After a successful 2024 for the markets and for your portfolios, we are now a couple weeks into the New Year. Markets in 2025, however, are not as positive as we would like to see them so far. We are off the highs of mid-December but given the run in the market for the past year and a half, a pullback was not out of line. We are still well in the Green Zone mid-to-longer term and looking forward to a relatively positive year ahead. In the much shorter term, there are some concerns, and we are more in the Yellow Zone and have increased cash and similar assets accordingly.

Reminder for RRSP and TFSA Contributions and for RRIF and LIF Withdrawals

This is that time of year for TFSA and RRSP contributions. The limit again for contributions to TFSAs for 2025 will be $7,000 per person. Should you be on our automatic list, your contribution will probably have been made by the time you read this.

The RRSP contribution room for the 2024 calendar year is 18% of your earned income from the previous tax year to a maximum of $31,560, less any pension adjustments. Should you require assistance in making this year’s contribution, please contact our team before the deadline of March 3, 2025. As always, we request you contact us a soon as possible instead of waiting until the deadline to ensure prompt processing of your contribution.

RRIF and LIF withdrawal minimums and maximums have now been set based on the 2024 year end balance. Should you have any questions regarding your draws, please contact our team.

2024 the year that was:

2024 was a strong year for the markets overall, particularly for the growth and tech stocks. As we suspected, the election of Trump saw markets run even higher in November on the basis that Republicans tend to be the party of pro business, less government, low regulation and lower taxes. The U.S. economy remained strong and as such, inflation (albeit slightly lower year over year) and interest rates are still a large concern. Investors toward the end of the year began to rightfully worry that interest rates would not be coming down as quickly as anticipated and hence, we did not see the typical Santa Rally.

In Canada, our economy was unfortunately much weaker given the higher government spending – the federal budget came in 50% higher than projected! There continued to be a lack of emphasis on growth and investment, especially in the oil and resource sectors for which Canada is known for. The loonie certainly suffered accordingly, dropping over 8% in 2024 alone, from $1.323 USD to $1.44 USD. We did see inflation and rates come down a fair bit more than the U.S., but that was due to the weakness in the economy. There is an election in 2025 and the succeeding government, whomever it may be, has some serious work cut out for them.

Our Performance:

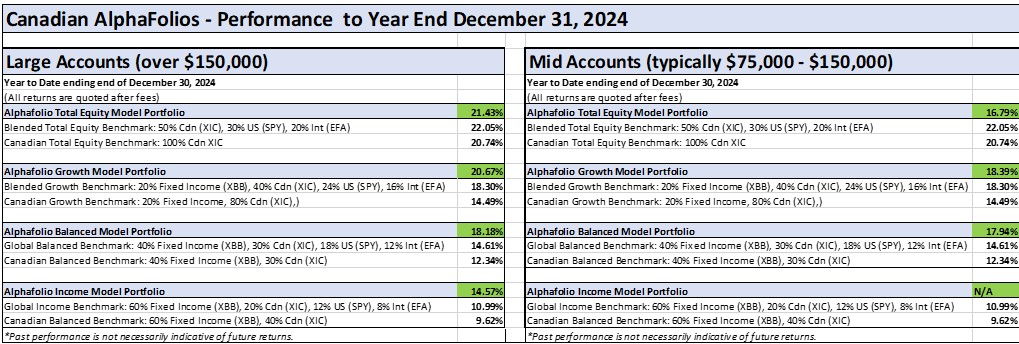

We were pleased with 2024 portfolio performance as we were in line with or outperforming our benchmarks (see charts). The exception was a slight difference in the Total Equity component which saw a bigger drawdown in the last half of December with the larger exposure to growth stocks. We were proactive in trading with changes we made in mid 2023, in looking to move quickly with replacing the losers and letting the winners run. This is also with the ongoing objective of looking to reduce the volatility of the portfolio versus the general market.

Bottom Line: The Equity component performed in line or better with the benchmarks. The Bond / Fixed Income components well outperformed our benchmarks. We will be reaching out to you to book review meetings in the near future. In the meantime, should you like a copy of your personal 2024 year-end Portfolio and Performance reports, please let us know and we would be happy to email or mail them to you.

Outlook for 2025:

We are looking for a positive year again for 2025. There are some potential pitfalls of course. BMO Equity Strategists are projecting a low double digit return expectation on the year as well. We definitely concur in their outlook and here are some of their key conclusions for 2025:

Investment Strategy - January 2025 - Market Insights January 09, 2025

After a fantastic year, market still well supported…but keep a close eye on tariffs and the unemployment rate

The year 2024 brought very strong performance for stock investors in the U.S., Canada, and foreign markets. We believe the market remains well supported for now.

Our key conclusions are as follows:

1. As we enter 2025, we remain overweight equities with a fair value of 29,000 for the S&P/TSX and 6,500 for the S&P 500, implying a better return potential – in local currency terms – for the Canadian market despite Trump’s tariff threats which are undoubtedly a risk (more on this below). The key pillars of this positive stance are: a) a low probability of recession in the next year; b) strong corporate earnings momentum (double-digit growth projected in the U.S. and Canada); c) a relatively favourable inflation and interest rate environment; and d) still reasonable valuation and dividend growth potential for a number of sectors and individual stocks (especially in Canada).

2. At the same time, investors should not underestimate the risks of a Trump-led tariff war and the high valuation for the U.S. stock market (particularly in the Tech and Communication sectors), along with the extreme concentration we are seeing with the top 10 largest U.S. companies comprising more than a third of the S&P 500’s value (a level only matched during the 1970s “nifty-fifty period”).

3. While both markets did well in 2024, the U.S. once again managed to outperform given the country’s huge edge in productivity growth and the S&P 500’s much higher exposure to the Artificial Intelligence theme which has captured investors’ imagination. However, we are seeing sector leadership broaden out and the S&P/TSX remains far cheaper, and the sector weights are more favourable in the context of a “soft landing” scenario (Financials, Industrials and Energy Infrastructure, in particular). Also, the prospect of a new Government with a more sensible economic vision could act as an important catalyst for foreign and domestic investors.

4. We think high-quality, lower-duration stocks (i.e., reasonably valued and paying growing dividends) will regain their luster in the not too-distant future. An example of such stocks are large pharmaceutical companies which have rarely traded this cheaply vs. the market in the last 20 years (currently at 70% of the S&P 500 forward price/earnings multiple).

5. Defensive/interest rate sensitive sectors like Utilities, REITs, and Financials should continue their recovery if we are right in our view that long-term interest rates are unlikely to spike up significantly from current levels. As for shorter term rates, both the Bank of Canada (“BoC”) and the U.S. Federal Reserve (“Fed”) remain in easing mode which has historically been a good tailwind for equities. We believe this is true despite the Fed recently indicating a slower path of interest rate cuts in 2025 relative to overly optimistic trader expectations. Also helpful is that the yield curve is steepening (meaning 10-year rates are now higher than the 2-year rate) which has historically been a good omen for stocks. Drilling down a little deeper, we conducted a study of the last 10 “steepening cycles” going back to 1984 and found that returns were very strong at almost 20% after a year. Dividend payers slightly outperformed non-payers and always had positive returns. This was not the case for growth-oriented, non-dividend payers which got hit very hard following the Tech bubble crash post March 2000.

6. On balance, our macro driver “dashboard” shows that key variables are still flashing a positive picture for equities. Historically, market returns in the U.S. have been better when inflation is coming down (the picture is more mixed for the S&P/TSX since Energy and Basic Material stocks tend to benefit from higher inflation). Also helpful are the steepening yield curve – as mentioned below – and the rising ISM New Orders Index1. Just-released December ISM results came in above consensus, with new orders rising a further 2.5% to 52.5%. This is the fourth straight month of increases, finally pushing through the key level of 50.

In the Shorter Term:

In the past week, we actually increased our cash component versus stocks. With the recent pullback, the market is currently in a short-term downtrend and we felt it was appropriate to take some profits and some risk off the table. In our technical analysis, our charts and indicators crossed our initial lines, highlighting the need for caution, but not for a breakdown yet at this point. So why did the pullback occur, besides the recent run up?

When we look at the actual bond market, interest rates in the U.S. and Canada have risen in the past month along with the US Dollar. This is on fears that inflation is no longer coming down as fast as anticipated. Recent job numbers announced last week corroborated this. Inflation numbers were announced this week in the U.S. and though slightly down, it shows that inflation is clearly stubborn. Potential U.S. tariffs may only exacerbate this, in both the U.S. and Canada. There has even been talk of a need of increasing rates. Rising rates make bonds more attractive and that money tends to leave stocks. Also, a rising U.S. dollar happens when investors are concerned for any reason, as it remains the safe haven and again, money leaves stocks for that safety.

Next week is also the inauguration of the new Trump administration. There are a lot of what-ifs and what-will-he-do’s. He will have a fight on his hands with the U.S. Fed as he wants interest rates lower. His administration will also be taking on a huge battle with a larger bureaucracy, and the battle within the Republicans and versus the Democrats over the deficit and the debt ceiling looms strong. All that creates uncertainty and with that, more volatility for the markets. As such, we consider it rather prudent to move somewhat to the sidelines to let this play out. We would rather miss some upside rather than catch a fair bit of downside. Once the dust settles, we will again look to the stronger relative strength positions and return fully to the market when appropriate.

The geopolitical landscape appears to be changing positively. The war in Israel versus Hamas has come to a ceasefire agreement, more than likely on the comments from Trump and from the push by the Israelis Defence Force – it is too coincidental to be otherwise. A resurrection of the Middle East Accords, particularly with Saudi Arabia, would see more stability in the region. Trump has also vowed to somehow end the war between Ukraine and Russia. We shall see, but the end of both conflicts would provide much comfort to the markets and a reduction of volatility.

However, there is also the expectation for a faceoff with China over TikTok, tariffs and spying. It is clear that U.S. relations with Beijing will worsen; especially with the likelihood for steep new tariffs, which are virtually certain. Both sides of the aisle are mostly in agreement here in their issue with China. We do see this as a potential concern for the economy and for the financial markets. It will be interesting to see how the new administration handles it.

On the Canadian side, we expect that we will see a spring election. The conservatives, should they win, have already indicated they will drop the increase on the Capital Gains Rates and the Carbon Tax, as well as take on reducing expenses including the bureaucracy - similar to the U.S. For the Liberals to win, they will probably have to moderate their stance on this as well. Those should all be good for the economy but will take time to be felt. Our market moves until then will be rather dependent on what the U.S. does, whether it be tariffs or rates, etc. We will therefore continue to be overweight U.S. assets until then.

Bottom Line:

We are in the Green Zone longer term but Yellow Zone in the very short term. As such, we are still majority invested but have increased cash and/or related assets. As an aside, even though markets had a jump back up on Wednesday of this week, we were still in line with the markets or better given the strength of the remaining positions we hold. So far, we have been able to protect on the downside while maintaining on the upside.

We look to the inauguration next week and subsequent moves by the new US administration to provide some clarity on where they want to take the economy, tariffs, interest rates and inflation and how these will affect markets going forward. It is important to remember that markets were quite positive with Trump’s last administration until COVID hit. Baring any major catalysts, we see good reason for the upside to repeat. The potential for a new government in Canada that would be more mindful of expenses, taxes and growth could be quite beneficial as well. Overall, we are indeed positive and look forward to a prosperous New Year!