half point in the past year to a still-low 3.9%, while Canada’s jobless rate has jumped a full point to 6.1%. Reinforcing that message, the job vacancy rate in Canada has fallen all the way back to pre-pandemic levels at 3.4%. Pulling these threads together, there is a very good case for the Fed to remain patient, but there is an equally good case for the Bank of Canada to begin trimming rates, forthwith.”

This explains why here on Wednesday morning, we saw the first of the rates cuts in Canada -- down 0.25%:

EconoFACTS – BoC — The Big Ease-y

Douglas Porter, CFA, Chief Economist

The Bank of Canada cut its key lending rate 25 basis points to 4.75% today, the first reduction in more than four years, the first such move since Tiff Macklem became Governor, and the first cut by a G7 central bank this cycle. The rate cut was largely built in by financial markets, but was far from a sure thing, so the wording really matters here. The overall tone was constructive for further cuts, and frankly a bit more dovish than we would have expected, but still with a healthy dose of caution. The Bank is clearly impressed with the broad moderation of underlying inflation in 2024, and plainly states that policy does not need to be so restrictive any longer, but is also obviously wary about moving too quickly.

The key message from today is that they are going to take this on a meeting-by-meeting basis, so every CPI report matters, as does every GDP and jobless rate release, to a lesser extent. We have been pencilling in rate cuts every other meeting for now as a base case, but—like the Bank—that call is data dependent. There are two CPI (and jobs) reports prior to the July 24 decision; if the inflation reports mimic the very mild results seen so far this year, a cut is very much on the table for that decision as well.

Some key quotes from Governor Macklem's Opening Statement (which has more meat than the press release):

-

On further cuts: "If inflation continues to ease, and our confidence that inflation is headed sustainably to the 2% target continues to increase, it is reasonable to expect further cuts to our policy interest rate. But we are taking our interest rate decisions one meeting at a time."

-

On the breadth of inflation: "...the proportion of CPI components increasing faster than 3% is now close to its historical average, suggesting price increases are no longer unusually broad-based"

-

On why they thus cut: "This all means restrictive monetary policy is working to relieve price pressures. And with further and more sustained evidence underlying inflation is easing, monetary policy no longer needs to be as restrictive."

-

On what could go wrong: "We don’t want monetary policy to be more restrictive than it needs to be to get inflation back to target. But if we lower our policy interest rate too quickly, we could jeopardize the progress we’ve made. Further progress in bringing down inflation is likely to be uneven and risks remain. Inflation could be higher if global tensions escalate, if house prices in Canada rise faster than expected, or if wage growth remains high relative to productivity."

For the economy, one 25 bp move, which had mostly been priced in, is not going to make a big impact all by itself. However, it will give at least a small bump to sentiment among borrowers, and brighten the mood in what has been a remarkably quiet housing market. As rates continue to gradually recede in coming quarters, the weight will be lifted off the struggling household sector, likely setting the stage for a modest improvement in growth in the year ahead.

Bottom Line: The first cut may not necessarily be the deepest, but it is the most significant, as it marks the official turning point after more than two years of restrictive policy. This is indeed likely to be the first of a series of cuts, although that series is not going to be a straight line down by any means. The Bank's tone is a bit more dovish than expected, but each and every cut this year will require evidence that inflation is calming.

Although the Bank monitors many economic indicators (as indeed all central banks do), the Bank converted its inflation barometer for operational purposes to a consumer price index measure that subtracts eight volatile components in order to better reflect core inflation. It also takes the foreign exchange rate for the Canadian dollar into its monetary policy decisions.

Monetary policy goals are to aid and abet solid economic growth along with rising living standards. To achieve these goals, inflation is kept low, stable, and predictable. The inflation control target is at the heart of Canadian monetary policy that the Bank and the Government have established. The level of interest rates and the exchange rate determine the monetary environment in which the Canadian economy operates.

The level of interest rates directly affects the economy. Higher interest rates tend to slow economic activity; lower interest rates stimulate economic activity. Either way, interest rates influence the sales environment. In the consumer sector, fewer homes or cars will be purchased when interest rates rise. Furthermore, interest rate costs are a significant factor for many businesses, particularly for companies with high debt loads or who have to finance high inventory levels. This interest cost has a direct impact on corporate profits. The bottom line is that higher interest rates are bearish for the financial markets, while lower interest rates are bullish.

Will Markets hold?

It will be interesting to see where markets move from here. Will they hold these highs or near highs? Or will they break down? They have a had a good run from the bottom of October and the slight pullback we saw in April did little to relieve the overbought pressures. We do expect that we will see some profit taking here and the sellers will probably take some control and potentially push markets back down. Certainly, from a “technical” point of view, it is expected that the computers and algorithms will be acting in such a manner. We could possibly see as much as a 5% pullback again in the shorter term, but nothing in the way of a major correction. Farther out in the year, however, with the lead up to the U.S. election, markets could get rather jumpy as confusion over the potential results become forefront. We could see something then that is more pronounced, but still nothing likely to take us near the Red Zone. U.S. election years usually finish strong and we would expect the same this year. Here are the latest comments from our own BMO Nesbitt Burns Technical analyst; Russ Visch:

Daily Action Report - U.S. equity markets continue to show a great degree of resiliency here despite the recent deterioration in our short-term timing model where breadth and momentum gauges for all of the major averages were fully negative coming into the week. Tactically, we would still allow for the S&P 500 and Nasdaq Composite to back and fill around their 50-day moving averages at some point (SPX: 5183, Nasdaq: 16,277) which would represent a normal short-term pullback within an otherwise healthy medium/long-term uptrend. Given the recent deterioration in long-term interest rates and a potential minor breakdown in the U.S. 10-year yield we are still working under the assumption that a more pronounced medium-term pullback doesn't get underway until later in the third quarter, which is more in line with U.S. presidential election year seasonality.

Bottom Line

Market indexes are pushing to the top once again. In technical analysis however, we look at the probabilities of price – just as the computer do. They now run eighty percent of the market and will be taking some profits here and with that, we will see some limited pullback. Remember, we are not trying to compete with or beat the computers, but with the availability of technology and technical analysis, we can trade alongside them and take profits too. We do not have to buy and hold nor accept all the move to the downside.

We mentioned the concern of the lack of participation by the broader markets, particularly in small to mid-size companies, which indicate some potential underlying weakness. We are also going into the weaker seasons of the year, which will include the U.S. election and the aforementioned increase in volatility. So, even though we are in the Green Zone mid to longer term (meaning six to twelve months), in the shorter term we do expect some profit taking and pullbacks before the summer and again into the fall.

The portfolios for now are somewhat “neutral” to the market. We look to both protect and profit in either direction, though not necessarily as much on the big up days as the market. We would rather miss some upside than catch more downside.

Therefore, we continue to maintain our exposure to both the growth stocks, which are holding up the majority of the market on those good days, as well as a significant exposure to defensive positions such as gold, quasi-inverse ETFs (that profit on downside), some cash/money market holdings, and a greater weighting to more protective fixed income. We continue to outperform our benchmarks and look to shield the profits. We will stick to our strategy and rules and when the charts and indicators confirm the worst is likely over, we will look to climb fully back in. Until then, we will be conservative from here.

- John, Victor and Megan

We do aways look forward to our client meetings and you don’t have to wait until the next scheduled contact.

Should at any time you would like to meet with us, please do contact us, by phone at 905-727-5040 or email at Ridd.Associates@nbpcd.com.

We would be pleased to setup an in-person meeting, phone meeting or virtual meeting, at a time that is convenient for you.

We look forward to reviewing your portfolio and wealth plan as well as answering any questions you may have.

If you know someone who can benefit from what you have learned today, please feel free to share this newsletter with them.